Tags

Center for Housing Policy, Florida, Foreclosure, MER, Mortgage Electronic Registration System, RealtyTrac, Securitization, United States

Quiet Title Actions: How to Force the Banks To Prove Up

The Foreclosure Crisis

I. THE FORECLOSURE CRISIS

• ISSUE ONE: Who Owns Your Note?

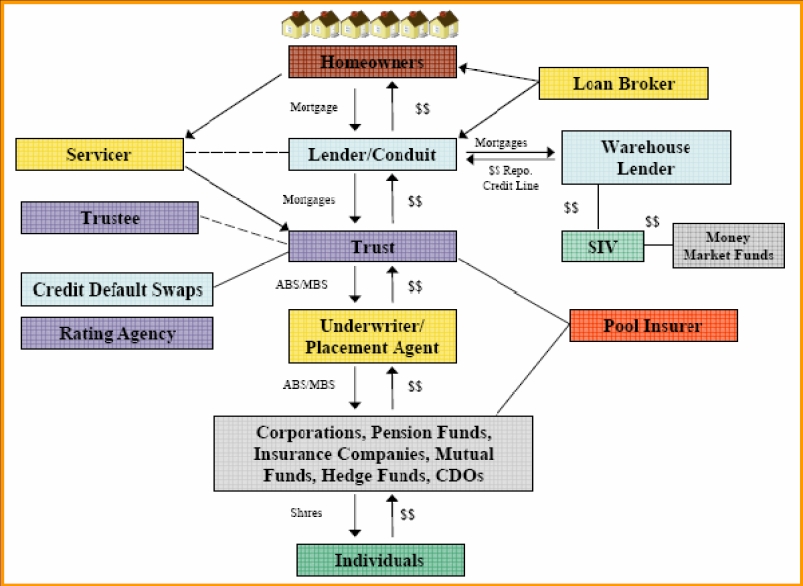

1. The Securitization Process:

– A. Originator Sells To Nominee (First Sale)

– B. The Nominee Sells To Depositor (Second Sale)

– C. The Depositor Sells to the REMIC Trust

• The REMIC Trust created to hold “pool” of mortgages and sell “shares” in

the REMIC Trust to investors.

• A Trustee is designated to operate the trust (typically a bank).

• The REMIC Trust operates through “Bylaws” and “Pooling and Servicing

Agreements”.

• The Pooling and Servicing Agreement outlines how the income from the

mortgages will be managed and the Servicing Agent who will collect income

and foreclose in the event of default.

The Foreclosure Crisis

• One in every 365 housing units in the United States was branded with a foreclosure notice recorded in December 2011, according to RealtyTrac.com. That means 850,000 Americans got a big lump of coal in their stocking from Uncle Scrooge.

• Over 2,076,764 American homes are now in foreclosure.

• One in every 165 housing units in California (more that twice the national average) received a foreclosure notice in December, for a total of 80,488 properties. In Nevada, the figure was one in every 93 houses.

• USA Today reports that almost 1 in 5 children in Nevada lived or live in owneroccupied homes that were lost to foreclosure or are at risk of being lost. The percentages are 15% in Florida, 14% for Arizona, and 12% for California. That’s about one in eight children in California. Five years into the foreclosure crisis, an estimated 2.3 million children have lived in homes lost to foreclosure.

• RealtyTrac reports that foreclosure and REO (real estate-owned) homes accounted for 24 percent of all residential sales during the fourth quarter of 2011.

• Here in relatively affluent Palm Beach County, homeowners are No. 1 in the state for the average number of loans in foreclosure that are delinquent. It has the fourth highest number of foreclosures, 45,829 with an average delinquency of 623 days.

Florida’s Foreclosure Statistics

• Florida is leading the country in foreclosure rates.

• Florida metro areas dominate the top 25 list for cities with the worst foreclosure rates — including the eight highest in the nation, according to a report released Tuesday.#

• In all, 17 of the top 25 cities with the highest foreclosure rates as of March are Florida cities, according to the Center for Housing Policy, the research arm of the Washington, D.C.-based National Housing Conference. #

• With a 10.9 percent foreclosure rate, Jacksonville is ranked 18th overall, but 14 other Florida cities had higher rates. Miami topped the list with the nation’s highest rate of 18.2 percent. #

• Miami’s conventional mortgage foreclosure rate in March was 14.2 percent, while its subprime rate was 39.1 percent. Jacksonville’s conventional foreclosure rate was 7.8 percent while its subprime rate was 29 percent.

