Tags

Fannie Mae, Foreclosure, Ibanez, Massachusetts, Massachusetts Supreme Judicial Court, U.S. Bancorp, Uniform Commercial Code, US Bank

Introduction

As a result of the collapse of the housing market in this country in or around 2008, the number of residential foreclosures has increased exponentially, putting unprecedented strains on the system.

Although most foreclosures are uncontested, since there is rarely any doubt that the borrower has defaulted in repayment of the debt, in the past several years a cottage industry has developed challenging the creditor’s “standing” to foreclose, sometimes colloquially known as the “show me the Note” defense.

The Commonwealth of Massachusetts has seen its share of this phenomenon, maybe more than its share.

This post will briefly review the string of Massachusetts judicial decisions over the past several years addressing various aspects of the foreclosure standing question, and will use those cases to “issue-spot” and frame questions that practitioners in every state should consider and perhaps need to answer before moving ahead with foreclosures or to defend past foreclosures in litigation, whether in defense of borrowers’ lawsuits or in eviction proceedings. Other notables decisions will also be surveyed to flesh out the issues and arguments further, without attempting to be exhaustive of the subject or to present the proverbial 50-State survey.

The Massachusetts Story

We begin with the Massachusetts foreclosure story. In early 2009, a judge on Massachusetts specialized Land Court called into question a title standard of the State’s Real Estate Bar Association that had been relied upon by the Massachusetts foreclosure Bar. REBA Title Standard No. 58 said that a foreclosure was not defective so long as an assignment of the mortgage was obtained at any time before or after the foreclosure. In other words, the title could be cleared by obtaining an assignment even after the conduct of the foreclosure auction sale. Land Court Judge Keith Long in U.S. Bank, N.A. v. Ibanez, 2009 WL 795201 (Mass. Land Ct. Mar. 26, 2009), held that the title standard did not correctly state Massachusetts law, and that under the Massachusetts foreclosure statute, M.G.L. c. 244, a creditor had to be the mortgagee to foreclose. In 2011, the Massachusetts Supreme Judicial Court in U.S. Bank, N.A. v. Ibanez, 458 Mass. 637 (2011), affirmed, holding that a foreclosing entity, if not the original mortgagee, must hold an assignment of the mortgage at the time it first published the notice of sale.

If the assignment of the mortgage was obtained after publication of the notice, a subsequently-completed foreclosure is unlawful and void.

Because Massachusetts is a non-judicial foreclosure jurisdiction, the foreclosing creditor does not have available ares judicata defense to a post-foreclosure challenge to title or possession.

Thus, the Massachusetts Court has held that a borrower or other defendant in an eviction action can defend by contesting the validity of a purchaser’s title if it stems from an invalid foreclosure, even if the mortgagor had done nothing to contest the foreclosure itself. Bank of New York v. Bailey, 460 Mass. 327 (2011).

The plaintiffs in Ibanez were securitization trustees and while the evidence in the record was incomplete, contributing to the result, the trustees were presumed to have held the notes in the respective loan pools, including the defendants’ notes, for the benefit of the investors. The Ibanez Court required the mortgagee to hold an assignment, and implicitly found that it would not be sufficient to confer standing to foreclose to hold the note without also holding the mortgage or obtaining an assignment, but nothing in the decision presaged a requirement that the mortgagee possess the note.

The argument that the mortgagee must also hold the note to foreclose was pressed to the Massachusetts high court almost immediately in the wake of Ibanez. This issue arises in Massachusetts because, contrary to the majority and longstanding American rule that the mortgage is mere security for the note and follows the note as a matter of law, Carpenter v. Longan, 83 U.S. 271 (1872), Massachusetts is a title-theory state that allows for the note and mortgage to be held separately. Under Article 3 of the Uniform Commercial Code (“UCC”), a note can be transferred by delivery of possession of an endorsed note, but Massachusetts, as a title theory state, requires a signed instrument to convey a mortgage, “which represents legal title to someone’s home.” Ibanez, 458 Mass. at 649. Comparable to the equity of redemption residing in the mortgagor, to reclaim legal title by repaying the debt and redeeming the mortgage, the owner of the note under Massachusetts law holds beneficial ownership of the mortgage and has the right to compel an assignment of the mortgage by the mortgagee, who holds the mortgage in trust for the holder of the note, in what has been described as a resulting trust implied by law. Id. at 652.

