Tags

When a Homeowner is approaching foreclosure on his/her property, there are numerous things the homeowner should bear in mind.

(This is Not Intended to be a Legal Advice and Nothing on this Post is to be Construed a Legal Advice).

I. HOMEOWNERS EXPECTATIONS

A. Realistic Expectations – Homeowners Should Expect to See ALL Original Mortgage Closing Documents.

1. Keep the Home – at some point lender will in all probability be entitled to foreclose either for the full amount due, small reduction or large reduction

2. Short Sale – No Buyers/No Money

3. Modify Mortgage – No Mandatory Programs:

Right now there is no program available that will compel a lender to renegotiate a loan, and you cannot force a cram down in bankruptcy. The program Congress passed in July effective Oct. 1, 2008 is a voluntary lender program. In order to be eligible, one must live in the home and have a loan that was issued between January 2005 and

June 2007. The provisions was later amended during the meltdown to include struggling homeowners in past few years. Additionally, the homeowner must be spending at least 31% of his gross monthly income on mortgage debt. The homeowner can be current with the existing mortgage or in default, but either way the homeowner must prove that he/she will not be able to keep paying their existing mortgage and attest that it is not a deliberate default just to obtain lower payments.

All second liens must be retired or paid such as a home equity loan or line of credit, or Condo or Home Owner Ass’n lien. So if the homeowner has a 2nd mortgage, he is not eligible for the program until that debt is paid. And, the homeowner cannot take out another home equity loan for at least five years, unless to pay for necessary upkeep on the home. The homeowner will need approval from the FHA to get the new home equity loan, and total debt cannot exceed 95% of the home’s appraised

value at the time. This means that the homeowner’s present lender must agree to reduce his payoff so that the new loan is not greater than 95% of appraised value. For example, if the present loan in default is $200,000.00 but the home appraises for $150,000.00 the new loan cannot exceed a little over $142,000.00, and the present lender has to agree to reduce the mortgage debt to that amount. You can contact your

current mortgage servicer or go directly to an FHA-approved lender for help. These lenders can be found on the Web site of the Department of Housing and Urban Development: http://www.hud.gov/ As I pointed out above, this is a voluntary program, so the present lender must agree to rework this loan before things can get started.

Also, homeowners should contact the city in which they reside or county to see if they have a homeowner’s assistance program. West Palm Beach will give up to $10,000 to keep its residents from going into default.

Over the years, we have seen FANNIE MAE and FREDDIE MAC announced that they will set aside millions to rewrite mortgage terms so its homeowner can remain in their home. Given the outcome of numerous modification attempts and denials of loan modifications, I do not know whether the terms or conditions for the modification was for the benefit of the lender or the borrower, though any prudent person will conclude it is for the former.

Bank of America, which includes Countrywide, and JP Morgan Chase also announced earlier, that they will set aside millions to rewrite mortgage terms so its home mortgagors can remain in their homes.

4. Stay in the home and try to defeat the foreclosure under TILA RESPA and Lost Note, etc.

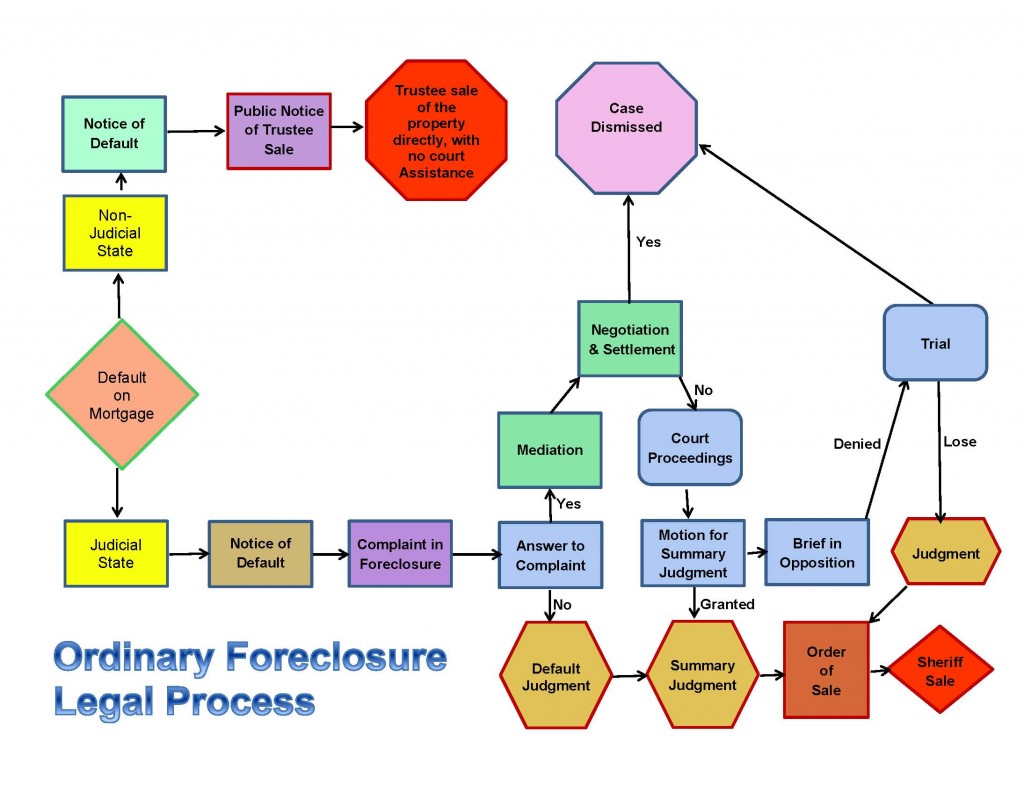

II. DEFENDING A MORTGAGE FORECLOSURE

A. Homeowners Should Prepare Themselves for Litigation. (Using Foreclosure Defense Package found at http://fightforeclosure.net

1. Homeowners needed for 4 Events

a. Answer Interrogatories, Request to Produce

b. Homeowner’s Deposition

c. Mediation – Homeowners should understand that mortgage cases like most cases have a high percentage of settling.

d. Trial

2. Cases move slowly even more now because of the volume of foreclosures and the reduction of court budgets.

3. Cases move on a 30/60/90 day tickler system – one side does something the other side gets to respond or sets a hearing.

