Homeowners in Judicial foreclosure states need to realize that Banks claim of ownership of the note is not an issue of standing but an element of its cause of action which it must plead and prove

The term “standing” has been applied by the courts to two legally distinct concepts. The first is legal capacity, or authority to sue. The second is whether a party has asserted a sufficient interest in the outcome of a dispute.

Standing and capacity to sue are related, but distinguishable legal concepts. Capacity requires an inquiry into the litigant’s status, i.e., its “power to appear and bring its grievance before the court”, while standing requires an inquiry into whether the litigant has “an interest in the claim at issue in the lawsuit that the law will recognize as a sufficient predicate for determining the issue.”

Wells Fargo Bank Minnesota, Nat. Ass’n v Mastropaolo, 42 AD3d239, 242 (2d Dept 2007) (internal citations omitted). Both concepts can result in dismissal on a pre answer motion by the defendant and are waived if not raised in a timely manner.

In some Jurisdictions such as New York, an action may be dismissed based on the grounds that the Plaintiff lacks the legal capacity to sue. CPLR 3211(a)(3) It governs no other basis for dismissal. CPLR 3211(e) provides that a motion to dismiss pursuant to CPLR 3211(a)(3) is waived if not raised in a pre-answer motion or a responsive pleading.

Many decisions treat the question of whether the Plaintiff in a foreclosure action owns the note and mortgage as if it were a question of standing and governed by CPLR 3211(e).

Citigroup Global Markets Realty Corp. v. Randolph Bowling , 25 Misc 3d 1244(A), 906 N.Y.S.2d 778 (Sup. Ct. Kings Cty 2009); Federal Natl. Mtge. Assn. v. Youkelsone, 303 AD2d546, 546—547 (2d Dept 2003);

Nat’l Mtge. Consultants v. Elizaitis, 23 AD3d 630, 631 (2dDept 2005);

Wells Fargo Bank, N.A. v. Marchione, 2009 NY Slip Op 7624, (2d Dept 2009)

There is a difference between the capacity to sue which gives the right to come into court, and possession of a cause of action which gives the right to relief. Kittinger v Churchill Evangelistic Assn Inc., 239 AD 253, 267 NYS 719 (4th Dept 1933). Incapacity to sue is not the same as insufficiency of facts to sue upon. Ward v Petri, 157 NY3d 301 (1898)

In the case of Ohlstein v Hillcrest, a defendant moved to dismiss a complaint in part based on lack of legal capacity to sue where plaintiff had assigned her stock. The Court denied that branch of the motion holding that even if plaintiff had assigned her stock, “the defect to be urged is that the complaint does not estate [sic] a cause of action in favor of the one who is suing, the alleged assignor – not that the plaintiff does not have the legal capacityto sue. Legal incapacity, as properly understood, generally envisages a defect in legal status,not lack of a cause of action in one who is sui juris.” Ohlstein v Hillcrest, 24 Misc 2d 212,214, 195 NYS2d 920, 922 (Sup Ct NY Co 1959).

The difference was articulated by the Court in the case of Hebrew Home for Orphans v Freund, 208 Misc. 658, 144 N.Y.S.2d 608 (Sup Ct Bx 1955). The plaintiff in that case sought a judgment declaring that an assignment of a mortgage it held was valid. The defendants moved to dismiss the complaint on the grounds that since the assignment was not accompanied by delivery of the bond and mortgage to plaintiff, plaintiff did not own the bond and mortgage and thus had no legal capacity to sue or standing to maintain the action. The Court denied the motion, stating:

The application to dismiss the complaint on the alleged ground that the plaintiff lacks legal capacity to sue rests upon a misapprehension of the meaning of the term. See Gargiulo v.Gargiulo, 207 Misc. 427, 137 N.Y.S.2d 886. Rule 107(2) of the Rules of Civil Practice relates to a plaintiff’s right to come into Court, and not to his possessing a cause of action. Idat 660-661, 610.

The Court then quotes Kittinger v Churchill for the principle that,

“The provision for dismissal of the complaint where the plaintiff has not the capacity to sue (Rules of Civil Practice, rules 106, 107) has reference to some legal disability, such as infancy, or lunacy, or want of title in the plaintiff to the character in which he sues. There is a difference between capacity to sue, which gives the right to come into court, and possession of a cause of action, which gives the right to relief in court.