• But given the fact that Florida cities made up 15 of the 25 cities with the highest “serious” mortgage delinquency rates — either behind by 90 days behind or more or now in foreclosure, there could be more foreclosures in the state’s future. And just like on the foreclosure list, Miami was also first, with a delinquency rate of 23.6 percent; and Jacksonville was 18th, with a rate of 15.6 percent.

Who Owns Your House?

• ISSUE ONE: WHO OWNS YOUR HOUSE?

– Promissory Note (the “Note”): Loan Agreement

– Mortgage/Deed of Trust: Power of Sale Document

– Grant Deed: You own until you breach the Promissory Note and

your Lender (or Others) use the Power of Sale Document to

Foreclose

– Before Securitization: Your Lender held your Note was always

the Foreclosing Entity.

– After Securitization: No One Knows Who Owns Your Note

Who Owns Your Note?

ISSUE TWO: Who Owns Your Note?

1. The Securitization Process:

– A. Originator Sells To Nominee (First Sale)

– B. The Nominee Sells To Depositor (Second Sale)

– C. The Depositor Sells to the REMIC Trust

• The REMIC Trust created to hold “pool” of mortgages and sell “shares” in

the REMIC Trust to investors.

• A Trustee is designated to operate the trust (typically a bank).

• The REMIC Trust operates through “Bylaws” and “Pooling and Servicing

Agreements”.

• The Pooling and Servicing Agreement outlines how the income from the

mortgages will be managed and the Servicing Agent who will collect income

and foreclose in the event of default.

• Why Is There a Question?

1. The Securitization Process: No One Knows Who Owns Your

Note

– The Original Lenders Failed to Properly Assign Your Note to

Subsequent Purchasers

– Incompetent Personnel

– No Training: No One Trained to Sell Notes Properly

– Never Occurred Before: Prior to Securitization Didn’t

Transfer or Sell Notes

– Thousands of Assignments Left Blank

– Remic Trusts Never Receive Assignments or Possession of

Notes: Current litigation

2. Mortgage Electronic Registration System, Inc

1. Created by over 44 Financial Institutions in 1998 to Avoid the

Registration of Securitized Mortgages : Saves Millions of

Dollars in Recordation fees;

2. Presently Being Sued in (5) States for Unlawfully failing to pay

Recording Fees on Securitized Mortgage Transactions

• WHAT IS MERS FUNCTION?

– TO CAMOUFLAGE THE SALE OF YOUR LOAN TO MULTIPLE

ENTITIES IN THE SECURITIZATION PROCESS;

– AVOID RECORDING FEES ON EVERY SALE OF YOUR LOAN

TO SUBSEQUENT PURCHASERS.

– ACT AS “BENEFICIARY” OF YOUR DEED OF TRUST OR

“NOMINEE” OF YOUR MORTGAGE

What is MERS?

• “MERS is a mortgage banking ‘utility’ that registers

mortgage loans in a book entry system so that … real

estate loans can be bought, sold and securitized (Similar

to Wall Street’s book entry utility for stocks and bonds is

the Depository Trust and Clearinghouse.”

• MERS is enormous. It originates thousands of loans

daily and is the mortgagee of record for at least 40

million mortgages and other security documents.

• MERS acts as agent for the owner of the note. Its

authority to act should be shown by an agency

agreement. Of course, if the owner is unknown, MERS

cannot show that it is an authorized agent of the owner.

Result: BANKS CAN’T PROVE THEY OWN YOUR LOAN

• The Wall Street Journal Picks Up the Scent

• An article by Nick Timiraos appeared in The Wall Street Journal on June 1, 2011 – “Banks Hit Hurdle to Foreclosures.”

• “Banks trying to foreclose on homeowners are hitting another roadblock,” Timiraos writes, “as some delinquent borrowers are successfully arguing that their mortgage companies can’t prove they own the loans and therefore don’t have the right to foreclose.”

• If you (or I) try to boot a homeowner into the street without any proof that we’re entitled to the property, the cops will lock us up. Stealing is stealing, whether it is somebody’s wallet or their 3-bedroom 2-bath in the suburbs with two dogs and a kid. When a bank tries to steal the bungalow without proof that they have a right to foreclose, it’s a “hurdle” or “another roadblock.”