4. If the Homeowner fails to do any of the above timely or fails to appear for any of the events, he/she may lose his case automatically.

5. Because of the way the system works the Homeowner may not hear from the court for several weeks or months – that does not mean that the court is ignoring the case – that is just how the system works but feel free to call or write and ask questions.

6. If you have a lawyers, keep in contact with the lawyer and advise of changes in circumstances/goals and contact info. If you are representing yourself keep in contact with the court clerk and docket sheet.

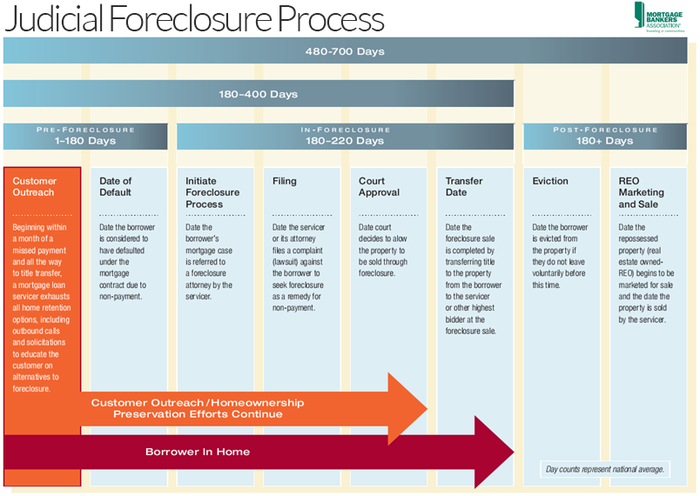

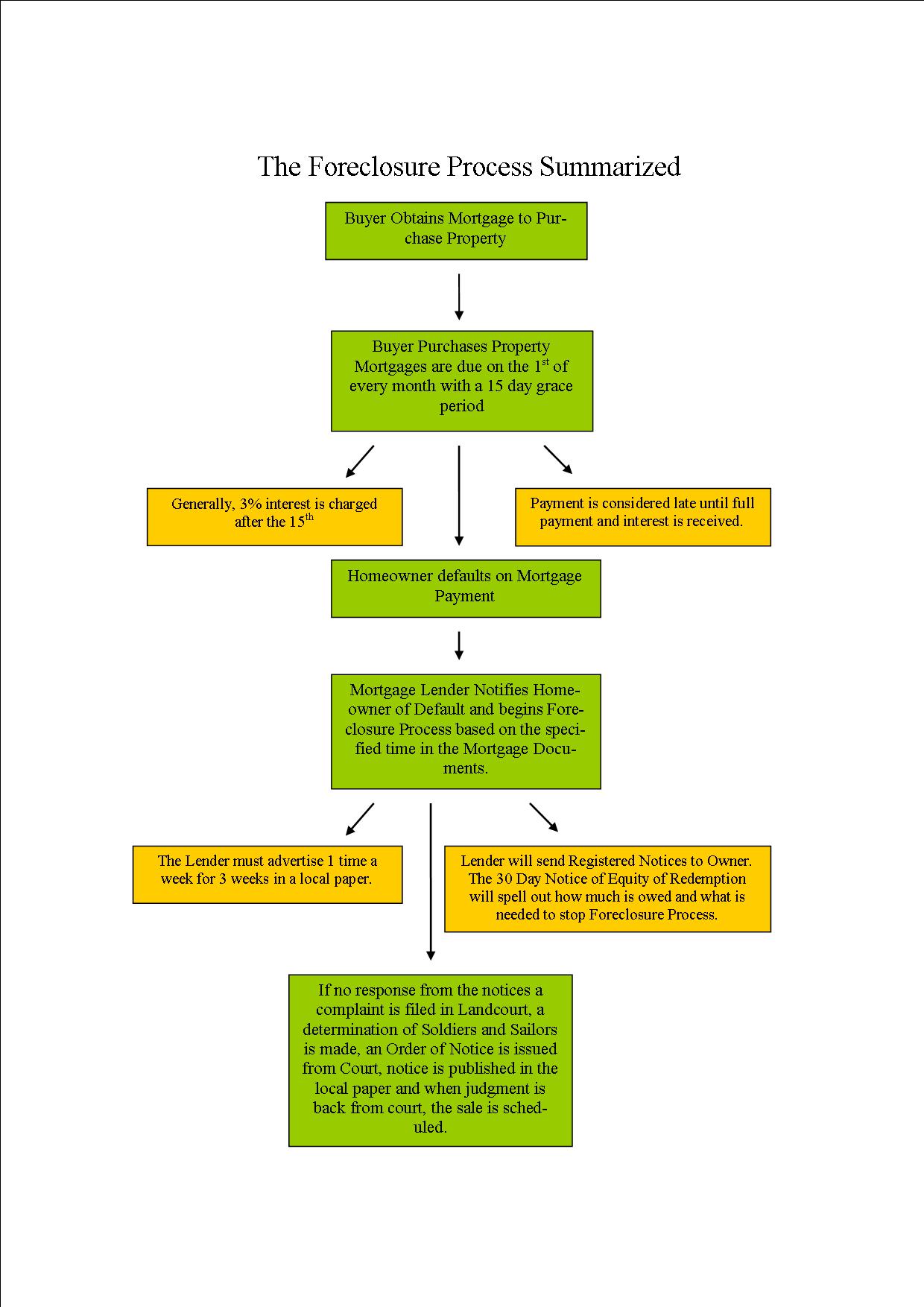

7. Home in places like Florida as well as other States should understand that a Foreclosure is – The legal mechanism by which the mortgage lender ends the “equity of redemption” by having a judge determine the amount of debt and a specific date, usually in 30 or 60 days to pay the money, and if not paid by that date, the judge allows the clerk to auction the property. Fla. Stat. §697.02, which changed the old English common law notion that the mortgage gave the lender an interest in the borrower’s land, makes the mortgage a lien against title. Fla. Stat. §45.0315 tells the mortgage lender that the borrower has the right to redeem the property after final judgement of foreclosure, until shortly after the clerk conducts the auction, when the clerk issues the certificate of sale. The client still has legal, recorded title to the property throughout the foreclosure process until the clerk issues the certificate of sale (ends redemption) then the certificate of title (transfers title) 10 days after the clerk’s sale if no objection to sale filed.

8. Deficiency – The judgement will determine the amount of the debt. A deficiency is the difference between the debt owed and the fair market value of the home at the date of the clerk’s sale.

9. Homeowners without Attorneys should knows that the complaint must be answered in 20 days or he/she could automatically lose, unless he/she either files a motion to dismiss with the court or files a motion for leave to extend time to answer “showing good cause” why the answer was not given when due. In either event, the motion needs to be filed before the due date.

B. Read the Summons Complaint, the Mortgage, Note and the Assignments.

1. Check the Summons for proper service and if not prepare a motion to quash.

2. The vast majority of foreclosure complaints are filed by foreclosure factories and will generally have 2 counts – reestablish a lost mortgage and note and foreclose. Fertile area for a motion to dismiss (see the sample motions to dismiss in the package at http://fightforeclosure.net)

3. Homeowners with the foreclosure defense package at http://fightforeclosure.net can be assured that he/she will find a basis to make a good faith motion to dismiss most of the form mortgage foreclosure complaints.

