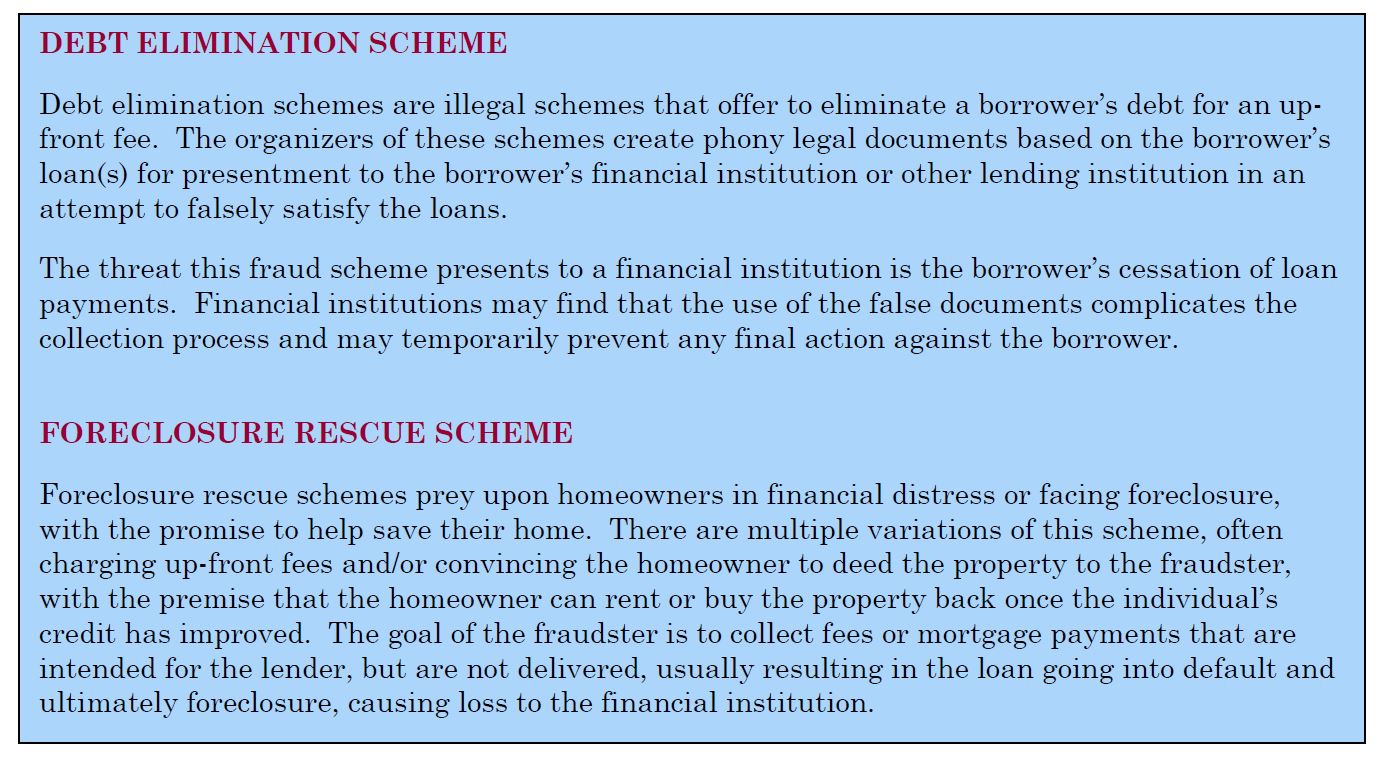

Tags

enforceability of judgment lien, Foreclosure, foreclosure defense, homeowners, involuntary liens, Lien, lien stripping, lien voidance, liens, Loan, Loan servicing, Mortgage loan, Mortgage modification, Mortgage servicer, Pro se legal representation in the United States, Property Lien Disputes, property liens, Real Estate Liens, Removing Liens, Types of Real Estate Liens, Unperfected Liens, voluntary liens

There are numerous methods for voiding questionable liens in any given mortgage. In this post, we’ll discuss an interesting decision by the U.S. Court of Appeals for the Ninth Circuit in Bankruptcy Adversary Proceeding.

