Tags

avoid foreclosure, Foreclosure, Foreclosure Crisis, foreclosure defense, Foreclosure Rescue Fraud, fraud prevention, HAMP, homeowners, Loan Modification, loan modification specialists, Making Home Affordable, Mortgage Coupon, Scam Artists

The most devastating foreclosure rescue fraud scams are those that not only promise a modification, but also trick homeowners into believing the lender has agreed to the terms. The party then instructs the homeowner to pay the “new” modified mortgage payments to them, and they will forward the payment to the lender. In reality, the third party takes the payments and the money never reaches the lender. Homeowners are often blindsided by foreclosure notices after many months of believing they are paying the “new” payments to the lender. The scammers often use copies of government logos and have names that are similar to real government programs.

“Your modification is approved! Send us your new payments”

Operation asserts the homeowner has been approved for a modification then steals the homeowner’s “new” mortgage payments.

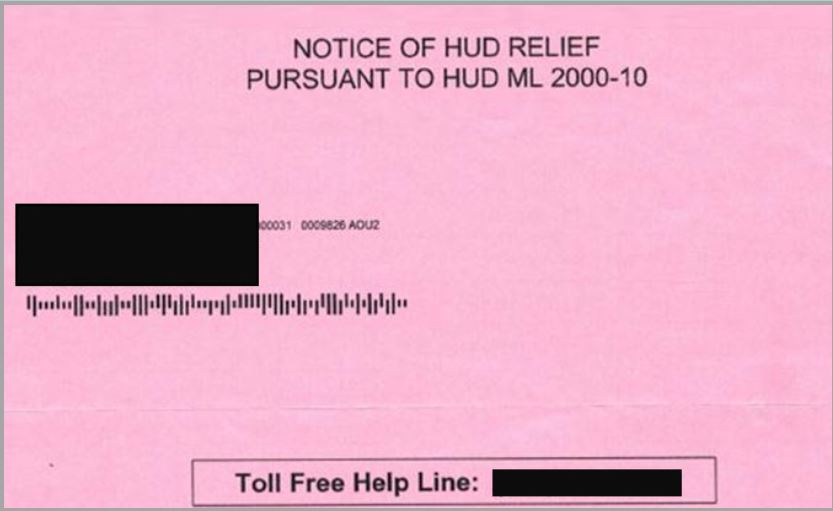

In one heartbreaking example, a woman from Lindenhurst, New York, received a flyer in the mail in early 2013 with the header “NOTICE OF HUD RELIEF.” Believing the flyer came from the government, she called the number on the flyer, and explained that she had tried working with her lender, but had no success. The third party told her that the lender was not being cooperative because they really just wanted to foreclose on her.

