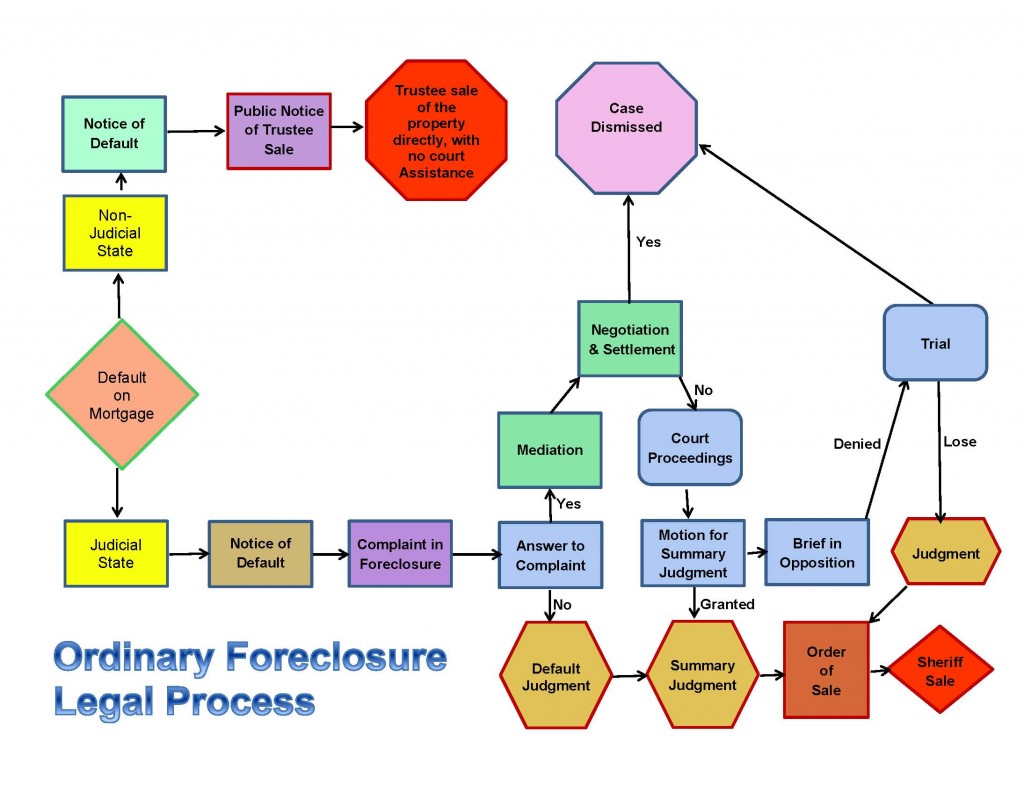

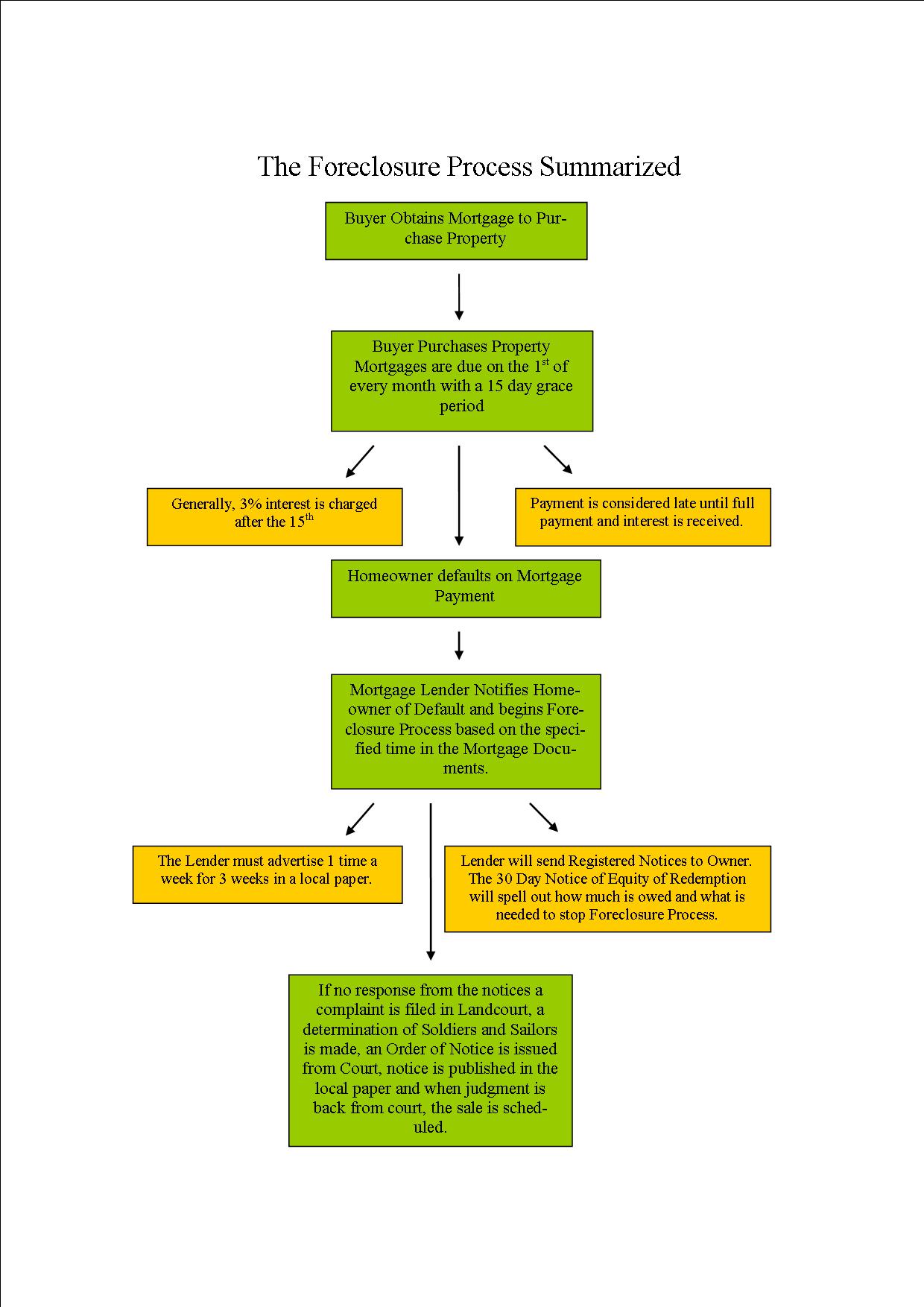

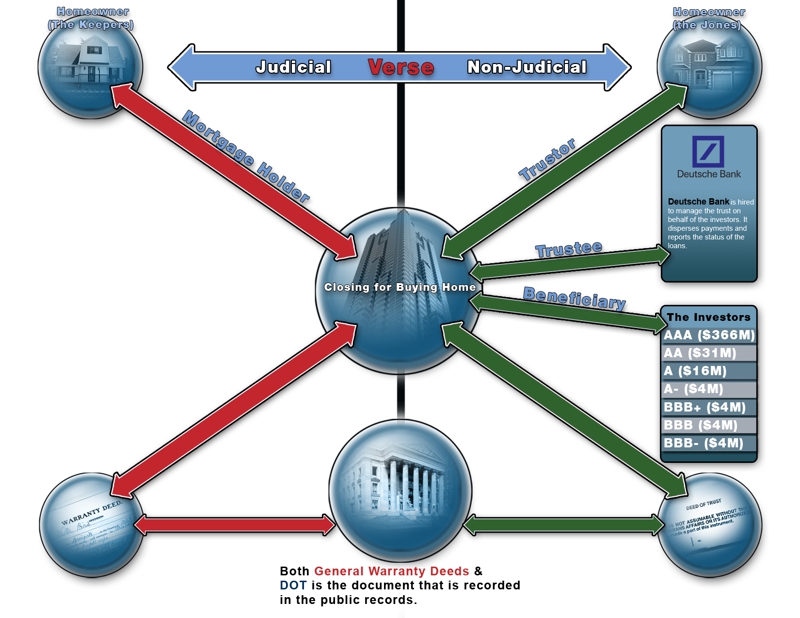

Foreclosures may be judicial (ordered by a court following a judgment in a lawsuit) or non-judicial (“on the courthouse steps”). Most foreclosures in Texas are nonjudicial. These are governed by chapter 51 of the Property Code and are held on the first Tuesday of each month between 10 a.m. and 4 p.m. at a designated spot at the county courthouse. The effect of foreclosure is to cut off and eliminate junior liens, including mechanic’s liens, but not tax obligations.