4. Homeowners should endeavor to set the motion to dismiss for hearing 30 days out or so. Otherwise, let the opposing counsel’s office set the hearing.

5. Cannot reestablish a negotiable instrument under Fla. Stat. §71.011 must be Fla. Stat. §673.3091 and person suing to foreclose must have the right to foreclose and reestablish when he files the lawsuit – post lawsuit assignments establish the lender did not own at time of suit unless pre-suit equitable assignment. See: Mason v. Rubin, 727 So.2d 283 (Fla. 4th DCA 1999); National Loan Invest. v. Joymar Ass.,

767 So.2d 549 (Fla. 3rd DCA 2000); State Street Bank v. Lord, 851 So.2d 790 (Fla. 4th DCA 2003). For an example of how far courts will go to find mortgages enforceable see: State Street Bank v. Badra, 765 So.2d 251 (Fla. 4th DCA 2000), Mtg. Elec. Regis. Sys. v. Badra, 4D07-4605 (Fla. 4th DCA 10-15-2008).

C. Answer Affirmative Defenses and Counterclaim

1. A general denial of allegations regarding the lost note is not enough. The foreclosure mill must specifically deny lost note allegations (see forms in the package at http://fightforeclosure.net).

2. Generally speaking Homeowners should be prepared to file a counterclaim with the affirmative defenses because the lender then cannot take a voluntary dismissal without court order and the

SOL (Statutes of Limitation) may expire for the TILA claims. You have more control over the suit, but now you must pay a filing fee for the counterclaim.

3. If Homeowners are not familiar with specific RESPA Yield Spread defense, they can review some of the articles in this blog because in 1995 or so FRB changed the regulations so that made the payment is not automatically a kickback for the referral of business (In my opinion this was the beginning of the mortgage mess we have now). Homeowners using Foreclosure Defense package found at http://fightforeclosure.net will find samples of well structured RESPA Yield Spread premium (YSP) defense within the package.

D. Discovery

1. In order to take more control over the case and shake up things from the beginning, homeowners using the Foreclosure Defense package at http://fightforeclosure.net should send out well constructed foreclosure Interrogatories and Request to Produce with the Answer. Homeowners in certain cases may also serve Notice of Taking P’s Deposition DT. See package for samples and for the wording. That will give Homeowners more control over the case, putting the Foreclosure Mill on its toes from the word go.

2. Usually the lenders firm will call and ask 3 things 1) “What do you really want – an extended sale date?” 2) “Can I have more time to answer discovery?” 3) “Can I have more time to find you a witness?” Answer to 1) “I really want to rescind the purported loan – do you want to agree to a rescission?” 2 & 3) “No problem as long as you

agree not to set any dispositive motion for hearing until a reasonable time after I get the discovery or take the deposition so that I can prepare and I do not incur an expedited deposition fee.”