In Eaton v. Fannie Mae, 462 Mass. 569 (2012), the Court laid down a new rule that foreclosing mortgagees must either (a) hold the note, or (b) be acting on behalf of the note holder. In other words, the Court held that “one who, although not the note holder himself, acts as the authorized agent of the note holder,” may exercise the power of sale. Id. at 586. Notably, unlike in Ibanez where the Court rejected entreaties for prospective application of its decision, the Eaton court chose to apply its holding prospectively only to foreclosures noticed after the date of the decision out of “concern for litigants and others who have relied on existing precedents,” this being a “new rule.” Id. at 588.

Massachusetts courts, like courts elsewhere, have also considered the standing of Mortgage Electronic Registration Systems, Inc. (“MERS”) to foreclose mortgages and to assign mortgages for foreclosure. MERS, discussed in greater detail below, holds title to mortgages as nominee for MERS Members. The Eaton court discussed MERS in several footnotes, see 462 Mass. 569 nn. 5, 7, 27 & 29, and implicitly accepted MERS’ pre-foreclosure assignment of the mortgage to the mortgage servicer.

In a federal court appeal earlier this year, the First Circuit Court of Appeals in Boston held expressly that MERS has the authority to assign mortgages it holds as nominee. Culhane v. Aurora Loan Services, — F.3d —-, 2013 WL 563374 (1st Cir., Feb. 15, 2013). Indeed, in the District Court decision the Court of Appeals affirmed, District Judge William Young remarked that “the MERS system fits perfectly into the Massachusetts model for the separation of legal and beneficial ownership of mortgages.” Culhane v. Aurora Loan Services, 826 F. Supp. 2d 352, 371 (D. Mass. 2011).

The recent Massachusetts mortgage foreclosure decisions were surprising, bordering on shocking, both to lenders and the Massachusetts real estate and foreclosure bars. In Ibanez, the Court disapproved a title standard of the well-respected statewide real estate bar group that conveyancers and others looked to for guidance, and in Eaton the Massachusetts Court for the first time announced a requirement that a foreclosing mortgagee be able to demonstrate its relationship to the mortgage note notwithstanding that there is no requirement under Massachusetts law to record or file notes or note transfers. 462 Mass. at 586;see also Wells Fargo Bank, N.A. v. McKenna , 2011 WL 6153419, at *2 n.1 (Mass. Land Ct. Dec. 8, 2011) (“There never has been recording of notes at the registries of deeds at any time. Notes are never recorded—not (as they may be in some other states) when the initial mortgage is recorded, nor at any time after that, including at the time, following the auction sale, when the foreclosure deed and

affidavit are put on at the registry.”). Whether the greater numbers of foreclosures and the perceived financial excesses and highly publicized alleged “sloppiness” of the mortgage industry have caused some courts to be more “pro-consumer,” or it is only that some of the legal doctrines underlying foreclosure standing had not been closely examined in a century or more, the rulings were unexpected. In part, they may represent the challenge of adapting historical, and in some cases ancient, property law to modern commerce, or vice versa. But they point out the critical need to understand state law, and to not take for granted that traditional custom and practice will be upheld, or that courts will not struggle applying that law or those established customs and practice to non-traditional modern mortgage ownership structures.

Mortgage notes, representing the debt for which the mortgages are collateral, will generally qualify as negotiable instruments whose ownership and transfer is governed by the principles of Article 3 of the UCC, adopted largely intact in most American jurisdictions. But despite the efforts of the UCC Commissioners to harmonize the law of security interests, including in some respects in real property, mortgage law and mortgage foreclosure in particular remains predominantly a creature of local state law. Thus, for mortgage foreclosure purposes, where the foreclosing creditor stands, in the legal vernacular, may depend on where the house sits. The discussion below frames some of the key standing inquiries suggested by the Massachusetts experience, and surveys some recent case law from across the country addressing the same or similar questions, and compares and contrasts the judicial precedents.

Although subsidiary questions such as whether the state is a title theory or lien theory jurisdiction, and whether the mortgage is deemed to follow the note as a matter of law, may affect how the questions are answered in any particular state, the core questions remain the same and can generally be framed in the following terms:

1. What relationship must the foreclosing entity have to the mortgage (or to the corresponding deed of trust in jurisdictions that know the security instrument by that terminology), and at what time must it hold or have it?

2. What relationship, if any, must the foreclosing entity have to the promissory note secured by the mortgage (or by the deed of trust), and at what time?

3. Does MERS when it holds the mortgage as nominee (or when it is named as beneficiary under a deed of trust) have standing to foreclose, or the ability to assign the mortgage (or deed of trust) to the lender, trustee or servicer for foreclosure?

4. Who has standing to foreclose in the securitization context, given the legal relationships under the standard Pooling and Servicing Agreement between and among the securitization trustee, the mortgage servicer and, where applicable, MERS as nominee under the mortgage (or deed of trust)?