The remedy of foreclosure is available in the event of a borrower’s monetary default (nonpayment) or technical default (e.g., failure to pay taxes or keep the property insured). In order to determine if there has been a default, the loan documents–the note, the deed of trust, the loan agreement, and so forth–should be carefully examined. Notice and opportunity to cure requirements contained in these documents must be strictly followed if a foreclosure is to be valid.

Notices of foreclosure sales must be filed with the county clerk and posted (usually on a bulletin board in the lobby of the courthouse) at least 21 calendar days prior to the intended foreclosure date. Notices are entitled “Notice of Trustee’s Sale” or “Notice of Substitute Trustee’s Sale.” They provide information about the debt, the legal description of the property, and designate a three-hour period during which the sale will be held. In larger metropolitan areas there are foreclosure listing services which publish a monthly list of properties posted for foreclosure.

Required Notices to the Borrower

Notices to the defaulting borrower must be given in accordance with Property Code sections 51.002 et seq. and the deed of trust. The content of foreclosure notices is technical and must be correct to insure a valid foreclosure that cannot later be attacked by a wrongful foreclosure suit. Clients often protest when their lawyer advises re-noticing the debtor–”But I’ve already sent them an email telling them they are in default.” Not good enough.

Usually, two certified mail notices to the borrower are required, the first being a “Notice of Default and Intent to Accelerate” which gives formal notice of the default and affords an opportunity for the borrower to cure it (at least 20 days for a homestead, although if the deed of trust is on the FNMA form, 30 days must be given). Note that S.B. 766 and S.B. 472, which did not make it out of committee in the 81st Legislature, would have extended the 20-day period. This legislation may be revived in the future. Many lawyers consider it best to routinely give a 30-day notice.

After the cure period has passed, a “Notice of Acceleration and Posting for Foreclosure” must be sent at least 21 days prior to the foreclosure date. This second letter must also specify the location of the sale and a three-hour period during which the sale will take place. A notice of foreclosure sale should be enclosed. This notice is also filed with the county clerk and physically posted at the courthouse. If there is going to be a change in trustees it is also necessary to file a written appointment of substitute trustee. Notices are addressed to the last known address of the borrower contained in the lender’s records (this is the legal requirement), but it is wise for the lender to double-check this to avoid later claims by the borrower that notice was defective. It is prudent to send notices by both first-class and certified mail. Why? The reason has to do with Texas’s mailbox rule, i.e., that a notice properly deposited in the U.S. mail is presumed to be delivered. “Common sense . . . dictates that regular mail is presumed delivered and certified mail enjoys no [such] presumption unless the receipt is returned bearing an appropriate notation.” McCray v. Hoag, 372 S.W.3d 237, 243 (Tex. App.–Dallas 2012, no pet. h.). A careful lender will send notices to all likely addresses where the borrower may be found.

Other lienholders (whether junior or senior) are not entitled to notice. Depending on the first lienholder’s strategy, however, it may be useful to discuss the issue with them.

If the borrower is able to cure, a reinstatement agreement should be executed unless the terms of the debt have been changed (e.g., payments have been lowered) in which case a hybrid reinstatement/modification agreement or even a new note may be appropriate.

Notice to the IRS

The best practice is to do a title search prior to foreclosure to determine if there is an IRS tax lien or other federal lien. If so, notice must be given to the IRS and/or the U.S. Attorney at least 25 days prior to the sale, not including the sale date. 26 U.S.C. § 7425(c)(1). If this is not done, any IRS tax lien on the property will not be extinguished by the sale. Note that the IRS also has 120 days following the sale to redeem the property, although this seldom happens. The successful bidder on an IRS-liened property is therefore not entitled to breathe a sigh of relief until the 121st day.