Ward v. Petrie, 157 NY 301, 51 N.E. 1002; Bank of Havana v. Magee,

20 NY 355; Ullman v. Cameron, 186 NY 339, 78 N.E.1074. The plaintiff is an individual suing as such. He is under no disability, and sues in norepresentative capacity. He is entitled to bring his suits before the court, and to cause a summons to be issued, the service of which upon the defendants brings the defendants in to court. There is no lack of capacity to sue.

The other meaning of standing involves whether the party bringing the suit has a sufficient interest in the dispute. Some cases have held that in this context, standing is jurisdictional, reasoning that where there is no aggrieved party, there is no genuine controversy, and where there is no genuine controversy, there is no subject matter jurisdiction.

Stark v Goldberg, 297 AD2d 203, 204(1st Dept 2002); xelrod v New York StateTeachers’ Retirement Sys., 154 AD2d 827, 828 (3rd Dept 1989).

Some courts have held that the jurisdiction of the court to hear the controversy is not affected by whether the party pursuing the action is, in fact, a proper party.They have held that if not raised in the answer or pre-answer motion to dismiss, the defense that the a party lacks standing is waived. Wells Fargo Bank Minnesota, Nat. Ass’n v. Perez,70 AD3d 817, 818, 894 N.Y.S.2d 509, 510 (2nd Dept 2010), Countrywide Home Loans, Inc.v. Delphonse, 64 AD3d 624, 625, 883 N.Y.S.2d 135 (2nd Dept 2009),

HSBC Bank, USA v. Dammond, 59 AD3d 679, 680, 875 N.Y.S.2d 490 (2nd Dept 2009)

The issue of whether a Plaintiff owns the mortgage and note is a different question from whether it has an interest in the dispute. Whether a party has a sufficient interest in the dispute is determined by the facts alleged in the complaint, not whether Plaintiff can prove the allegations.

Wall St. Associates v. Brodsky, 257 AD2d 526, 684 N.Y.S.2d 244 (1st Dept1999), Kempf v. Magida, 37 AD3d 763, 764, 832 N.Y.S.2d 47, 49 (2nd Dept 2007). For the purpose of determining whether a party has sufficient interest in the case the allegations areassumed to be true.

It is important to note that This issue is not analogous to the issue of whether citizens have standing to seek judicial intervention in response to what they believe to be governmental actions which would impair the rights of members of society, or a particular group of citizens, (e.g. Schulz v. State, 81 NY2d 336, 343, 615 N.E.2d 953, 954 (1993), or whether registered voters have standing to challenge the denial of the right to vote in a referendum pursuant to Section 11 of Article VII of the State Constitution, or whether commercial fishermen have standing to complain of the pollution of the waters from which they derive their living, see also Leo v. Gen. Elec. Co., 145 AD2d 291, 294, 538 N.Y.S.2d 844, 847 (2nd Dept 1989). The issue of standing in these types of cases turn on whether the claimants have an interest sufficiently distinct from societyin general.

Foreclosure actions implicate a concrete interest specific to a plaintiff, and the determination must be made as to whether it has been aggrieved and is therefore entitled to receive monetary damages for the alleged breach of the law.

Therefore homeowners needs to realize that when Banks pled that it owns the note and mortgage and asserts the right to foreclose on the mortgage which it asserts is in default. If it is successful in proving its claims, then usually it is entitled to receive the proceeds of the sale of the mortgaged property. Homeowners should understand that the objection that the Plaintiff in fact does not own the note and mortgage is not a defense based on a lack of standing. Courts will usually claim homeowners “does not say” (insufficient facts were alleged). But that the homeowner’s argument is that the facts alleged are not true. It is not a question of whether the Bank has alleged a sufficient interest in the dispute, but of whether the Bank can prove its prima facie case.

In Judicial States where the Banks are the plaintiff; unlike standing, denial of the Plaintiff’s claim that it owns the note and mortgage is not an affirmative defense because it is usually a denial of an allegation in the complaint that is an element of the Plaintiff’s cause of action.