There is a large body of case law nationwide on all of these questions, with additional decisions being handed down on virtually a daily basis; what follows below is only a representative sampling intended to illustrate the more significant issues and arguments, to inform the analysis of applicable local state law.

1. Relationship Between Foreclosing Entity and Mortgage.

In U.S. Bank, N.A. v. Ibanez, 458 Mass. 637 (2011), as discussed above, the Massachusetts Supreme Judicial Court held that a foreclosing entity must hold an assignment of the mortgage at the time of the publication of the notice of sale. Other states differ on whether they require a foreclosing party to hold the mortgage either at the time of the foreclosure sale itself or when notice is issued.

In considering any question of a party’s status in the foreclosure process, it is first important to note whether jurisdictions are judicial or non-judicial jurisdictions:

– Judicial foreclosure states require the foreclosing party to initiate a court proceeding in order to foreclose. The foreclosure complaint seeks permission from the court to foreclose on the secured property.

– Non-judicial foreclosure jurisdictions do not require court involvement. Instead, the foreclosing entity must follow certain practices as set by state statute, such as mailing notices of acceleration and default, and publishing notice in the local papers. That entity often is the deed of trust trustee, under state law. If the borrower wishes to contest the sale, he or she may seek to enjoin it before the sale occurs.

Twenty-two states are considered judicial foreclosure jurisdictions, whereas 28 are deemed non-judicial.

In New York, where foreclosures are conducted judicially, one court recently stated that “a plaintiff has standing where it is both the holder or assignee of the subject mortgage and the holder or assignee of the underlying note at the time the action is commenced.” Wells Fargo Bank, N.A. v Wine, 90 A.D.3d 1216, 1217 (N.Y. App. Div. 3d Dep’t 2011).

To a similar effect, one Florida court has said a party must “present evidence that it owns and holds the note and mortgage in question in order to proceed with a foreclosure action.” Gee v. U.S. Bank N.A., 72 So. 3d 211, 213 (Fla. Dist. Ct. App. 5th Dist. 2011). But a different Florida appellate court has held that an assignment of the mortgage may not be necessary at the time a complaint is filed. Standing to bring a judicial foreclosure requires “either an assignment or an equitable transfer of the mortgage prior to the filing of the complaint.” McLean v. JP Morgan Chase Bank N.A., 79 So. 3d 170, 172 (Fla. Dist. Ct. App. 4th Dist. 2012). Because ownership of a mortgage follows an assignment of the debt under that case, the mortgage does not need to be assigned to the plaintiff before the Complaint is filed if it proves ownership of the note at that time.

New Jersey, also a judicial state, has said that if a foreclosing creditor bases standing to foreclose on assignment of the mortgage, the assignment must precede filing of the foreclosure complaint; however, if the foreclosing creditor held the note at the time of filing the complaint, assignment of the mortgage is unnecessary to establish standing to foreclose. Deutsche Bank Nat’l Trust Co. v. Mitchell, 422 N.J. Super. 214, 222-25 (App. Div. 2011). There, although Deutsche Bank had not proved its standing because the mortgage assignment it relied on was executed a day after it filed its complaint, the Court remanded to allow Deutsche Bank to demonstrate standing by proving that it possessed the note prior to filing the complaint. Contrast state filing rules with the law of a non-judicial state like Michigan, which allows a foreclosing party to be “either the owner of the indebtedness or of an interest in the indebtedness secured by the mortgage or the servicing agent of the mortgage.” MCL 600.3204(1)(d)). Thus, under the statute, a loan servicer is expressly authorized to foreclose regardless of whether it holds the note or mortgage. However, by the date of the foreclosure sale, the mortgage must be assigned to the foreclosing party if it is not the original mortgagee. MCL 600.3204(3).

Where an assignment of the mortgage may be required in order to foreclose, there are differences regarding whether the assignment of mortgage is required to be recorded.

– Massachusetts: In U.S. Bank, N.A. v. Ibanez, 458 Mass. 637 (2011), although the Court required the foreclosing entity to hold the mortgage, it notably did not require the assignment of mortgage be recorded – or even be in recordable form.

– California, likewise, does not require that assignments of a deed of trust be recorded prior to foreclosure, despite a statutory pre-foreclosure recording requirement for mortgage assignments (mortgages are uncommon in California). Calvo v. HSBC Bank USA, N.A., 199 Cal. App. 4th 118, 122-2 (Cal. App. 2d Dist. 2011).