Fair Debt Collection Practices Act

The Fair Debt Collection Practices Act (15 U.S.C. §§ 1601 et seq.) requires that a borrower be given 30 days to request and obtain verification of the debt. The lender may give notice of default, accelerate the debt, and even post for foreclosure in less time, but the foreclosure sale itself should not be conducted until the 30-day debt verification period has expired.

There is also an equivalent state statute (the Texas Debt Collection Practices Act) contained in Finance Code chapter 392. Failure to provide verification of the debt when the borrower has requested it in writing has serious penalties under both laws.

Due Diligence by the Investor Prior to Foreclosure

Buying property at foreclosure sales is a popular form of investment but it contains traps for the unwary. The investor’s goal is to acquire instant equity in the property by paying a relatively modest sum at the foreclosure sale. However, apparent equity can evaporate if the property is loaded down with liens. It is advisable, therefore, to check the title of the property that will be sold. Is the lien being foreclosed a second or third lien? If so, then the first lien (usually a purchase-money lien held by a mortgage company) will continue in force. First liens are king. They are not extinguished by foreclosure on an inferior lien. What about IRS liens? Improvement liens? Liens imposed by homeowners associations? Any or all of these could consume whatever equity might otherwise have existed in the property. If an investor is unsure as to which liens will be wiped out in a foreclosure sale, then copies of each lien document should be pulled and taken to the investor’s real estate attorney for review. As far as researching title is concerned, every professional investor should ultimately acquire the skills to go to the real property records in the county clerk’s office and do this unaided. One should obtain copies of the warranty deed and any deeds of trust or other lien instruments. Alternatively, a down-date report from a title company may be requested.

If more information is needed about the property itself, one can contact the trustee named in the Notice of Trustee’s Sale. Trustees vary in their level of cooperation but are often willing to provide additional information if they have it. They may have a copy of an inspection report on the property which they may be willing to share. One might even be able to arrange to view the property if it is unoccupied.

The investor should also check the military status of the borrower, since Property Code section 51.015 prohibits non-judicial foreclosure of a dwelling owned by active duty military personnel or within 9 months after active duty ends. Knowingly violating this law is a Class A misdemeanor.

Property Condition

It goes without saying that the investor should physically inspect the property if at all possible, although one should not trespass on occupied property to do this. It is legal, however, to stand in the street (public property) and take photos.

When one buys at a foreclosure sale, it is “as is.” Property condition is therefore important. When buying residential properties in particular, an investor should be especially curious about condition of the foundation (learn to recognize signs of settlement), whether the property is flood-prone, and whether or not there may be environmental contamination (generally not a problem if the house is in a restricted subdivision). It is usually best to avoid any property that suffers from one or more of these deficiencies. Other items that involve significant expense are the roof and the HVAC system.

The past or continuing presence of hazardous substances can impose huge potential liability (particularly on commercial properties) since both Texas and federal law provide that any owner of property (including the investor) is jointly and severally liable with any prior owner for cleanup costs. The Texas Commission on Environmental Quality (“TCEQ”) maintains a web site at www.tceq.state.tx.us where the environmental history of a property can be researched.

Valuation

It is, of course, important not to bid more than the equity in the property (fair market value less the total dollar amount of the liens, if any, that will survive the foreclosure sale). So how does one discover fair market value? Again, it is a question of getting the right information. One of the best ways to do this is to obtain a comparative market analysis or broker price opinion (BPO) from a realtor.

Last-Minute Bankruptcies

Foreclosures can be rendered void by last-minute bankruptcy filings. Some professional investors will check with the bankruptcy clerk’s office the morning of the sale to make sure that the borrower has not filed under any chapter of the U.S. Bankruptcy Code before they bid on the property. Note that the bankruptcy clerk’s office opens at 9 a.m. and bidding commences at 10 a.m. Checking bankruptcy filings is a wise precaution if the borrower has previously filed or threatened bankruptcy. It can be cumbersome and inconvenient to get money back from a trustee on a void sale.