3. Lender Depositions: There is rarely a need to actually depose the lender because their testimony rarely varies , and it can work to your disadvantage because if you actually take the pre-trial deposition for the lender or his servicing agent, you will have preserved the lender’s testimony for trial. If for some reason the lender cannot appear on the scheduled trial date, he will either take a voluntary dismissal or settle

the case. It is easier for Homeowners to win their cases or forced favorable settlements when the lender’s representative could not appear at the trial or meet up with the court deadlines.

4. Closing Agents depositions: Again, There is rarely a need to actually depose the closing because the testimony rarely varies and you will have preserved the testimony for trial. They either say: 1) “I do not remember the closing because I do hundreds and this was years ago, but it is my regular business practice to do A B and C and I followed my regular practice for this loan.” – the most credible and the usual

testimony; 2) 1) “I remember this closing and I gave all the required disclosures to the consumer and explained all the documents.” Not credible unless they tie the closing to an exceptional memorable event because the closing generally took place years and hundreds of closings earlier and you can usually catch them on cross “So name the next loan you closed and describe that closing” 3) 1) “I remember this closing and I gave the consumer nothing and explained nothing. Rare – though this has happened at one time. You do need the closing file so you can do a notice of production to non-party.

5. Mortgage Broker depositions: Again, there is rarely a need to actually depose the broker because the testimony rarely varies and you will have preserved the testimony for trial. They either say: 1) “I do not remember this borrower because I do hundreds and this was years ago, but it is my regular business practice to do A B and C and I followed my regular practice for this loan.” – the most credible and the usual

testimony; 2) 1) “I remember this borrower and I gave all the required disclosures to the consumer and explained all the documents.” Not credible unless they tie the borrower to an exceptional memorable event. 3) 1) “I remember this closing and I broke the mortgage brokerage laws and violated TILA. Rare – this has never

happened. You do need their application package so do a notice of production to nonparty.

6. Compare the documents in all of the closing packages: Lender’s underwriting, closing agent and mortgage broker. I have seen 3 different sets of documents. One in each package. The key is what was given to the Homeowner at the closing.

7. Homeowner’s deposition – very important if the case turns on a factual issue of what happened at the closing. Homeowner needs to be very precise and sure as to what occurred at the closing.

E. Motions to Strike

1. Lender’s counsel frequently moved to strike the defenses. These motions are generally not well taken, and simply prolong the case. See Response to Motion to Strike.

2. There are two rules for striking a party’s pleadings; one arises under Fla. R. Civ. P. 1.140(f), and the other arises under Fla. R. Civ. P. 1.150.

3. Under Rule 1.140(f): “A party may move to strike . . . redundant, immaterial, impertinent, or scandalous matter from any pleading at any time.” Fla. R. Civ. P. 1.140(f).

4. Under Rule 1.150, a party can move to strike a “sham pleading” at any time before trial. This rule requires the Court to hear the motion, take evidence of the respective parties, and if the motion is sustained, allows the Court to strike the pleading to which the motion is directed. The Rule 1.150(b) Motion to Strike as a sham must be verified and must set forth fully the facts on which the movant relies and may be supported by affidavit.

F. Lender’s Motions for Summary Judgment

1. The lender will no doubt file a motion for summary judgment, usually including the affidavit of a servicing agent who has reviewed the file, many times not attaching the documents that he is attesting are true and accurate. The court should rule that the affidavits are hearsay and lack a foundation or predicate because the affiant is summarizing the legal import of documents usually trust agreements and servicing agreements, without attaching copies. See another post in this Blog that deals with the Summary Judgment memorandum for the legal basis to object to the lender’s summary judgment.

III. TRUTH IN LENDING

A. Overview

1. Congress passed TIL to remedy fraudulent practices in the disclosure of the cost of consumer credit, assure meaningful disclosure of credit terms, ease credit shopping, and balance the lending scales weighted in favor of lenders. Beach v. Ocwen, 118 S.Ct.1408 (1998), aff’g Beach v. Great Western Bank, 692 So.2d 146,148-149 (Fla.1997), aff’g Beach v. Great Western, 670 So.2d 986 (Fla. 4th DCA 1996), Dove v. McCormick, 698 So.2d 585, 586 (Fla. 5th DCA 1997), Pignato v. Great Western Bank, 664 So.2d 1011, 1013 (Fla. 4th DCA 1996), Rodash v. AIB Mortgage, 16 F.3d 1142 (11th Cir.1994). {1}

2. TIL creates several substantive consumer rights. §1640(a)(1) gives consumers actual damages for TIL errors in connection with disclosure of any information. §1640(a)(2)(A)(iii) gives consumers statutory damages of twice the amount of any finance charge, up to $2,000.00 for errors in connection with violations of §1635 or §1638(a)(2) through (6), or (9), and the numerical disclosures, outside of the $100.00 error tolerance. See Beach, 692 So.2d p.148-149, Kasket v. Chase Manhattan Bank,

695 So.2d 431,434 (Fla.4 DCA 1997) [Kasket I,] Dove, p.586-587, Pignato, p.1013, Rodash, p.1144. {2} See also §1605(f)(1)(A). {3}

3. §1635(a) allows a consumer to rescind home secured non-purchase credit for any reason within 3 business days from consummation. If a creditor gives inaccurate required information, TIL extends the rescission right for 3 days from the date the creditor delivers the accurate material TIL disclosures and an accurate rescission notice, for up to three years from closing. Pignato, p.1013 (Fla. 4th DCA 1995) (“TILA permits the borrower to rescind a loan transaction until midnight of the third business day following delivery of all of the disclosure materials or the completion

of the transaction, whichever occurs last.”]. See also: Beach, cases, supra, Rodash, Steele v Ford Motor Credit, 783 F.2d 1016,1017 (11th Cir.1986), Semar v. Platte Valley Fed. S&L, 791 F.2d 699, 701-702 (9th Cir. 1986).