In a Judicial foreclosure case, the Plaintiff must plead and prove as part of its prima facie case that it owns the note and mortgage and has the right to foreclose. Wells Fargo Bank, N.A., 80AD3d 753, 915 N.Y.S.2d 569 (2d Dept 2011); Argent Mtge. Co., LLC v. Mentesana, 79AD3d 1079, 915 N.Y.S.2d 591 (2d Dept 2010); Campaign v Barba , 23 AD3d 327, 805 NYS2d 86 (2nd Dept 2005).

However, it is usually not enough for the Defendant (Homeowner) to filed a pro se “answer” containing a “general denial”, which is a denial of all of “Plaintiff’s allegations”.

In Hoffstaedter v. Lichtenstein , 203 App.Div. 494, 496, 196 N.Y.S. 577 (1st Dept 1922),the First Department held that the general denial put the allegations in the plaintiff’scomplaint in issue. In that case, the defendant executed a note in favor of the plaintiff as a promise to pay for certain goods. When plaintiff brought an action to recover on the note, the defendant answered with a general denial. It went on to state that “[i]t is elementary that under a general denial a defendant may disprove any fact which the plaintiff is required to prove to establish a prima facie cause of action.” Id., at 578.

The Court of Appeals cited Hoffstaedter v. Lichtenstein in holding that a general denial puts in issue those matters already pled.

Munson v. New York Seed Imp. Co-op., Inc., 64 NY2d 985, 987, 478 N.E.2d 180, 181 (1985).The general denials contained in the answer enable defendant to controvert the facts upon which the plaintiff bases her right to recover. Strook Plush Company v. Talcott, 129 AD 14, 113 NYS 214 (2nd Dept 1908). A generaldenial is sufficient to challenge all of the allegations in a complaint. Bodine v. White , 98 NYS232, 233 (App. Term 1906).The Second Department in Gulati v. Gulati, 60 AD3d 810, 811-12, 876 N.Y.S.2d 430, 432-33 (2nd Dept 2009), held it was that where a claim would not take the plaintiff by surprise and “does not raise issues of fact not appearing on the face of the complaint”, a denial of the allegations in the plaintiff’s complaint was sufficient. It heldthat where the plaintiff alleged as an element of her prima facie case that the defendant abandoned the marital residence without cause or provocation, and the defendant denied these allegations in his answer, defendant did not need to further allege abandonment as an affirmative defense

The Fourth Department in Stevens v. N. Lights Associates, 229 AD2d 1001, 645 N.Y.S.2d 193, 194 (4th Dept 1996), found that a denial by defendant that it was in control of the premises where plaintiff fell did not need to be separately pled as a defense, as the denialof control did not raise any issue of fact which had not already been pled in the complaint.See also

Scully v. Wolff, 56 Misc. 468, 107 N.Y.S. 181 (App. Term 1907), Bodine v. White,98 N.Y.S. 232 (App. Term 1906).

In this case, Defendant’s contesting Plaintiff’s claim in the complaint that it owns the note and mortgage could not take the Plaintiff by surprise as a general denial contests Plaintiff’s factual allegations in the complaint itself, and does not rely upon extrinsic facts. Since ownership of the note was pled in the complaint and is an element of the Plaintiff’s cause of action, Defendant did not waive the defense that Plaintiff did not own the note, because he made a general denial to the factual allegations contained in the complaint.