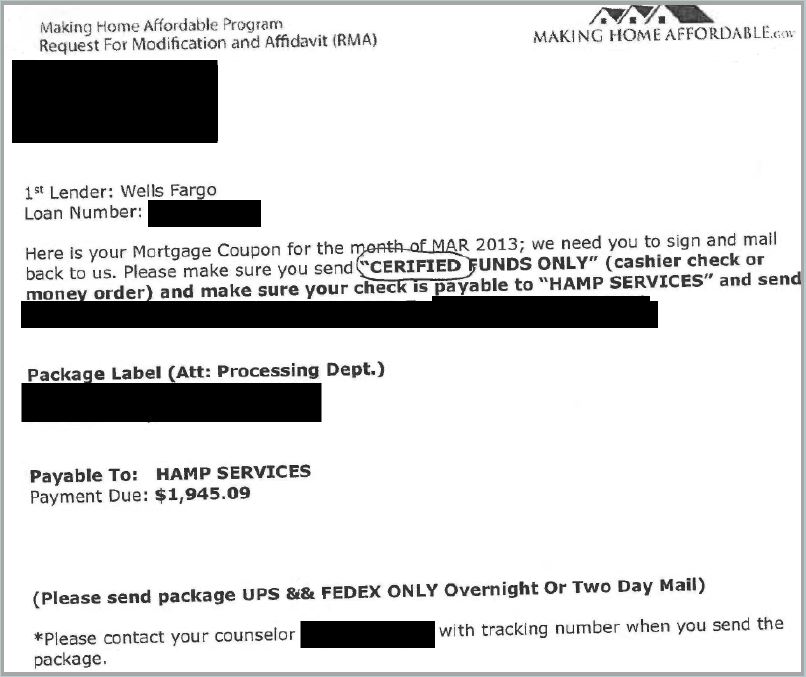

After sending the third party personal financial information, the homeowner quickly received a call back with some good news: they told her she was qualified for “HAMP through Making Home Affordable.” The homeowner was told she now had a mortgage that was a thousand dollars less than her current one, but this was a lie. Then the party told her there was one other thing she had to do before paying the new mortgage payment – pay a “reinstatement fee” of $6,000 that her lender required. Believing it was the final hurdle to reach relief, she sent in the $6,000. Then in March, April and May 2013, she made her new “trial payments” to the third party. They encouraged the homeowner to let them know when she sent the check so they could contact her lender with a tracking number.

Each month the homeowner received a “Mortgage Coupon” with what appeared to be various government logos on it, including the Making Home Affordable and Treasury logos. The homeowner stayed in close contact with the third party, diligently sending the checks.

In May 2013, the homeowner received a call from her lender, telling her she owed almost $30,000. She explained that she had received a loan modification and had already paid the reinstatement fee along with three mortgage payments. The lender representative told the homeowner that she may have gotten caught in a scam. Frantically, the homeowner called her main contact at the operation to which she had been sending her checks. The phone number was disconnected.

After losing almost $12,000, the homeowner is now facing foreclosure.

STATE LAWS

Ensure that Homeowners Are Covered Under State Laws Targeting Foreclosure Rescue Fraud: Many states have passed new laws to address foreclosure rescue scamming. However, some of these laws defined “homeowners” that the law was designed to protect too narrowly. For example, some state laws limit coverage to homeowners who are in default or foreclosure, and fail to reach many homeowners who are defrauded seeking to refinance their mortgage or are seeking mortgage relief because loss of job or unexpected medical costs. It is therefore important that state laws targeting foreclosure rescue fraud define homeowners broadly to cover fraud at any stage of the process.

As the foreclosure crisis grew, foreclosure rescue fraud – scams designed to capitalize on homeowners facing foreclosure by extracting thousands of dollars in exchange for empty promises of assistance – exploded and increased the pain of these homeowners. The proliferation of this type of fraud is not surprising. Homeowners with financial difficulties desperately need to find help to keep their homes and are vulnerable to scam artists posing as loan modification specialists, for example. Scam operators blanket television, radio, newspapers, and the internet with advertisements in English and Spanish, and also rely on street flyers, signs, billboards, and direct mail solicitation.

This saturation marketing, often filled with lies and exaggerations, plays on the trust of distressed homeowners. Scammers use high-pressure sales tactics and false guarantees of success to attract homeowners and to extract large upfront cash payments from homeowners, and then typically do little or no work to obtain the relief promised, essentially abandoning these homeowners. The homeowners not only lose the money they paid to the scam operation, but fall deeper into default and lose valuable time that could have been spent negotiating directly with their mortgage servicer or by going to free a HUD-approved housing counseling agency with true expertise in assisting homeowners in trying to save their homes.

As the foreclosure crisis was peaking, these scams replaced predatory lending as a major problem in the housing finance industry and scams resulted in what was known as the “second wave” of the foreclosure crisis. Indeed, many predatory lending operations morphed into foreclosure rescue scam entities.

“We volunteer all our hours with no payment.”

Alleged “Non-profits” Referring Homeowners to “Law Groups”

Attorney involvement in scams is growing and appears to be an effective means of ensnaring victims, but some homeowners still approach attorneys with skepticism. Attorneys, or someone pretending to be affiliated with an attorney, attempt to ease this skepticism by involving a “non-profit.” Anyone involved in preventing foreclosure or foreclosure rescue fraud knows the best resource for homeowners is a FREE, HUD – approved housing counseling agency.

The problem is that not every organization who claims to fit that description actually does. Some “non-profits” operate as lead generation agencies, gaining the trust of vulnerable homeowners. A search for “.org” in the Database produces over 1400 complaint hits. Homeowners meet with these “non-profits” and things appear to be in order. They aren’t asking for any money, the people seem very nice, and they begin to look over various mortgage documents, free of charge. Providing what appears to be a free service, the “non-profit” can make the homeowner feel at ease and also invested in the process. Once the homeowner is invested, the next level of the scam begins.