———————————————

{1} All 11th Circuit TIL decisions and pre- 11th Circuit 5th Circuit cases are binding in Florida. Kasket v. Chase Manhattan Mtge. Corp., 759 So.2d 726 (Fla. 4th DCA 2000) (Kasket, II) [11th Circuit TIL decisions binding in Florida]

{2} §1640’s last paragraph has the §1640(a)(2) damage limit: “In connection with the disclosures referred to in section 1638 of this title, a creditor shall have a liability determined under paragraph (2) only for failing to comply with the requirements of section 1635 of this title or of paragraph (2) (insofar as it requires a disclosure of the “amount financed”), (3), (4), (5), (6), or (9) of section of this title…”

{3} This subsection provides that numerical disclosures in connection with home secured loans shall be treated as being accurate if the amount disclosed as the finance charge does not vary from the actual finance charge by more than $100, or is greater than the amount required to be disclosed. See also Williams v. Chartwell Financial Services, Ltd., 204 F.3d 748 (7th Cir. 2000). (Over-disclosure can also be a violation under certain circumstances.)

———————————————-

4. HOEPA loans (Also called a §1639 or Section 32 loan.) TIL requires additional disclosures and imposes more controls on loans that meet either the “T-Bill Trigger” or “Points and Fees Trigger” set forth at §1602(aa). §1639, Reg Z 226.31 & Reg Z 226.32, require the creditor for a §1602(aa) loan to give additional early [3 days before consummation] disclosures to the consumer and prohibits loans from containing certain terms [i.e. a prohibition on certain balloon payments]. It also has

a special actual damage provision at §1640(a)(4). (HOEPA can make a lender a TIL creditor for the first HOEPA loan). (The trigger for Florida’s Fair Lending Act is based on the HOEPA triggers. This may affect a larger number of loans and may provided post 3 year rescission. See Fla. Stat. §494.00792(d)).

5. Zamarippa v. Cy’s Car Sales, 674 F.2d 877, 879 (11th Cir. 1982), binding in Florida under, Kasket II, hods: “An objective standard is used to determine violations of the TILA, based on the representations contained in the relevant disclosure, documents; it is unnecessary to inquire as to the subjective deception or misunderstanding of particular consumers.”

6. In 1995, Congress created a defensive right to rescind when a lender sues a consumer to foreclose the mortgage. See §1635(a) & (i)[1995], Reg. Z 226.23(a)(3) & (h) [1996]. The §1635(i) amendment triggers the consumer’s defensive right to rescind when the creditor overstates the amount financed by more than $35.00, or errs in the Notice of Right to Cancel form, and the claim is raised to defend a foreclosure. See also Reg Z 226.23(h).

7. Florida defers to the FRB’s interpretation of TIL and its own regulations. Beach, 692 So.2d p.149, Pignato, p.1013, Kasket, I p.434. The U.S. Supreme Court requires deference to the FRB’s interpretations of the Statute and its own regulations. Ford Motor Credit Co. v. Milhollin, 444 U.S. 555, 560, 565-570 (1980). TIL is remedial, so courts expansively and broadly apply and interpret TIL in favor of the consumer.

Rodash, p. 1144; Schroder v. Suburban Coastal Corp., 729 F.2d 1371, 1380 (11th Cir. 1984); Kasket II, W.S. Badcock Corp. v. Myers 696 So.2d 776, p. 783 (Fla. 1st DCA 1996) adopting Rodash, p.1144: “TIL is remedial legislation. As such, its language must be liberally construed in favor of the consumer.”

8. Pignato, p. 1013 also holds: “Creditors must strictly comply with TILA. Rodash, 16 F.3d at1144; In re Porter, 961 F.2d 1066, 1078 (3d Cir. 1992). A single violation of TILA gives rise to full liability for statutory damages, which include actual damages incurred by the debtor plus a civil penalty. 15 U.S.C.A. §§1640(a)(1)(2)(A)(i). Moreover, a violation may permit a borrower to rescind a loan transaction, including a rescission of the security interest the creditor has in the borrower’s principal dwelling. 15 U.S.C.A. §§1635(a).” See also the Beach cases.

This is in harmony with W.S. Badcock, p. 779, which holds: “Violations of the TILA are determined on an objective standard, based on the representations in the relevant disclosure documents, with no necessity to establish the subjective misunderstanding or reliance of particular customers.”