• Semantics aside, this is good news for all people holding grant deeds. This year, the Journal reports, cases in California, North Carolina, Alabama, Florida, Maine, New York, New Jersey, Texas, Massachusetts and other states have raised questions about whether banks properly demonstrated ownership.

• In some cases, borrowers are showing courts that banks failed to properly assign ownership of mortgages after they were pooled into mortgage-backed securities. In other cases, borrowers say that lenders backdated or fabricated documents to fix those errors.

• “Flawed mortgage-banking processes have potentially infected millions of foreclosures, and the damages against these operations could be significant and take years to materialize,” said Sheila Bair, chairman of

the Federal Deposit Insurance Corp., in testimony to a Senate committee last month.

• In March, an Alabama court said J.P. Morgan Chase & Co. couldn’t foreclose on Phyllis Horace, a delinquent homeowner in Phenix City, Ala., because her loan hadn’t been properly assigned to its owners

– a trust that represents investors – when it was securitized by Bear Stearns Cos. The mortgage assignment showed that the loan hadn’t been transferred to the trust from the subprime lender that originated it.

The Problem With MERS

• Federal bankruptcy courts and state courts have found that MERS and its member banks often confused and misrepresented who owned mortgage notes. In thousands of cases, they apparently lost or mistakenly destroyed loan documents.

• The problems, at MERS and elsewhere, became so severe last fall that many banks temporarily suspended foreclosures.

• Not even the mortgage giant Fannie Mae, an investor in MERS, depends on it these days.

• “We would never rely on it to find ownership,” says Janis Smith, a Fannie Mae spokeswoman, noting it has its own records.

• Apparently with good reason. Alan M. White, a law professor at the Valparaiso University School of Law in Indiana, last year matched MERS’s ownership records against those in the public domain.

• The results were not encouraging. “Fewer than 30 percent of the mortgages had an accurate record in

MERS,” Mr. White says. “I kind of assumed that MERS at least kept an accurate list of current ownership.

They don’t. MERS is going to make solving the foreclosure problem vastly more expensive.”

• The Arkansas Supreme Court ruled last year that MERS could no longer file foreclosure proceedings there, because it does not actually make or service any loans. Last month in Utah, a local judge made the no-lessstriking decision to let a homeowner rip up his mortgage and walk away debt-free. MERS had claimed ownership of the mortgage, but the judge did not recognize its legal standing.

• And, on Long Island, a federal bankruptcy judge ruled in February that MERS could no longer act as an “agent” for the owners of mortgage notes. He acknowledged that his decision could erode the foundation of the mortgage business.

• But this, Judge Robert E Grossman said, was not his fault.

• “This court does not accept the argument that because MERS may be involved with 50 percent of all residential mortgages in the country,” he wrote, “that is reason enough for this court to turn a blind eye to

the fact that this process does not comply with the law.”

Legal Issues

1. SEPARATION OF THE NOTE AND THE DEED

• In the case of MERS, the Note and the Deed of Trust are held by separate entities. This can pose a unique problem dependent upon the court. The prevailing case law illustrates the issue:

• “The Deed of Trust is a mere incident of the debt it secures and an assignment of the debt carries with it the security instrument. Therefore, a Deed Of Trust is inseparable from the debt and always abides with the debt. It has no market or ascertainable value apart from the obligation it secures.

• A Deed of Trust has no assignable quality independent of the debt, it may not be assigned or transferred apart from the debt, and an attempt to assign the Deed Of Trust without a transfer of the debt is without effect. “

• This very “simple” statement poses major issues. To easily understand, if the Deed of Trust and the Note are not together with the same entity, then there can be no enforcement of the Note. The Deed of Trust enforces the Note. It provides the capability for the lender to foreclose on a property. If the Deed is separate from the Note, then enforcement, i.e. foreclosure cannot occur.

The following ruling summarizes this nicely.

• In Saxon vs Hillery, CA, Dec 2008, Contra Costa County Superior Court, an action by Saxon to foreclose on a property by lawsuit was dismissed due to lack of legal standing. This was because the Note and the Deed of Trust were “owned” by separate entities. The Court ruled that when the Note and Deed of Trust were separated, the enforceability of the Note was negated until rejoined.