– New York, recording is also not required. See, e.g., Bank of NY v. Silverberg, 86 A.D.3d 274, 280 (N.Y. App. Div. 2nd Dep’t 2011) (rejecting contention that absence of recorded assignment allowed inference that plaintiff did not own the note and mortgage; “an assignment of a note and mortgage need not be in writing and can be effectuated by physical delivery”).

But some non-judicial states require that assignments of deeds of trusts or mortgages be recorded before a foreclosure can occur:

– Oregon: Ore. Rev. Stat. § 86.735(1)

– Idaho: Idaho Stat. § 45-1505(1)

– Minnesota: Minn. Stat. § 580.02(3)

– Montana: Mont. Code Ann. § 71-1-313(1)

– Wyoming: Wyo. Stat. § 34-4-103(a)(iii)

Regardless of any requirement, assignees typically record mortgage assignments to put the world on notice of their interest. See MetLife Home Loans v. Hansen, 48 Kan. App. 2d 213 (Kan. Ct. App. 2012) (“The assignment of the Mortgage was merely recorded notice of a formal transfer of the title to the instrument as required by recording statutes, which are primarily designed to protect the mortgagee against other creditors of the mortgagor for lien-priority purposes, not to establish the rights of the mortgagee vis-à-vis the mortgagor.”

Need for Correct Corporate Names

When an assignment of mortgage is required, it must also be assigned to the correct corporate entity. Confusion over corporate names can impede foreclosures.

For example, the servicer of a loan filed a judicial foreclosure action alleging that it was the assignee of the original lender. Bayview Loan Servicing, L.L.C. v. Nelson, 382 Ill. App. 3d 1184 (Ill. App. Ct. 5th Dist. 2008). Reversing the trial court’s judgment in favor of the servicer (Bayview Loan Servicing, L.L.C.), the Court of Appeals held that the servicer was not allowed to foreclose because the mortgage was not assigned to it. Rather, the mortgage had been assigned to an affiliated entity, Bayview Financial Trading Group, L.P. Id. at 1187. Without any evidence that the foreclosing entity held the note or mortgage, the fact that it was servicer was insufficient to allow it to foreclose. Id. at 1188.

But the situation was different in a judicial foreclosure filed in the same state by Standard Bank, which was the successor to the originator of the loan as a result of several mergers and name changes. Std. Bank & Trust Co. v. Madonia, 964 N.E.2d 118 (Ill. App. Ct. 1st Dist. 2011). The mortgagors argued that the plaintiff bank was required to show a mortgage assignment or endorsement of the note to it. Rejecting that argument, the Court held that the plaintiff bank retained all of the interests of the originator, including those under the note and mortgage, as a result of the mergers. Id. at 123.

A court may require proof of a merger. The note and mortgage in this case were assigned to Wells Fargo Home Mortgage, Inc. Wells Fargo Bank, N.A. v. deBree, 2012 ME 34 (Me. 2012). Upon the borrowers’ default, Wells Fargo Bank, N.A. filed a complaint as “Successor by Merger to Wells Fargo Home Mortgage, Inc.” The trial court granted summary judgment for Wells Fargo Bank. On appeal, the Maine Supreme Judicial Court held that Wells Fargo Bank had not proved its ownership of the mortgage note and mortgage because there was no evidence that it, as opposed to Wells Fargo Home Mortgage, Inc., owned the instruments. Id. at ¶ 9. The Court rejected the Bank’s arguments that the borrowers had waived their argument, and it declined to take judicial notice that Wells Fargo Home Mortgage had merged into Wells Fargo Bank. Id.at ¶¶ 9-10. The showing of ownership was necessary for the Bank to prevail on summary judgment, so the foreclosure judgment was vacated. Id. at ¶ 11.

2. Relationship Between Foreclosing Entity and Note

In Eaton v. Fannie Mae, 462 Mass. 569 (2012), discussed above, the Massachusetts Supreme Judicial Court announced a new rule, applicable to foreclosures noticed after June 22, 2012 (the date of the decision), requiring that foreclosing mortgagees must either (a) hold the note; or (b) be acting on behalf of the noteholder, at the time of foreclosure. In other words, the Court held that “one who, although not the note holder himself, acts as the authorized agent of the note holder” may exercise the power of sale.

Various courts in other states are split as to whether a foreclosing entity must hold the note.

California, for example, allows by statute non-judicial foreclosure by the “trustee, mortgagee, or beneficiary, or any of their authorized agents.” Debrunner v. Deutsche Bank National Trust Co., 204 Cal. App. 4th 433, 440 (Cal. App. 6th Dist. 2012) (quoting Cal. Civ. Code § 2924(a)(1)). The party foreclosing need not have possession of or a beneficial interest in the note because no such prerequisite appears in comprehensive statutory framework. Id. at 440-42.