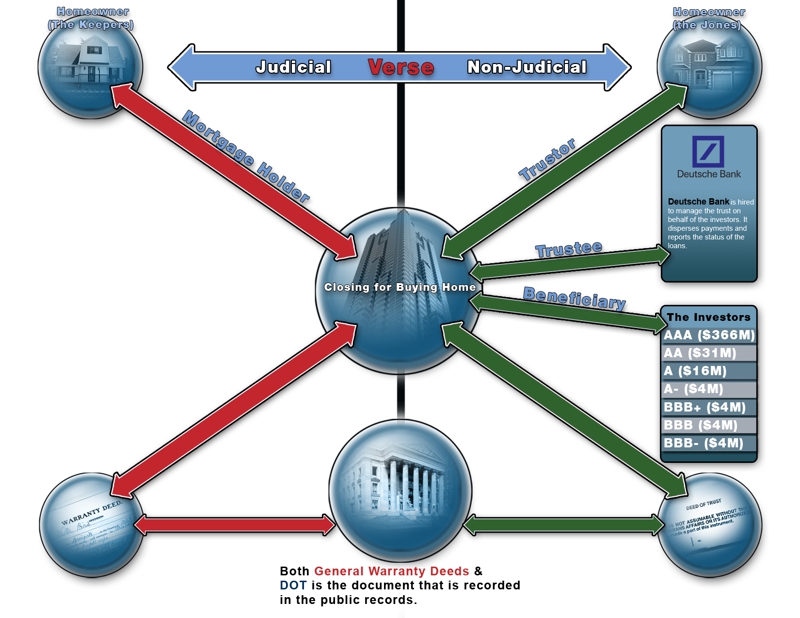

B. Assignee Liability

1. §1641(a)(1) and §1641(e)(1)-(2) provides that assignees are liable for §1640(a) damages if the disclosure errors are apparent on the face of the disclosure statement and other documents assigned. Congress statutorily designated the TIL disclosure statement, the TIL notice of right to cancel, and any summary of the closing costs as documents assigned. See §1641(e)(2).

2. §1641(c) provides that assignees are liable for §1635 rescission regardless of the apparent on the face of the “documents assigned” standard for damages claims. Belini v. Washington Mut. Bank, FA, 412 F.3d 17, p. 28 (1st Cir. 2005).

3. You must make sure that you rescind as to the correct “creditor.” See: Miguel v. Country Funding Corp., 309 F.3d 1161 (9th Cir. 2002).

C. Right to Rescind

1. Each consumer with the right to rescind must receive one [1] copy of the correct TIL Disclosure Statement and two [2] copies of a correct Notice of Right to Cancel form. If not, the consumer can rescind for up to 3 years after closing. See: Reg Z 226.23(a)(3), fn 48; Beach v. Ocwen, 118 S.Ct.1408 (1998), aff’g Beach v. Great Western Bank, 692 So.2d 146,148-149 (Fla.1997), aff’g Beach v. Great Western Bank, 670 So.2d 986 (Fla. 4th DCA 1996); Rodash v. AIB Mortgage, 16 F.3d 1142

(11th Cr.1994); Steele v Ford Motor Credit, 783 F.2d 1016 (11th Cir.1986), all binding here under Kasket v. Chase Manhattan Mtge. Corp., 759 So.2d 726 (Fla. 4th DCA 2000) (11th Circuit cases on federal TIL issues are binding on Florida courts).

2. The error must be a “material error” which is defined at Reg Z 226.23 fn 48: “The term “material disclosures” means the required disclosures of the annual percentage rate, the finance charge, the amount financed, the total payments, the payment schedule, and the disclosures and limitations referred to in sections 226.32(c) and (d).”

3. A HOEPA loan requires additional disclosures 3 days before consummation. See: Reg Z 226.31(c)(1) (“The creditor shall furnish the disclosures required by section 226.32 at least three business days prior to consummation of a mortgage transaction covered by section 226.32.”). The failure to deliver the HOEPA forms is an additional TIL material disclosure which extends the right to rescind for violations. See: Reg Z 226.23(a)(3): “The consumer may exercise the right to rescind until midnight of the third business day following consummation, delivery of the notice required by paragraph (b) of this section, or delivery of all material disclosures, [fn]48 whichever occurs last. If the required notice or material disclosures are not delivered, the right to rescind shall expire 3 years after consummation….” See also fn 48 above.

4. Florida’s Fair Lending Act is based on the HOEPA triggers and appears to adopt TIL right to rescind without the 3 year limit. See: Fla. Stat. §494.00792(d). This theory has not been tested in any appellate court.

5. Most creditor’s closing/underwriting files will have a signed acknowledgment that the consumer received 2 copies of the TIL notice of right to cancel. Under TIL 15 U.S.C. 1635(c) this creates a rebuttable presumption of receipt: “Notwithstanding any rule of evidence, written acknowledgment of receipt of any disclosures required under this subchapter by a person to whom information, forms, and a statement is

required to be given pursuant to this section does no more than create a rebuttable presumption of delivery thereof.” Once the consumer’s affidavit or interrogatory answer or deposition stares that the consumer did not receive the 2 notices, this rebuts the presumption of receipt in the acknowledgment and presents a question of fact for trial. See: Cintron v. Bankers Trust Company, 682 So.2d 616 (Fla. 2nd DCA 1996).

6. The critical issue is what did each consumer receive not what is in the creditor’s underwriting or closing file. Make sure that the TIL Right to Rescind form is correctly filled out and the loan closed on the date it purports to have closed. If the lender directs the consumer to deliver the notice of right to cancel form to a post office box, this should extend the right to rescind.

D. Material Errors

1. The TIL Disclosure Statement “Federal Box” will contain the following “material information”. These numbers are taken from the Norwest v. Queen Martin trial memorandum: {4}

Annual Percentage Rate Finance Charge Amount Financed

11.227% $176,073.12 $70,708.16

Total of Payments

$246,781.28

PAYMENTS: Your payment schedule will be:

Number of Payments Amount of Payments When Payments Are Due

Monthly beginning

359 685.52 10/01/99

1 679.60 09/01/29

————————————————

{4} The disclosures are interrelated. If one multiplies the monthly payment amounts by the number of payments, and adds the sums, this equals the total of payments. Adding the finance charge to the amount financed equals the total of payments. The annual percentage rate is the percent of these figures, based on 360 monthly payments, using either the American or actuarial method.