Conduct of the Sale

Foreclosure sales in the larger counties can seem chaotic, with many sales going on at once. There are two general types: sales by trustees (usually attorneys) for individual and institutional lenders and sales by the county sheriff for unpaid taxes. Sales are held at the location designated by the commissioners of the county where the property is located–often the courthouse steps or close by.

The sale is conducted by the named trustee unless a substitute trustee has been duly appointed and notice of the appointment has been filed of record. As a practical matter, the foreclosing trustee is usually the attorney for the lender.

There is no standard or required script for a trustee to follow in auctioning property, although trustees usually recite the details of the note and lien, the fact that the note went into default, proper notice was given, the note was subsequently accelerated, and the property is now for sale to the highest cash bidder. The trustee has a duty to conduct the sale fairly and impartially and to not discourage bidding in any way (this can result in “chilled bidding,” which is a defect). A trustee may set reasonable conditions for conducting the foreclosure sale and may set the terms of payment (e.g., by cash or cashier’s check). However, these conditions and terms must be stated prior to the opening of bidding for the first sale of the day held by that trustee.

Bidding at the Sale

The investor should remain in motion, talking to the trustees, until finding the right trustee with the right property. Caution: do not let the excitement of the sale cause you to exceed your preestablished maximum bid.

The lender often bids the amount of the debt plus accrued fees and costs, so this bid can be anticipated. If the sale generates proceeds in excess of the debt, the trustee must distribute the excess funds to other lienholders in order of seniority and the remaining balance, if any, to the borrower.

If the investor is the successful bidder, he or she should be prepared to make payment “without delay” or within a mutually agreed-upon time. In order to be prepared, seasoned bidders carry with them some cash plus an assortment of cashier’s checks in different amounts made payable to “Trustee.” If the high bidder is for any reason unable to complete the purchase, then the trustee will reopen the bidding and auction the property again. The successful bidder will, within a reasonable time, receive a trustee’s deed or substitute trustee’s deed which conveys the interest that was held by the borrower in the property–no more, no less.

Property Code section 51.009 states that a buyer at a foreclosure sale “acquires the foreclosed property ‘as is’ without any expressed or implied warranties, except as to warranties of title, and at the purchaser’s own risk; and is not a consumer.” The “consumer” part of that statement is meant to prevent any DTPA claims.

Elapsed Time

Compared to other states, Texas has a streamlined non-judicial foreclosure process that is nearly as quick as an eviction. The minimum amount of time from the first notice to the day of foreclosure is 41 days, unless the deed of trust is a FNMA form, in which case the time is 51 days, although it is never wise to cut these deadlines that close. Why risk a void sale or give the borrower a possible wrongful foreclosure claim?

The advantage of a foreclosure over an eviction is that there are no effective defenses to the foreclosure process except for the borrower to block it with a temporary restraining order or file bankruptcy. For either option, the buyer needs money and probably an attorney.

Deficiency Suits

In the event that proceeds of the foreclosure sale exceed the amount due on the note (including attorney’s fees and expenses), then surplus funds must be distributed to the borrower. More often, however, the price at which the property is sold is less than the unpaid balance on the loan, resulting in a deficiency. A suit may be brought by the lender to recover this deficiency any time within two years of the date of foreclosure. Tex. Prop. Code § 51.003. Federally insured lenders have four years. As part of a defense to a deficiency suit, the borrower may challenge the foreclosure sales price if it is below fair market value, and receive appropriate credit if it is not. Any money received by a lender from private mortgage insurance is credited to the account of the borrower. One case states that the purpose of this “is to prevent mortgagees from recovering more than their due.”

For borrowers, deficiencies can be as significant a loss as the foreclosure itself since the IRS deems the deficiency amount to be taxable ordinary income.

Servicemembers Civil Relief Act

The Servicemembers Civil Relief Act (“SCRA”), 50 U.S.C. app. § 501, which was passed in 2003 completely rewrites the existing 1940 law by expanding protections for those serving in the armed forces. Except by court order, a landlord may not evict a servicemember or dependents from the homestead during military service. The SCRA provides criminal sanctions for persons who knowingly violate its provisions.