In Idaho, a non-judicial foreclosure state, the state supreme court expressly rejected the idea that a party must have ownership of the note and mortgage. Trotter v. Bank of N.Y. Mellon, 152 Idaho 842, 861-62 (2012). Rather, “the plain language of the [deed of trust foreclosure] statute makes it clear that the trustee may foreclose on a deed of trust if it complies with the requirements contained within the Act.” Id. at 862.

Despite these states’ rejections of any requirement to hold the note, some courts in other jurisdictions do seem to require the foreclosing party to also be the noteholder, for example, or perhaps at least an agent or authorized person:

– New York: According to this intermediate appellate division, judicial foreclosure plaintiff must both hold the note and the mortgage at the time the action is commenced. Wells Fargo Bank, N.A. v Wine, 90 A.D.3d 1216, 1217 (N.Y. App. Div. 3d Dep’t 2011).

– Florida: In Florida, the holder of a note, or its representative, may foreclose. Gee v. U.S. Bank N.A., 72 So. 3d 211, 213 (Fla. Dist. Ct. App. 5th Dist. 2011). If the plaintiff is not the payee of the note, it must be endorsed to the plaintiff or in blank. Id.

– Maryland: The transferee of an unendorsed promissory note has the burden of establishing its rights under the note by proving the note’s prior transfer history, especially where the mortgagor requests an injunction to stop foreclosure. Anderson v. Burson, 424 Md. 232, 245 (2011). Thus, the Court held that although the agent of the substitute trustee under the mortgage had physical possession of the note, it was not a holder of the note because there was no valid endorsement; it could nevertheless still enforce the note based on concessions from the mortgagors. Id. at 251-52.

– Oklahoma: “To commence a foreclosure action in Oklahoma, a plaintiff must demonstrate it has a right to enforce the note and, absent a showing of ownership, the plaintiff lacks standing.” Wells Fargo Bank, N.A. v. Heath, 2012 OK 54, ¶ 9 (Okla. 2012).

– Washington: Under Washington’s non-judicial foreclosure statute, the trustee is required to “have proof that the beneficiary is the owner of any promissory note or other obligation secured by the deed of trust.” RCW61.24.030(7)(a). Note, however, that borrowers cannot bring a judicial action based on a beneficiary or trustee’s failure to prove to the borrower that the beneficiary owns the note. Frazer v. Deutsche Bank Nat. Trust Co., 2012 WL 1821386, at *2 (W.D. Wash. May 18, 2012) (“[T]he Washington Deed of Trust Act requires that a foreclosing lender demonstrate its ownership of the underlying note to the trustee, not the borrower.”).

Some jurisdictions more clearly take an either/or approach to foreclosing. In Michigan, for example, the foreclosing entity must be “either the owner of the indebtedness or of an interest in the indebtedness secured by the mortgage or the servicing agent of the mortgage.” Residential Funding Co., LLC v. Saurman, 490 Mich. 909 (2011) (quoting MCL 600.3204(1)(d)). The question in Saurman was whether foreclosures by MERS, as a mortgagee that did not hold the note, were proper. The Michigan Supreme Court upheld the foreclosures because the mortgagee’s interest in the note—even though not an ownership interest—was a sufficient interest in the indebtedness to allow it to foreclose.

There are other state courts that follow the either/or approach as well, for example:

– Ohio: In CitiMortgage, Inc. v. Patterson, 2012 Ohio 5894 (Ohio Ct. App., Cuyahoga County Dec. 13, 2012), the Ohio Court of Appeals held that a party has standing if “at the time it files its complaint of foreclosure, it either (1) has had a mortgage assigned or (2) is the holder of the note.” Id. at ¶ 21. Thus, the plaintiff in Patterson had standing because it possessed the note when it filed its complaint, even though the mortgagewas not assigned until later. Id. at ¶ 22.

– Alabama: In Sturdivant v. BAC Home Loans Servicing, LP, — So.3d —-, 2011 Ala. Civ. App. LEXIS 361 (Ala. Civ. App. Dec. 16, 2011), the Alabama Court of Civil Appeals ruled that a party lacked standing to foreclose because it was not yet the assignee of a mortgage when it initiated foreclosure. In Perry v. Fannie Mae, 100 So. 3d 1090 (Ala. Civ. App. 2012), the Court explained that the mortgage need not be assigned to a foreclosing party at the time it initiates foreclosure if it is a holder of the note. Because the evidence showed that the foreclosing party held the note at the time it initiated foreclosure proceedings, the foreclosure was proper. Id. at 1094-96.