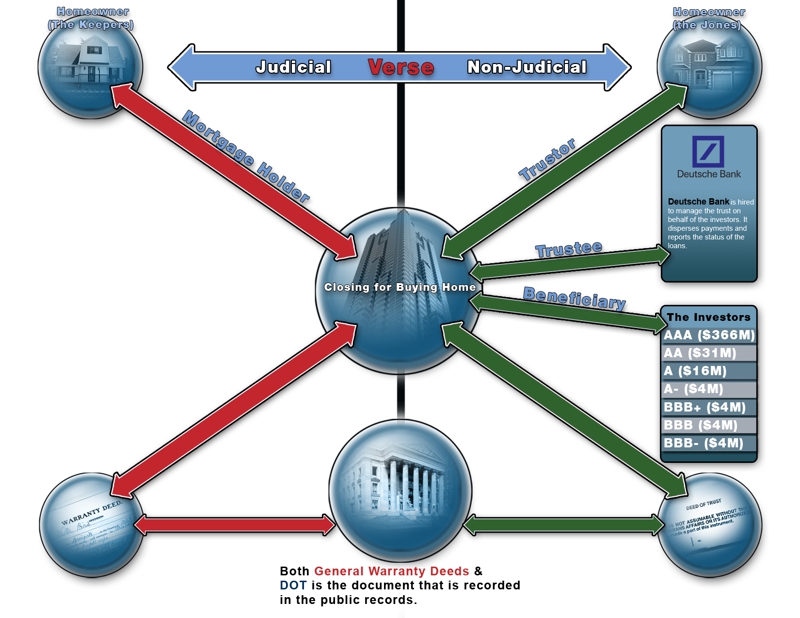

In fact, the identity of the owner of the note and mortgage is information that is often in the exclusive possession of the party seeking to foreclose. Mortgages are routinely transferred through MERS, without being recorded. The notes underlying the mortgages, as negotiable instruments, are negotiated by mere delivery without a recorded assignment or notice to the borrower. A defendant has no method to reliably ascertain who in fact owns the note, within the narrow time frame allotted to file an answer.

In jurisdictions such as New York, CPLR 3018(b) provides that an affirmative defense is any matter “which if not pleaded would be likely to take the adverse party by surprise” or “would raise issues of fact not appearing on the face of a prior pleading”.

CPLR 3018(b) also lists some common affirmative defenses, although the list is not exhaustive. The list of affirmative defenses in CPLR 3018(b) are those which raise issues such as res judicata or statute of limitations which are based on facts not previously alleged in the pleadings.

“The defendant has the burden of proof of affirmative defenses, which in effect assume the truth of the allegations of the complaint and present new matter in avoidance thereof.” 57 NY Jur. 2d Evidence and Witnesses 165″.

To survive motion to dismiss or Summary Judgement, it is important that Pro Se Homeowners using “Standing” as a foreclosure defense also review their PSA in order to include missing or lack of assignments.

This defense will be based on “Conveyance from the Depositor to the Trust”.

Homeowners arguments under these defense will be based that the Trustee violated the terms of the trust by acquiring the note directly from the sponsor’s successor in interest rather than from the Depositor, for instance ABC, as required by the PSA.

In Article II, section 2.01 Conveyance of Mortgage Loans, the PSA requires that the Depositor deliver and deposit with the Trustee the original note, the original mortgage and an original assignment . The Trustee is then obligated to provide to the Depositor an acknowledgment of receipt of the assets before the closing date. PSA Article II, Section 2.01.

The rationale behind this requirement is to provide at least two intermediate levels of transfer to ensure the assets are protected from the possible bankruptcy by the originator which permits the security to be provided with the rating required for the securitization to be saleable.

Deconstructing the Black Magic of Securitized Trusts, Roy D. Oppenheim Jacquelyn K. Trask-Rahn 41 Stetson L. Rev. 745 Stetson Law Review (Spring 2012).

So to further the arguement, homeowners should argue that the assignment of the note and mortgage from original lender to Trustee which is called (A-D), rather than from the Depositor ABC violates section 2.01 of the PSA which requires that the Depositor deliver to and deposit the original note, mortgage and assignments to the Trustee.

In most cases, “if homeowner’s pleadings are in order”, meaning (The evidence submitted by homeowner that the note was acquired after the closing date and that assignment was not made by the Depositor), is sufficient to raise questions of fact in the court as to whether the Bank owns the note and mortgage, and usually will Deny motion to Dismiss(in non-juidical States) or preclude granting Bank’s summary judgment (in Judicial States).

The courts will usually find and conclude that the assignment of the homeowner’s note and mortgage, having not been assigned from the Depositor to the Trust, is therefore void as in being in contravention of the PSA.

For More Info How You Can Use Well Structured Pleadings Containing Facts and Case Laws Necessary To Win Your Foreclosure Defense Visit: http://www.fightforeclosure.net