2. MERS IS A NOMINEE AND NOT THE HOLDER OF THE NOTE

• The question now becomes as to whether a Note Endorsed in Blank and transferred to different entities does allow for foreclosure. If MERS is the foreclosing authority but has no entitlement to payment of the money, how could they foreclose? This is especially true if the true beneficiary

is not known. Why do I raise the question of who the true beneficiary is?

• THE MERS WEBSITE STATES…..

• “On MERS loans, MERS will show as the beneficiary of record. Foreclosures should be commenced in the name of MERS. To effectuate this process, MERS has allowed each servicer to choose a select number of its own employees to act as officers for MERS.

Through this process, appropriate documents may be executed at the servicer’s site on behalf of MERS by the same servicing employee that signs foreclosure documents for non-MERS loans. Until the time of sale, the foreclosure is handled in same manner as non-MERS foreclosures. At the time of sale, if the property reverts, the Trustee’s Deed Upon Sale will follow

a different procedure. Since MERS acts as nominee for the true beneficiary, it is important that the Trustee’s Deed Upon Sale be made in the name of the true beneficiary and not MERS. Your title company or MERS officer can easily determine the true beneficiary. Title companies have indicated that they will insure subsequent title when these procedures are followed.”

3. MERS IS THE NOMINEE AND NOT THE BENEFICIARY

• To further reinforce that MERS is not the true beneficiary of the loan, one need only look at the following Nevada Bankruptcy case, Hawkins, Case No. BK-S-07-13593-LBR (Bankr.Nev. 3/31/2009) (Bankr.Nev., 2009) – “A “beneficiary” is defined as “one designated to benefit from an appointment, disposition, or assignment . . . or to receive something as a result of

a legal arrangement or instrument.” BLACK’S LAW DICTIONARY 165 (8th ed. 2004). But it is obvious from the MERS’ “Terms and Conditions” that MERS is not a beneficiary as it has no rights whatsoever to any payments, to any servicing rights, or to any of the properties secured by the loans. To reverse an old adage, if it doesn’t walk like a duck, talk like a duck, and quack like a duck, then it’s not a duck.”

• When the initial Deed of Trust is made out in the name of MERS as Nominee for the Beneficiary and the Note is made to AB Lender, there should be no issues with MERS acting as an Agent for AB Lender. Hawkins even recognizes this as fact.

• The issue does arise when the Note transfers possession. Though the Deed of Trust states “beneficiary and/or successors”, the question can arise as to who the successor is, and whether Agency is any longer in effect. MERS makes the argument that the successor Trustee is a MERS

member and therefore Agency is still effective, and there does appear to be merit to the argument on the face of it.The original Note Holder, AB Lender, no longer holds the note, nor is entitled to payment. Therefore, that Agency relationship is terminated. However, the Note is endorsed in blank, and no Assignment has been made to any other entity, so who is the true

beneficiary? And without the Assignment of the Note, is the Agency relationship intact?

4. MERS FORECLOSURE PROCEDURES

• There, you have it. Direct from the MERS website. They admit that they

name people to sign documents in the name of MERS. Often, these are

Title Company employees or others that have no knowledge of the actual

loan and whether it is in default or not.

• Even worse, MERS admits that they are not the true beneficiary of the loan.

In fact, it is likely that MERS has no knowledge of the true beneficiary of the

loan for whom they are representing in an “Agency” relationship. They

admit to this when they say “Your title company or MERS officer can

easily determine the true beneficiary.

• Why are the Courts Accepting MERS as a Nominee or Agent of the

“Lenders”? The “beneficiary” term is erroneous. Even MERS states it

is not a “beneficiary”.

• If so, MERS cannot assign deeds of trust or mortgages to third parties

legally.

• ISSUE THREE: Does MERS have the Right to Participate in Your

Foreclosure?

– NO. According to the Majority of Federal Court Opinions and Every State Supreme Court decision which has addressed this Issue: Oregon and Washington Supreme Ct Decisions Pending

– Every Attorney General who has examined the legality of MERS has determined it is illegal business enterprise: New York; Delaware; Oregon, Washington, Idaho; with more to come.

_ Declared Unlawful Business Organization : ( In re: Agard, No. 10-77338, 2011 Bankr. LEXIS 488, at 58-59 (Bankr. E.D.N.Y. Feb 10, 2011)

_ In California, the federal court determined that MERS has to have a written contract with the new noteholder in order to have the authority to appoint or assign the beneficial interest in the note sufficient to foreclose (In re: Vargas: US Dist Ct, Central Dist of Calif; Case No LA 08-107036-SB).