This decision from the U.S. Court of Appeals for the Ninth Circuit poses a serious threat to mortgage companies that service mortgages of chapter 13 debtors. Mortgage servicers should be aware of the case’s implications and adjust their internal case monitoring procedures as necessary.

Consider a common situation. A borrower files a chapter 13 bankruptcy case, and her mortgage servicer files a proof of claim for the mortgage balance. The borrower then objects to the proof of claim based on some purported technicality: the signature was forged, the endorsement was improper, the servicer lacks standing to enforce the note, etc. For whatever reason, the mortgage servicer does not respond to this objection, and the claim is disallowed by default.

When this happens, the borrower will often attempt to leverage a favorable settlement, like a mortgage modification, by filing a lawsuit to void the mortgage under 11 U.S.C. § 506(d). This provision allows a bankruptcy court to void a lien if the lien secures a claim that is not “allowed.” Because the mortgage was “disallowed” by default due to the mortgage servicer’s failure to respond, this statute theoretically allows the court to void the mortgage altogether.

Courts generally do not void mortgages that are substantively valid but were disallowed because of a default. The most common solution in these situations is a settlement and a motion to reconsider the disallowance under 11 U.S.C. § 502(j). Bankruptcy courts may grant these motions for “cause” at their discretion, which is typically satisfied if the mortgage servicer can prove the substantive validity of the mortgage. See generally In re Oudomsouk, 483 B.R. 502, 513-14 (Bankr. M.D. Tenn. 2012). This works to everyone’s advantage: the mortgage servicer gets paid through the bankruptcy, and the debtor avoids the risk of post-bankruptcy foreclosure if the lien’s validity is ultimately upheld after the case concludes.

The decision of the U.S. Court of Appeals for the Ninth Circuit in In re Blendheim may change this result. 2015 WL 5730015 (9th Cir. Oct. 7, 2015). In Blendheim, the debtors owned a condominium with two mortgages. After filing chapter 7 and obtaining a discharge of their unsecured debts, the debtors immediately filed a chapter 13 case to restructure their mortgages on the condominium (this process is known as a “chapter 20”). HSBC, the senior servicer, filed a proof of claim for the senior mortgage, but the debtors objected because (a) HSBC attached only the deed of trust, and not the promissory note, to the proof of claim, and (b) one of the signatures on the note was purportedly forged.

For reasons unknown, HSBC did not respond to the objection, and the bankruptcy court entered an order disallowing HSBC’s claim by default. Five months later, the debtors brought an adversary proceeding to void the mortgage under 11 U.S.C. § 506(d). Almost eighteen months after the bankruptcy court disallowed HSBC’s claim, HSBC filed a motion to reconsider the disallowance. HSBC also challenged the debtors’ attempt to void the mortgage because the disallowance was not actually litigated; it was the result of a default. The bankruptcy court disagreed, finding that (a) HSBC had no good reason for failing to respond to the claim objection, and (b) the statute plainly permitted lien avoidance in these circumstances. After the bankruptcy court confirmed the debtors’ plan, which provided for payment of only the junior mortgage, HSBC appealed.

On appeal, HSBC raised three primary issues. First, it argued that Section 506(d) should not operate to void its mortgage, notwithstanding the plain language of the statute, when the order disallowing the claim was not actually litigated but was based on a default. Second, it argued that even if the lien were properly voided under Section 506(d), the result could not be permanent because the debtors, having recently received a discharge in their chapter 7 case, were not eligible for a discharge in their chapter 13 case. Third, it argued that by losing its lien because of a default order in the bankruptcy case, as opposed to a formal lawsuit, it was denied due process.