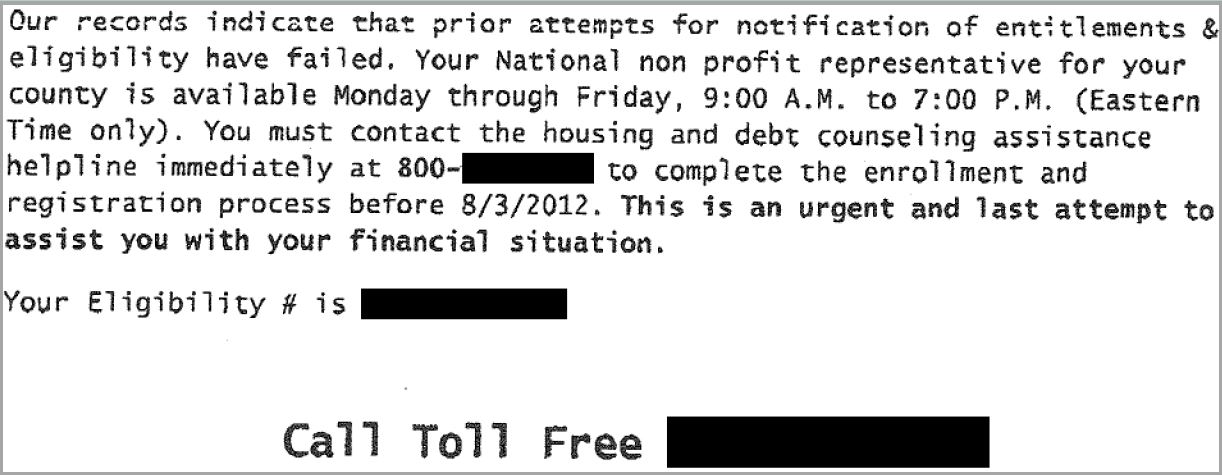

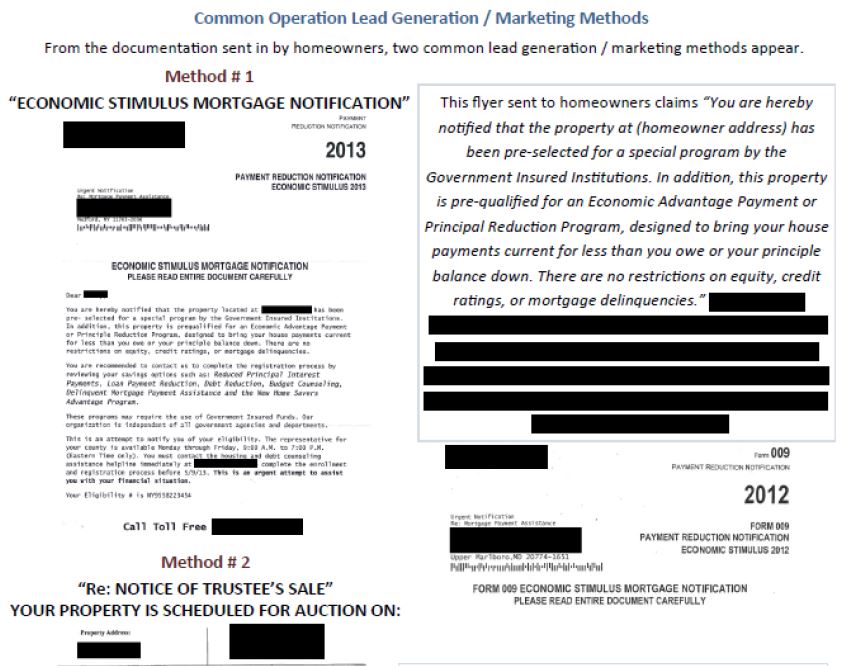

One homeowner from Rosedale, New York, began working with one of these “non-profits” in early 2013. She had received a flyer in the mail with the headline, “Economic Stimulus Mortgage Notification” that read, in part: “You are hereby notified that the property at (her address) has been pre-selected for a special program by the Government Insured Institutions. In addition, this property is pre-qualified for an Economic Advantage Payment or Principal Reduction Program, designed to bring your house payments current for less than you owe or your principle balance down. There are no restrictions on equity, credit ratings, or mortgage delinquencies.” The flyer said to contact “Your National non-profit representative” because this is the “last attempt to assist you with your financial situation.”