– New Jersey: As noted in the preceding section, New Jersey recognizes standing to file a complaint to foreclose based on either assignment of the mortgage or possession of the note. Deutsche Bank Nat’l Trust Co. v. Mitchell, 422 N.J. Super. 214, 222 (App. Div. 2011).

MERS is a system for electronically tracking interests in mortgages that are traded on the secondary market. MERS members (approximately 6,000) agree that MERS serves as mortgagee or beneficiary, and when loan ownership or servicing rights are sold from one MERS member to another, MERS remains the titleholder to the security.

3. Standing of MERS

What is MERS?

MERS is a system for electronically tracking interests in mortgages that are traded on the secondary market. MERS members (approximately 6,000) agree that MERS serves as mortgagee or beneficiary, and when loan ownership or servicing rights are sold from one MERS member to another, MERS remains the titleholder to the security instrument as nominee on behalf of whomever owns the loan. MERS is modeled on the “book entry system” used to track ownership in stock exchanges.

The use of nominees predates MERS: “The use of a nominee in real estate transactions, and as mortgagee in a recorded mortgage, has long been sanctioned as a legitimate practice.” In re Cushman Bakery, 526 F. 2d 23, 30 (1st Cir. 1975) (collecting cases). However, the concept of a nominee serving as agent for one member of a group of possible principals—where the principal may change in a way not reflected in the public record—has fostered arange of reactions, from commendation to criticism to confusion, but ultimately MERS (and its members) have repeatedly prevailed in foreclosure challenge litigation.

Authority of MERS to Foreclose

Most courts to consider the issue have ruled that MERS may serve as mortgagee or beneficiary and foreclose, for example:

– Texas: Athey v. MERS, 314 S.W. 3d 161, 166 (Tex. App. 2010) (MERS could foreclose, though it never held the note).

– Utah: Burnett v. MERS, 2009 WL 3582294 (D. Utah Oct. 27, 2009) (“MERS had authority under the Deed of Trust to initiate foreclosure proceedings”).

– Nevada: Croce v. Trinity Mortg. Assurance Corp. 2009 WL 3172119, at 3 (D. Nev. Sept. 28, 2009) (collecting cases from Georgia, California, Florida, and Colorado rejecting argument “that MERS does not have standing as a beneficiary under the Note and Deed of Trust, and therefore, is not authorized to participate in the foreclosure proceedings.”); see also Edelstein v. Bank of N.Y. Mellon,286 P.3d 249, 254 (Nev. 2012) (“The deed of trust also expressly designated MERS as the beneficiary… it is an express part of the contract that we are not at liberty to disregard, and it is not repugnant to the remainder of the contract.”).

– Michigan: Residential Funding Corp. v. Saurman, 805 N.W. 2d 183 (Mich. 2011) held that MERS had a sufficient interest to foreclose because it owned “legal title to a security lien whose existence is wholly contingent on the satisfaction of the indebtedness.”

In addition, at least two states—Minnesota (Minn. Stat. § 507.413) and Texas (Tex. Prop. Code § 51.0001)—have enacted statutes recognizing that MERS can foreclose.

Some state courts, nevertheless, have raised various questions about MERS’s role as it relates to foreclosures.

– Oregon: In Niday v. GMAC Mortg., 284 P. 3d 1157 (Or. App. 2012), the Oregon Court of Appeals ruled that MERS did not meet Oregon’s statutory definition of “beneficiary,” disagreeing with the majority of trial court rulings that had ruled MERS could serve as beneficiary.

Niday is on appeal to the Supreme Court of Oregon; oral argument was heard January 8, 2013.

– Maine: The Maine Supreme Court has ruled that MERS cannot meet its definition of “mortgagee,” and thus had no standing to foreclose judicially. MERS v. Saunders, 2 A. 3d 289 (Me. 2010) (“MERS is not in fact a ‘mortgagee’ within the meaning of our foreclosure statute”).

– Washington: Bain v. Metro. Mortg. Group, Inc., 285 P.3d 34, 46 (Wash. 2012) ruled that MERS did not meet the statutory definition of deed of trust beneficiary, though Bain did not explain whether this impaired foreclosure proceedings.

Nearly two years ago, MERS changed its rules of membership to provide that the noteholder must arrange for an assignment to be executed from MERS to the foreclosing entity prior to commencement of any foreclosure proceeding, judicial or non-judicial. So, this issue may be a legacy question after all.