The court disagreed with HSBC on each issue. First, it held that lien avoidance was appropriate. HSBC cited cases where courts refused to void a mortgage when a claim was disallowed for being filed late. The court distinguished these cases, holding that a creditor who files a late proof of claim is not “actively participating in the case” and therefore cannot have its state law lien rights impacted. See generally Dewsnup v. Timm, 502 U.S. 410, 418-19. But when a creditor timely files a proof of claim then willfully fails to respond to the debtors’ objection to the claim, the situation is fundamentally different. According to the court, the Bankruptcy Code plainly allows permanent lien avoidance when a creditor, like HSBC, “just sle[eps] on its rights and refuse[s] to defend its claim.” Blendheim, 2015 WL 5730015, at *11.

Next, the court addressed HSBC’s second argument and held that lien avoidance was appropriate even though the debtors were not eligible for a discharge. Acknowledging a split of authority, the court clarified that discharge affects only personal liability, not the in rem rights of creditors, so the cases on which HSBC relied were distinguishable. Nothing in the Bankruptcy Code prohibits lien avoidance just because a borrower has no right to a discharge.

Finally, the court held that HSBC’s due process was not offended. HSBC received notice of the claim objection and had ample time to respond. Its failure to do so, while fatal to its lien, did not violate its due process rights.

What This Means for Mortgage Creditors

The Blendheim case may have serious implications for mortgage creditors. This situation is not an outlier: mortgage servicers commonly fail to respond to claim objections. his may be because of the quick deadline to respond to these objections or the use of separate legal counsel for handling administrative functions in bankruptcy versus defending adversary proceedings. Historically, when a claim is disallowed based on a creditor’s failure to respond to a claim objection, bankruptcy courts will grant a reconsideration motion under Section 502(j) if the creditor can prove the substantive validity of the mortgage.

After Blendheim, the result may be different. The Blendheim court, after all, did not seem to care about the underlying validity of HSBC’s claim. Instead, it focused on HSBC’s failure to respond without a good reason.

How does this Affect Mortgage Creditors

Mortgage servicers should be aware of this decision and should make sure that they are closely following the dockets of cases involving their borrowers in bankruptcy. If they don’t, they risk losing their mortgage lien, if any, altogether.

[The views expressed in this document are solely the views of the Author. This document is intended for informational purposes only and is not legal advice or a substitute for consultation with a licensed legal professional in a particular case or circumstance]

When Homeowner’s good faith attempts to amicably work with the Bank in order to resolve the issue fails;

If you are a homeowner already in Chapter 13 Bankruptcy with questionable liens on your property, you needs to proceed with Adversary Proceeding to challenge the validity of Security Interest or Lien on your home, Our Adversary Proceeding package may be just what you need.

Homeowners who are not yet in Bankruptcy should wake up TODAY! before it’s too late by mustering enough courage for “Pro Se” Litigation (Self Representation – Do it Yourself) against the Lender – for Mortgage Fraud and other State and Federal law violations using foreclosure defense package found at https://fightforeclosure.net/foreclosure-defense-package/ “Pro Se” litigation will allow Homeowners to preserved their home equity, saves Attorneys fees by doing it “Pro Se” and pursuing a litigation for Mortgage Fraud, Unjust Enrichment, Quiet Title and Slander of Title; among other causes of action. This option allow the homeowner to stay in their home for 3-5 years for FREE without making a red cent in mortgage payment, until the “Pretender Lender” loses a fortune in litigation costs to high priced Attorneys which will force the “Pretender Lender” to early settlement in order to modify the loan; reducing principal and interest in order to arrive at a decent figure of the monthly amount the struggling homeowner could afford to pay.

If you find yourself in an unfortunate situation of losing or about to lose your home to wrongful fraudulent foreclosure, and need a complete package that will show you step-by-step litigation solutions helping you challenge these fraudsters and ultimately saving your home from foreclosure either through loan modification or “Pro Se” litigation visit: https://fightforeclosure.net/foreclosure-defense-package/

If you have received a Notice of Default “NOD”, take a deep breath, as this the time to start the FIGHT! and Protect your EQUITY!

If you do Nothing, you will see the WRONG parties WITHOUT standing STEAL your home right under your nose, and by the time you realize it, it might be too late! If your property has been foreclosed, use the available options on our package to reverse already foreclosed home and reclaim your most prized possession! You can do it by yourself! START Today — STOP Foreclosure Tomorrow!