The homeowner was in need of a modification, so she called the “non-profit” listed on the top of the flyer. After working with the “non-profit” for a while, they told her that they did “all that they could,” and she needed to talk to “(Name withheld) Law Group.” This “Law Group” advertised that they “fight the bank.” They assured her that nothing could happen to her home as long as they were defending her, saying “(her lender) will not take her case until 2016,” giving her some much needed breathing room. After paying four thousand dollars to the “Law Group” and following weeks of empty promises, she was blindsided by a letter telling her that her mortgage was put into foreclosure just a few months after she began working with the “non-profit.”

To keep skeptical homeowners on the hook, the “non-profit” will stay involved throughout the process, assuring the vulnerable homeowner everything is fine. The “Law Group” extracts numerous fees from the homeowner, often saying, “the bank can’t do anything as long as we represent you.” Often in the end, the “non-profit” was started by the same attorney (or non-attorney) who started the “Law Group.” The homeowner loses thousands of dollars and is left wondering, if a “non-profit” will scam them, is there anyone they can trust?

“You’re eligible to join our lawsuit”

Fake Mass Joinder & Other Lawsuits

On average, complaints that allege some type of attorney involvement have produced greater losses per homeowner than all other complaints. While attorneys can be involved in any type of foreclosure rescue fraud, they are uniquely capable of tricking homeowners into believing they can get involved in fake mass joinder or other lawsuit against a lender. The lawsuit schemes can prove to be even more painful for homeowners because they often involve two parts: first a fee for a “forensic audit” to see if the homeowner is eligible to join the suit, then another fee to join the suit. Most promise very impressive results, like the homeowner who was told she could “join a class action lawsuit against her lender. Once this was settled she was guaranteed $75,000.”

The final selling point for many of these lawsuits is the assurances made to homeowners that nothing can happen to their homes as long as they are part of the suit. Some attorneys advise homeowners to stop paying their mortgage and instead pay monthly retainer fees to them. Month after month, homeowners pay the fee, believing the attorney is fighting for them. In the worst cases, the homeowner doesn’t realize the attorney is actually providing no service at all until a foreclosure notice arrives.

One senior citizen from Williamstown, New Jersey, was contacted by a group of attorneys who guaranteed him a loan modification for just over four thousand dollars. After they allegedly reviewed his documents and made “headway” with the bank regarding a loan modification, they informed him that he was eligible to join a lawsuit against his lender. The suit included over twenty thousand homeowners and they assured him that the lender would settle. At that point the homeowner began making monthly retainer payments of just over a thousand dollars, for eleven months, for a suit that never happened. On top of all of that, the attorneys advised him to stop making his mortgage payments.

Attorneys Engaged in Foreclosure Rescue Fraud

Results in Higher Homeowner Losses

These “Law Groups” or “Law Networks” claim to include hundreds of lawyers from around the country and claim that they will connect homeowners to lawyers in their home state.

The Domino Effect of Foreclosure Rescue Fraud

The average dollar figure a homeowner loses in Attorney involved Scam is around $3600, and $2850 on non-Attorney Scams. This dollar figure does not take into account the potential domino effect of foreclosure and homelessness these foreclosure rescue scams can have.

Homeowners may lose over $3,200 in cash payments to a scammer, but then can end up losing hundreds of thousands of dollars more because their homes fall into foreclosure as a direct result of the scam.

At Reno Nevada Foreclosure Prevention Event: One story was particularly memorable.

It involved a homeowner named Bill, and his Dad. After the Lawyers’ Committee’s presentation, Bill’s father, who is in his 80’s, came to the Lawyers’ Committee’s table and asked that we speak to his son, who has medical issues and has difficulty walking. Bill opened his rolling filing cabinet, where he kept his mortgage documents meticulously categorized, and pulled out a large stack of papers from the section labeled “Name Withheld Law Center.”

Bill described his experience as follows: Towards the end of 2009, he received a flyer in the mail with the subject line, “RE: Obama Administration’s Homeowner Affordability and Stability Plan.” This “Modification PROGRAM” said he may be eligible for the “Governmental Economic Stimulus Act of 2009.” The flyer contained Bill’s name, address, and exact loan amount. There was a place for him provide his email address and phone number so the group responsible for the flyer could contact him.

After receiving the flyer, Bill began talking to the “Name Withheld Law Center” associated with it. He pulled out the contract that was sent to him, which contained a recognized attorney’s name because several state Attorneys General had obtained cease and desist orders against that attorney. The attorney doesn’t appear to have ever been licensed in Nevada, and while he had been licensed in California, his license was suspended in early 2013 for misconduct in three loan modification cases.