Authority of MERS to Assign Mortgage

Even before the change in the membership rules, MERS often assigned mortgages to the foreclosing entity so that entity could foreclose. Some borrowers have argued that, as nominee, MERS does not have the power to assign the mortgage. These challenges have been almost universally rejected, as the security instruments expressly authorize MERS, as nominee, to take any action required of its principal and refer to the mortgagee or beneficiary as MERS and its “successors and assigns.” Indeed the First Circuit recently rejected this very argument. See Culhane v. Aurora Loan Services, — F.3d —-, 2013 WL 563374 (1st Cir., Feb. 15, 2013).

Likewise, the fact that an assignment of the security instrument may occur after the transfer of the note is not problematic, and makes sense under the MERS model: “[MERS] members often wait until a default or bankruptcy case is filed to have a mortgage or deed of trust assigned to them so that they can take steps necessary to seek stay relief and/or to foreclose…. [T]he reason they wait is that, if a note is paid off eventually, as most presumably are, MERS is authorized to release the [deed of trust] without going to the expense of ever recording any assignments.”Edelstein, 286 P.3d at 254.

Borrowers have also claimed that MERS lacks authority to assign the note. Since MERS typically does not hold notes, language in MERS assignments referencing the note in addition to the mortgage likely reflects a lack of precision. Insofar as MERS did not hold a note the issue is immaterial.

Splitting” the Note and Mortgage

Some borrowers have alleged that the naming of MERS as holder of title to the mortgage, while the lender holds title to the note, separates the note from the security instrument thereby rendering assignments void and the security instrument unenforceable. As one court has colorfully described it, the debt is the cow, and the mortgage the cow’s tail—while the debt can survive without the security instrument, the instrument has no independent vitality without the debt. See Commonwealth Prop. Advocates, LLC v. MERS, 263 p.3d 397, 403 (Utah App. 2011).

As noted, in Massachusetts, those arguments have been squarely rejected as Massachusetts permits the note and mortgage to be held separately. Indeed the District of Massachusetts remarked that the “MERS system fits perfectly into the Massachusetts model for the separation of legal and beneficial ownership of mortgages.” Culhane v. Aurora Loan Services, 826 F. Supp. 2d 352, 371 (D. Mass. 2011), aff’d — F.3d —-, 2013 WL 563374 (1st Cir. Feb. 15, 2013).

This theory has typically been rejected elsewhere as well, as, if successful, it would “confer[] an unwarranted windfall on the mortgagor.” Id. (citing Restatement (Third) of Prop.: Mortgages § 5.4 cmt. a). In Edelstein, 286 P.3d 249, 255 (Nev. 2012), for example, the court held that in Nevada, “to have standing to foreclose, the current beneficiary of the deed of trust and the current holder of the promissory note must be the same.” However, under the MERS system, the parties agree that MERS holds the security instrument while the note is transferred among its members—as long as the two instruments are united in the foreclosing entity prior to foreclosure, the Nevada court held, the foreclosing entity has standing to foreclose in that state.

Along similar lines, some borrowers allege that operation of MERS makes it impossible to identify who the proper noteholder is, because only the security instrument (not the note) was assigned by MERS. “A ‘show me the note’ plaintiff typically alleges a foreclosure is invalid unless the foreclosing entity produces the original note.” Stein v. Chase Home Fin., LLC, 662 F. 3d 976, 978 (8th Cir. 2011). Of course, when the foreclosing entity is able to produce the note, the claim is typically defeated on summary judgment, id., and many courts considering “show me the note” arguments in the MERS context have dismissed them as a matter of law without any inquiry into note ownership. E.g., Diessner v. MERS, 618 F. Supp. 2d 1184, 1187 (D. Ariz. 2009) (“district courts have routinely held that Plaintiff’s ‘show me the note’ argument lacks merit”) (collecting cases from California, Nevada, and Arizona) (internal quotations omitted).

Unrecorded Assignment Theories

Some states (including Massachusetts after November 1, 2012)statutorily require that, in order to bring a non-judicial foreclosure, all assignments of thesecurity instrument must be recorded. E.g., ORS 86.735(1) (Oregon) (trustee sale may proceed only if “any assignments of the trust deed by the trustee or the beneficiary … are recorded”). In Oregon, a few borrowers have successfully argued that, because the security follows the debt as a matter of law, transfers of the debt while MERS remains lienholder of record result in assignments that go unrecorded, precluding non-judicial foreclosure. See Niday, 284 P. 3d at 1169 (“any assignments” language in ORS 86.735(1) includes “assignment by transfer of the note, ” and that all such assignments from the initial lender to subsequent lenders must be recorded prior to commencement of a non-judicial foreclosure proceeding). Niday is under review by the Supreme Court of Oregon, which heard oral argument on January 8, 2013.