– Judge Michael Simon of the Oregon Federal Court has found that MERS cannot assign its beneficiary status in a deed of trust to a third party for foreclosure purposes due to the fact that MERS does not under Oregon law have the legal authority to do so (James, et al v Reconstruct Trust, et al: US Dist Ct. Case No: 3:11-cv-00324-ST).

Solutions

QUIET TITLE ACTIONS: Definition

• quiet title action n. a lawsuit to establish a party’s title to real property

against anyone and everyone, and thus “quiet” any challenges or claims to

the title. Such a suit usually arises when there is some question about clear

title, there exists some recorded problem (such as an old lease or failure to

clear title after payment of a mortgage), an error in description which casts

doubt on the amount of property owned, or an easement used for years

without a recorded description. An action for quiet title requires description

of the property to be “quieted,” naming as defendants anyone who might

have an interest (including descendants—known or unknown—of prior

owners), and the factual and legal basis for the claim of title. Notice

must be given to all potentially interested parties, including known and

unknown, by publication. If the court is convinced title is in the plaintiff (the

plaintiff owns the title), a quiet title judgment will be granted which can be

recorded and thus provide legal “good title.“

• QUIET TITLE ACTIONS:

– Purpose: Require All Adverse Claims to Title to Prove to the Court the

Worthiness of Their Claim:

– Mortgages/Deeds Of Trust:

• Who is the Owner of Your Note? Prove It

• Who is the Beneficiary of Your Deed of Trust/Mortgage? The Owner of the

Note

• Who has the Legal Right to Foreclose?

– ONLY THE OWNER OF THE NOTE IS A TRUE BENEFICIARY

– ONLY THE BENEFICIARY OF THE MORTGAGE OR DEED OF

TRUST OR ITS LEGAL REPRESENTATIVE CAN FORECLOSE

– MERS IS NOT A BENEFICIARY-According to its own Website

– MERS IS NOT A LEGAL REPRESENTATIVE OF ANY REMIC TRUST

» No Contract

» At Best MERS has a Contractual Relationship with Original Lender

• FLORIDA QUIET TITLE STATUTES-Civil Practice and Procedure

• 65.061 Quieting title; additional remedy.—

• (1) JURISDICTION.–Chancery courts have jurisdiction of actions by any person or corporation claiming legal or equitable title to any land…. and shall determine the title of plaintiff and may enter judgment quieting the title and awarding possession to the party entitled thereto….

• (2) GROUNDS.–When a person or corporation not the rightful owner of land has any conveyance or other evidence of title thereto, or asserts any claim, or pretends to have any right or title thereto, any person or corporation is the true and equitable owner of land the record title to which is not in the person or corporation because of the defective execution of any deed or mortgage because of the omission of a seal thereon, the lack of witnesses, or any defect or omission in the wording of the acknowledgment of a party or parties thereto, when the person or corporation claims title thereto by the defective instrument and the defective instrument was apparently made and delivered by the grantor to convey or mortgage the real estate and was recorded in the county where the land lies which may cast a cloud on the title of the real owner….

• (4) JUDGMENT.–If it appears that plaintiff has legal title to the land or is the equitable owner thereof based on one or more of the grounds mentioned in subsection (2), or if a default is entered against defendant (in which case no evidence need be taken), the court shall enter judgment removing the alleged cloud from the title to the land and forever quieting the title in plaintiff and those claiming under him or her since the commencement of the action and adjudging plaintiff to have a good fee simple title to said land or the interest thereby cleared of cloud.

DECLARATORY RELIEF

• WHO OWNS THE NOTE? WHO IS ENTITLED TO FORECLOSE?

• FEDERAL RULES OF CIVIL PROCEDURE: RULE 57. DECLARATORY JUDGMENT

• 28 U.S.C. §2201. Rules 38 and 39 govern a demand for a jury trial. The existence of another adequate remedy does not preclude a declaratory judgment that is otherwise appropriate. The court may order a speedy hearing of a declaratory-judgment action.