—————————————-

2. At the bottom of the TIL Disclosure Statement, usually just inside the bottom part of the federal box, you will see a place for the creditor to place an “X” next to: “‘e’ means an estimate;” and a second box to place an “X” next to: “all dates and numerical disclosures except the late payment disclosures are estimates.” Estimated disclosures violate TIL.

3. If no Reg Z 226.18(c) required Itemization of Amount Financed (not a material disclosure error) one “work backwards” to determine how the creditor arrived at the TIL disclosures. First, one must deduct the $70,708.16 “amount financed” from the face amount of the note. Lets assume this note was for a $76,500.00 loan. Therefore the creditor had to use $5,791.84 as the total of “prepaid finance charges.” In order

to arrive at the disclosed $70,708.16 “amount financed.” Then one must examine the HUD-1 charges to find the charges that equal the $5,791.84 “prepaid finance charges” to determine the items from the HUD-1 that the creditor included in the $5,791.84 prepaid finance charges to determine if $5,791.84 correct reflects all the prepaid finance charges. See: §1638(a)(2)(A); Reg Z 226.18(b): “The amount financed is calculated by: (1) Determining the principal loan amount or the cash price

(subtracting any downpayment); (2) Adding any other amounts that are financed by the creditor and are not part of the finance charge (usually not applicable); and, (3) Subtracting any prepaid finance charge.”

4. The Norwest/Martin Trial memo has a great deal of detail with respect to the specific charges and violations.

F. Truth in Lending Remedies

1. §1635(b) and Reg Z 226.23(d)(1-4) rescission; and, 2) §1640 damages.

2. Semar v. Platte Valley Federal S & L Ass’n, 791 F.2d 69 (9th Cir. 1986) is the leading case used by virtually all courts to impose TIL’s §1635(b) and Reg Z 226.23(d)(1-4) rescission remedy in a non-§1639, non-vesting case.

3. Semar, interpreted Reg Z 226.23(d)(1) “Effects of rescission: When a consumer rescinds a transaction, the security interest giving rise to the right of rescission becomes void and the consumer shall not be liable for any amount, including any finance charge.” The Semar, Court accepted the consumer’s rescission formula under Reg Z 226.23(d)(1), added all the “finance charges” listed on the HUD-1, plus the 2 $1,000.00 maximum statutory damage awards ($1,000.00 for the initial error and $1,000.00 for the improper response to rescission, increased to $2,000.00 in 1995),

plus all the mortgage payments made, then deducted this sum from the face amount of the Semar, note to arrive at the net debt owed the creditor.

4. §1640(a)(2)(A)(iii) Statutory Damages $2,000.00 for initial errors and $2,000.00 for the improper response to rescission. See: 15 U.S.C. §1635(g); 15 U.S.C. §1640 (a)15 U.S.C. §1640(g); Gerasta v. Hibernia Nat. Bank, 575 F.2d 580 (5th Cir. 1978), binding in the 11th Circuit under Bonner. (TIL statutory damages available for initial TIL error and improper response to demand to rescind).

5. §1640(a)(1) Actual Damages for any errors: Hard to prove need to establish “detrimental reliance” on an erroneous disclosure.

6. §1640(a)(4) Enhanced HOEPA Damages: §1640(a)(4) enhances the damages: “in the case of a failure to comply with any requirement under section 1639 of this title, an amount equal to the sum of all finance charges and fees paid by the consumer, unless the creditor demonstrates that the failure to comply is not material.”

5. Equitable Modification under §1635(b) and Reg Z 226.23(d)(4). Williams v. Homestake Mortg. Co., 968 F.2d 1137 (11th Cir. 1992) allows for equitable modification of TIL, Burden on lender to prove facts that justify the equitable modification. If not, Florida courts must follow Yslas v. D.K Guenther Builders, Inc., 342 So.2d 859, fn 2 (Fla. 2nd DCA 1977), which holds:

“The statutory scheme to effect restoration to the status quo provides that within ten days of receipt of the notice of rescission the creditor return any property of the debtor and void the security interest in the debtor’s property. The debtor is not obligated to tender any property of the creditor in the debtor’s possession until the creditor has performed his obligations. If the creditor does not perform within ten days of the notice or does not take possession of his property within ten days of the

tender, ownership of the creditor’s property vests in the debtor without further obligation.” [emphasis added].

The 2nd District recently reaffirmed Yslas in Associates First Capital v. Booze, 912 So.2d 696 (Fla. 2nd DCA 2005). Associates, involved a partial §1635(b) and Reg Z 226.23(d)(1-4) rescission because the consumer refinanced with the same creditor, and the refinance included an additional advance of credit. In the Associates, the consumer can rescind only the additional advance. Important here, the Associates,

consumer argued, and the Court agreed that the lender failed to perform a condition precedent to equitably modify TIL by failing to respond to his rescission notice within 20 days, as required by §1635(b) and Reg Z 226.23(d)(2):

“If a lender fails to respond within twenty days to the notice of rescission, the ownership of the property vests in the borrowers and they are no longer required to pay the loan. See § 1635(b); Staley v. Americorp Credit Corp., 164 F. Supp. 2d 578, 584 (D. Md. 2001); Gill v. Mid-Penn Consumer Disc. Co., 671 F.Supp. 1021 (E.D.Pa. 1987). However, because 12 C.F.R. § 226.23(f)(2) provides only a partial right of rescission where there is a refinancing, when the Lender failed to respond to

the notice of rescission within twenty days, ownership of only the property subject to the right of rescission — the $994.01 loaned for property taxes — vested in the Borrowers without further obligation.” Associates, p. 698.