Right of Redemption

There is no general right of redemption by a borrower after a Texas foreclosure. The right of redemption is limited to:

(1) Sale for unpaid taxes. After foreclosure for unpaid taxes, the former owner of homestead or agricultural property has a two-year right of redemption (Tax Code section 34.21a). The investor is entitled to a redemption premium of 25% in the first year and 50% in the second year of the redemption period, plus recovery of certain costs that include property insurance and repairs or improvements required by code, ordinance, or a lease in effect on the date of sale. For other types of property (i.e., nonhomestead), the redemption period is 180 days and the redemption premium is limited to 25%.(2) HOA foreclosure of an assessment lien. Prop. Code section 209.011 provides that a homeowner may redeem the property until no “later than the 180th day after the date the association mails written notice of the sale to the owner and the lienholder under section 209.101.” A lienholder also has a right of redemption in these circumstances “before 90 days after the date the association mails written notice . . . and only if the lot owner has not previously redeemed.” These provisions are part of the Texas Residential Property Owners Protection Act designed to reign in the once arbitrary power of HOAs (Chapter 209 of the Code). Note that an HOA is not permitted to foreclose on a homeowner if its lien is solely for fines assessed by the association or attorney fees.

An investor should be prepared to hold the property and avoid either making substantial improvements to it or reselling it until after any applicable rights of redemption have expired.

Postforeclosure Eviction

Foreclosure gives the new owner title; the next step is to obtain possession, and the procedure for doing this is outlined in the previous chapter. It is generally necessary to give the usual 3-day notice to vacate and file a forcible detainer petition in justice court. After judgment, the new owner must wait until the constable posts a 48 hour notice on the door and then forcibly removes a former borrower if that person is otherwise unwilling to leave.

An investor should build eviction costs into the budget from the beginning. It is advisable to hire an attorney for the first couple of evictions, after which an investor will likely be prepared to handle them solo. Never, however, attempt to conduct an eviction appeal to county court without an attorney.

As discussed in the chapter on evictions, there are both state and federal protections for tenants. Both Property Code section 24.005(b) and the federal Protecting Tenants at Foreclosure Act of 2009 require at least 90 days’ notice to vacate so long as a tenant continues to pay rent.

Stopping a Foreclosure Sale

It is a myth that lawyers can wave a wand and, with a phone call or nasty letter, stop foreclosure. Attorneys have no such power. It is a fact that foreclosure can be stopped, but the only sure way to do so is to file a lawsuit and successfully persuade a judge to issue a temporary restraining order prior to the foreclosure sale. After the sale occurs, the remedy that remains–a suit for wrongful foreclosure–is slightly different. Relief may be limited to a money judgment if the property was sold at foreclosure to a third party for cash (a bona fide purchaser or “BFP”). If a BFP is in the mix, the possibility that the property itself can be recovered by the borrower is near zero.

Clients will often report that they have been engaged in reinstatement negotiations with the lender, usually consisting of numerous phone calls and messages, and ask if that is sufficient to avoid a scheduled foreclosure. The answer is a resounding no. Unless there is payment of the arrearage and a signed reinstatement agreement, the foreclosure will almost certainly go forward, even if the client was talking settlement with the lender just the day before. Note that reinstatement agreements must be in writing and signed by both parties. Phone calls mean nothing in this business.

Clients will sometimes state that they don’t want to sue the lender; they just want to get a restraining order to stop the foreclosure. The lawyer must reply “Sorry, it doesn’t work that way, you can’t split the two.” A restraining order is an ancillary form of relief, meaning that it arises from an underlying suit. In other words, there must be an actual lawsuit in place to provide a basis for requesting a TRO. Fortunately, the suit and application for the TRO can be filed simultaneously and a hearing obtained usually within a day.

There is an additional issue: a borrower must have grounds for legal action or possibly face penalties for filing a frivolous suit. Some clients have difficulty understanding this. “Why,” they ask, “can’t you just go and get a TRO for me?” The answer is that the lawyer must give the judge at least some credible basis for granting equitable relief.