• The fact that a declaratory judgment may be granted “whether or not further relief is or could be prayed” indicates that declaratory relief is alternative or cumulative and not exclusive or extraordinary. A declaratory judgment is appropriate when it will “terminate the controversy” giving rise to the proceeding. Inasmuch as it often involves only an issue of law

on undisputed or relatively undisputed facts, it operates frequently as a summary proceeding, justifying docketing the case for early hearing as on a motion, as provided for in California (Code Civ.Proc. (Deering, 1937) §1062a), Michigan (3 Comp.Laws (1929) §13904), and Kentucky

(Codes (Carroll, 1932) Civ.Pract. §639a–3).

• The “controversy” must necessarily be “of a justiciable nature, thus excluding an advisory decree upon a hypothetical state of facts.” Ashwander v. Tennessee Valley Authority, 297 U.S. 288, 325, 56 S.Ct. 466, 473, 80 L.Ed. 688, 699 (1936). The existence or nonexistence of any right, duty, power, liability, privilege, disability, or immunity or of any fact upon which such legal relations depend, or of a status, may be declared.

• WRONGFUL FORECLOSURE:

• What is a Wrongful Foreclosure Action?

• A wrongful foreclosure action typically occurs when the lender starts a

judicial foreclosure action when it simply has no legal cause. Wrongful

foreclosure actions are also brought when the service providers accept

partial payments after initiation of the wrongful foreclosure process, and

then continue on w i t h the f o r e c l o s u r e process. These

predatory lending strategies, as well as other forms of misleading

homeowners, are illegal.

• The borrower is the one that files a wrongful disclosure action with the court against the service provider, the holder of the note and if it is a non-judicial foreclosure, against the trustee complaining that there was an illegal, fraudulent or willfully oppressive sale of property under a power of sale contained in a mortgage or deed or court judicial proceeding. The borrower can also allege emotional distress and ask for punitive damages in a wrongful foreclosure action.

• FRAUD CLAIMS

• Mortgage Payments: Have you been paying mortgage payments to the

wrong financial institution?

• JP Morgan Chase: Bought “Assets” of WAMU from FDIC in 2008

– All Mortgage Loans from 2003-2008 were already sold to REMIC Trusts

– What Did Chase Bank Buy? Servicing Contracts?

– Can Chase Bank Foreclose on Notes It Does Not Own?

• One West Bank: Bought “Assets” of IndyMac from FDIC in 2008

– All Mortgage Loans from 2003-2008 were already sold to REMIC Trusts

– What did One West Bank Buy? Servicing Contracts?

– Can One West Foreclose on Notes It Does Not Own?

• Bank of America: Bought “Servicing Contracts” from Countrywide in 2008

– All Mortgage Loans from 2003-2008 were already sold to REMIC Trusts

– What Did Bank of America Buy? Servicing Contracts

– Can Bank of America Foreclose on Notes It Does Not Own?

• QUIET TITLE LITIGATION:

– Potential Outcomes:

• Actual Quiet Title: Removal of All Liens, Encumbrances,

Mortgages:

• Principal Reduction: Mediation or Arbitration Resulting in

Substantial Reduction in Your Mortgage Balance

• Damage Claims against Financial Institutions: Punitive Damages?

• TROS and Injunctions: Stopping the Foreclosure Process

• Did Default Insurance Pay Off My Mortgage

• Declaratory Relief:

– Who Do I Pay My Mortgage To?

– Who Can Foreclose on My House?

Credit Rehabilitation

• Credit Rehabilitation

• The Fair Credit Reporting Act (FCRA) gives you the right to contact credit bureaus directly and dispute items on your credit reports. You can dispute any and all items that are inaccurate, untimely, misleading, biased, incomplete or unverifiable (questionable items). If the bureaus cannot verify that the information on their reports is indeed correct, then those items must be deleted.

• PeabodyLaw has created the “Mortgage Audit Plan”:

– Obtain a Securitization Audit from Audit Pros, Inc.

– Peabody Law will utilize the results of your Securitization Audit to file a

court action seeking a court order removing all negative credit reporting

items from your credit history based upon the findings of the audit.

– Upon receipt of Court Judgment rendering the nullification of unlawful

and erroneous credit references, Peabody Law will send a Demand

Letter with the Judgment attachment to each Credit Reporting Agency

demanding retraction and removal of all negative credit references

relating to mortgage payments, foreclosures, short sales, etc.

For a Complete Pro Se “Do It Yourself” Foreclosure Defense Kit With Well Drafted Pleadings and Step By Step Guide For Saving Your Home Visit: http://www.fightforeclosure.net