G. Truth in Lending Supplements State Remedies & Both Apply

1. Williams v. Public Finance Corp., 598 F.2d 349, rehearing denied with opinion at 609 F.2d 1179 (5th Cir. 1980), binding here under Bonner, holds that a consumer can get both TIL damages and usury damages because state usury laws and the Federal Truth in Lending Act provide separate remedies to rectify separate wrongs based on separate unrelated statutory violations. The 5th Circuit rejected the creditor’s “double penalty” argument by holding that if it accepted the argument, it would give special lenient treatment to the creditor when his loan violates 2 separate statutes, one state and one federal, designed to remedy 2 separate wrongs:

“Moreover, we eschew an analysis of these statutory cases limited by the

common law doctrines of compensation for breach of contract. These cases involve penal statutes, and we are compelled to enforce their clear and direct commands whether or not they seem to be overcompensating in a contract or tort analysis. There is nothing inherently wrong, excessive, or immoral in a borrower receiving two bounties for catching a lending beast who has wronged him twice — first, by sneaking up on him from behind, and then by biting him too hard. The private attorney general who exposes and opposes these credit wolves is not deemed unduly enriched when his valor is richly rewarded and his vendor harshly rebuked. Nor does the state’s punishment for the usurious bite interfere with Congress’s punishment for the wearing of sheep’s clothing.”

“We have come, or gone, a long way from Shakespeare’s ancient caution, “Neither a borrower, nor a lender be.” In today’s world borrowing and lending are daily facts of life. But that a fact becomes diurnal does not mean it has been cleansed of its dire potential. We still heed the Bard’s advice, but in our own modern way — by strict regulation of the strong and careful protection of the weak and unwary. While the well-intended efforts of our many sovereigns may at times sound more like discordant and competing solos than mellifluous duets, we, as judges, must restrain

our impulse to stray from the score.” Williams, 609 F.2d pg. 359-360.

In case the first opinion was unclear on this point, the Williams, rehearing opinion repeated and reaffirmed its “lending wolf” analysis:

“Noting that the effect of appellants’ argument was to ask for “special lenient treatment to lenders who violate two laws instead of just one,” we rejected the approach to the question proposed by the appellants and defined our inquiry in the following terms:

[W]e think the real question in this case is a relatively standard one of statutory interpretation. More specifically, we think the question is whether Congress intended that the TIL Act would apply to loans which violated state usury laws punishable by forfeiture. At the outset we note that no exception for such loans is made explicitly in the TIL Act. Moreover, since the Act is to be construed liberally to effect its remedial purposes, Thomas v. Myers-Dickson Furniture Co., 479 F.2d 740, 748 (5th

Cir. 1973), we are generally disinclined to read into the Act an implicit exception which benefits lenders at the expense of borrowers. However, the real test of whether this exception was intended or not must start with the question of whether it serves or disserves the purposes of the Act. In this analysis resides the real focus of our decision. The ILA and TIL Act provide separate remedies to rectify separate wrongs.

The ILA limits what a lender subject to its provisions can charge for the use of its money; the TIL Act provisions involved here are designed to penalize and deter an independent wrong arising from nondisclosure. [fn5] We did not believe, and do not believe, that it subserves the purposes of the TIL Act to read into it an implied exception for loans which violate unrelated state usury laws. As we have already said, we do not think it especially unfair or unjust to order two punishments for a

lender who violates two laws. And more to the point, we think it would be directly contrary to the purposes and policies of the TIL Act to excuse a violator from federal penalty simply because he is also liable for a state penalty, especially where that state penalty may often be less harsh than the federal penalty…….”

“…… Appellants petition for rehearing have taken offense at our characterization of lenders who violate the ILA as “credit wolves” and as wearers of “sheep’s clothing” when they also violate the disclosure provisions of the TIL Act. They suggest that such labels have obscured our analysis of the legal issues here. Such most certainly is not the case. Our analysis was and is based on our perception of the proper

construction of the federal and state policies, even though their meshing is not nearly as perfect as we and appellants could wish. Nonetheless, as we read the ILA and the TIL Act, appellants have violated both and are subject to the penalties of both. Although appellants’ predations may be technical and they may feel we have cried “wolf” too readily, the fact remains that as we read the statutes appellants are guilty of the violations charged.” Williams, 598 F.2d pg. 1181-1184.

When Homeowner’s good faith attempts to amicably work with the Bank in order to resolve the issue fails;

Home owners should wake up TODAY! before it’s too late by mustering enough courage for “Pro Se” Litigation (Self Representation – Do it Yourself) against the Lender – for Mortgage Fraud and other State and Federal law violations using foreclosure defense package found at http://www.fightforeclosure.net “Pro Se” litigation will allow Homeowners to preserved their home equity, saves Attorneys fees by doing it “Pro Se” and pursuing a litigation for Mortgage Fraud, Quiet Title and Slander of Title; among other causes of action. This option allow the homeowner to stay in their home for 3-5 years for FREE without making a red cent in mortgage payment, until the “Pretender Lender” loses a fortune in litigation costs to high priced Attorneys which will force the “Pretender Lender” to early settlement in order to modify the loan; reducing principal and interest in order to arrive at a decent figure of the monthly amount the struggling homeowner could afford to pay.

If you find yourself in an unfortunate situation of losing or about to lose your home to wrongful fraudulent foreclosure, and need a complete package that will show you step-by-step litigation solutions helping you challenge these fraudsters and ultimately saving your home from foreclosure either through loan modification or “Pro Se” litigation visit: http://www.fightforeclosure.net