So why don’t more people sue to stop a foreclosure? Money. A person in financial distress will have difficulty coming up with cash. Here is the blunt truth: if a borrower or investor cannot readily write a substantial retainer check to an attorney for purposes of suing a lender, then that person has no business in the expensive world of litigation.

Wrongful Foreclosure Suits

After the sale, a suit for wrongful foreclosure can be filed if there are grounds for alleging that the loan documents (e.g., the note and deed of trust) were defective in some way; if the notices leading up to the foreclosure were done incorrectly; or if there was some alleged impropriety in the sale itself. Note that there is no requirement that the sales price be fair. A sale cannot be set aside because the consideration paid is allegedly inadequate because it is less than market value. Sauceda v. GMAC Mortg. Corp., 268 S.W.3d 135, 139 (Tex. App.–Corpus Christi 2008, no pet.). To prevail in a wrongful foreclosure suit based on inadequate sale price, three elements must be proven: (1) grossly inadequate consideration; (2) defective foreclosure notices or sale; and (3) a causal connection between the defect and the inadequate consideration. If the notices and sale were correctly done, then the sale will be valid even though the sales price was lower than market value.

As a general rule, it is far better for a borrower to obtain a restraining order to stop a foreclosure than it is to bring suit after the fact. Texas law favors the finality of foreclosures, making wrongful foreclosure suits an uphill battle. If the property was sold to a third party who has no knowledge of any claims or alleged defects there is little chance that the borrower will get the property back. The third party is a protected BFP, and any remedy for the borrower will therefore likely be limited to monetary damages. Bottom line? If in doubt about whether or not a foreclosure is going to occur, file suit and attempt to get a temporary restraining order to stop it. “Wait and see” is the worst possible strategy in this case, since it is always more difficult to correct the situation after the foreclosure sale has occurred. The judge will likely ask without much sympathy, “Why, since you knew about these various alleged defects, did you not take action to stop the foreclosure?”

If a wrongful foreclosure suit is being considered, it should be filed quickly so that notice of the suit (a notice of lis pendens) can be filed in the real property records. If the lender was the successful bidder, this notice may effectively prevent the lender from transferring the property to a BFP.

Note that the action available under Property Code section 51.004 (discussed above) is different from a wrongful foreclosure remedy per se. Relief is granted if the court finds that the fair market value is greater than the sale price, but only in the context of a deficiency claimed by the lender.

The cruel fact for borrowers is that wrongful foreclosure suits face challenges from the beginning. Is that fair? You decide. It is, however, undoubtedly the bias of Texas judges, whether one approves or not.

A plaintiff can realistically expect the following in a wrongful foreclosure lawsuit: (1) The lender will not rush to settle, since lenders pay high fees to large litigation firms to fight tooth and nail to avoid doing the right thing; (2) written discovery (interrogatories, requests for production, and requests for admission) from the plaintiff will be nearly entirely objected to by lender’s counsel, so extensively as to make the responses essentially useless (a deposition will therefore be required); (3) lender’s counsel will remove the case from state court to federal court where judges are more conservative and lenders can use Federal Rule 12(b)(6) to dismiss the case. This rule permits dismissal if the borrower’s complaint fails “to state a claim upon which relief can be granted,” which happens more often than one might think. A change of courts can also create complications for the attorney representing the borrower, who may be accustomed to practicing in state rather than federal court. The attorney may be an experienced state court lawyer, but may not even be licensed in federal court. This is common as federal practice becomes more of a specialty among lawyers.

Prolonged Negotiations for a Modification

Homeowners often report that they were engaged in prolonged negotiations to modify their existing loan prior to the foreclosure sale. Of course, these communications were conducted by phone and there is no signed written agreement binding the lender to stop the sale, so there is likely no basis for a wrongful foreclosure suit. Do lenders pursue this strategy intentionally, so as to make it appear that they are willing to be reasonable, when in fact it is in their interest to foreclose instead? Opinions vary.

If you find yourself in an unfortunate situation of losing or about to your home to wrongful fraudulent foreclosure, visit: http://www.fightforeclosure.net

31.968599

-99.901813