Bill paid just under two thousand dollars for a loan modification that he never received.

Bill’s Dad sat behind him and watched closely as Bill spoke about his experience with the “Name Withheld Law Group,” and about his life in general. Bill’s Dad’s eyes would well up from time to time.

This story is so moving because it accurately describes the effects of the foreclosure crisis and foreclosure rescue frauds on struggling homeowners. The vast majority of people looking for help to modify their mortgages don’t have an exploding rate mortgage. They, like Bill, have a normal 30 year fixed mortgage that they could afford pre-recession. Bill bought his home for around $280,000 in 2005, putting down a full 20%, which now is worth somewhere between $130,000 and $160,000. When he bought the home, like many Americans, he couldn’t foresee the worst recession since the Great Depression and the simultaneous housing collapse.

These homeowners became prime targets for foreclosure rescue scammers, having been blindsided by the recession and believing the guarantees of success by those who promised to save their homes.

Military Scams

Fake Military Discounts in Foreclosure Rescue Fraud

“We have a discount for military members & their families”

With more than three years of data in the Database – including over thirty-eight thousand complaints and over eighty-four million dollars in total reported losses – sadly there is no shortage of disturbing stories. From the dying cancer patient who was scammed out of thousands of dollars while he was trying to make sure his widow could afford the mortgage when he was gone, to the single woman who took in her sister’s four children after she passed away who was scammed into believing she was part of a fake lawsuit, then threatened by the same attorneys who scammed her after she complained. One type of troubling scam appearing over the past few years is the “Military Discount” targeted to active military service members and their families.

One man, a senior citizen from Fort Worth, Texas, had hit a rough patch when he was solicited by a third party. At that point, he was one month behind on his mortgage payments and was working hard to keep up. The company guaranteed him a loan modification for $1,600. He was hesitant to pay so much money when he was already struggling to stay current on his mortgage. Sensing his hesitation with the original price, the third party asked if he, or anyone in his family, was currently serving the country. After he explained that his daughter was currently serving the country in Iraq, the third party thanked him for his daughter’s service and told him that he was eligible for a military discount of $300. Lowering the price just enough to make it bearable for him, he paid the fee. Months went by with no results and no refund. The damage was not done there. The company advised him that he needed to stop making his mortgage payments in order to get the loan modification, so he did. He went from being just one month behind on his mortgage when he started working with this operation, to his home being sold in foreclosure.

State laws targeting foreclosure rescue fraud should define covered homeowners broadly, as those who seek foreclosure relief services can easily be defrauded before an actual foreclosure or mortgage payment default, thereby excluding them from the coverage of otherwise applicable consumer protection laws. Homeowners who are not yet in foreclosure and who have not fallen behind on mortgage payments should be encompassed in laws regulating third-party services in this area.

Some state and federal laws prohibiting foreclosure rescue fraud directly or indirectly (including through prohibitions on deceptive business practices) are only enforceable by government entities.

When Homeowner’s good faith attempts to amicably work with the Bank in order to resolve the issue fails;

Home owners should wake up TODAY! before it’s too late by mustering enough courage for “Pro Se” Litigation (Self Representation – Do it Yourself) against the Lender – for Mortgage Fraud and other State and Federal law violations using foreclosure defense package found at https://fightforeclosure.net/foreclosure-defense-package/ “Pro Se” litigation will allow Homeowners to preserved their home equity, saves Attorneys fees by doing it “Pro Se” and pursuing a litigation for Mortgage Fraud, Unjust Enrichment, Quiet Title and Slander of Title; among other causes of action. This option allow the homeowner to stay in their home for 3-5 years for FREE without making a red cent in mortgage payment, until the “Pretender Lender” loses a fortune in litigation costs to high priced Attorneys which will force the “Pretender Lender” to early settlement in order to modify the loan; reducing principal and interest in order to arrive at a decent figure of the monthly amount the struggling homeowner could afford to pay.

If you find yourself in an unfortunate situation of losing or about to lose your home to wrongful fraudulent foreclosure, and need a complete package that will show you step-by-step litigation solutions helping you challenge these fraudsters and ultimately saving your home from foreclosure either through loan modification or “Pro Se” litigation visit: https://fightforeclosure.net/foreclosure-defense-package/