Other courts considering the same argument have rejected it. For instance, Minnesota, Idaho, and Arizona have the same statutory requirement that assignments must be recorded, but have not found note transfers to trigger an obligation to create and record an assignment of the corresponding security instrument. E.g., Jackson v. MERS, 770 N.W.2d 487 (Minn. 2009) (answering “no” to certified question: “Where an entity, such as defendant MERS, serves as mortgagee of record as nominee for a lender and that lender’s successors and assigns and there has been no assignment of the mortgage itself, is an assignment of the ownership of the underlying indebtedness for which the mortgage serves as security an assignment that must be recorded prior to the commencement of a mortgage foreclosure by advertisement under Minn. Stat. ch. 580?”); Homeyer v. Bank of America, N.A.,2012 WL 4105132, at *4 (D. Idaho Aug. 27, 2012) (“Idaho law does not require recording each assignment of a trust deed based upon transfer of the underlying note.”); Ciardi v. Lending Co., Inc., 2010 WL 2079735, at *3 (D. Ariz. May 24, 2010) (“Plaintiffs have failed to cite any Arizona statute that requires the recording of a promissory note or even the assignment of a promissory note.”). These cases ruled that a transfer of a promissory note does not create an “assignment” for purposes of those statutes.

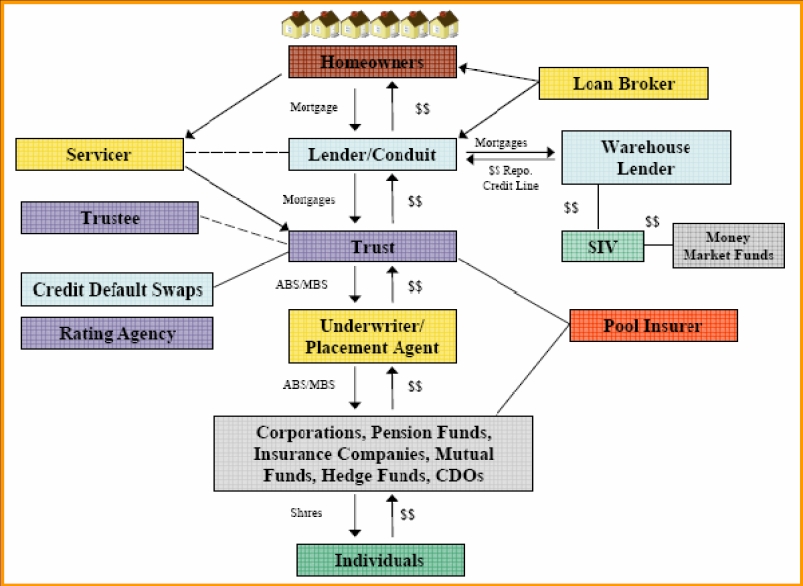

4. Securitization Standing

What is Securitization?

Securitization is the packaging of debt into instruments broadly referred to as “mortgage-backed securities”; one court has described it with analogies: “One could analogize this process to taking raw ingredients and combining them to make bread then selling the slices individually, or putting different kinds of meat into a sausage grinder then selling the individual sausages. What is born from this process are new debt instruments, sold on the open market, that have pooled-and-sliced home loans as their ingredients. Different debt instruments work in different ways, but the basic concept is that home loan debt gets repackaged and sold to other investors rather than being held by the bank that originated the loan.” Bisson v. Bank of America, N.A., — F.Supp.2d —-, 2013 WL 325262, at *1 (W.D. Wash. Jan. 15, 2013). The securitization market emerged to facilitate the inflow of capital to fund home loans, and it “allows banks to spread mortgage risk across the financial system rather than hold it all themselves.” Id.

Although securitization has fallen well off its peak of approximately $1 trillion in originations in 2006, it is projected to rise from $4 billion in 2012 to $25-30 billion in 2013.

There are several parties to a securitization agreement, but the borrower is not one of them. A typical securitization arrangement involves the following parties:

· Originator: The originator is the party identified as “lender” on note and mortgage (or deed of trust).

· Depositor: The depositor is either the originator or someone that buys loans from originators and pools them into securities pursuant to a Pooling and Servicing Agreement (“PSA”) to which the depositor, trustee, and master servicer are parties.

· Trust: Entity into which loans are pooled (e.g., “Structured Asset Securities Corp. Mortgage Pass-Through Certificates, Series 2006-Z”). Sometimes referred to as a “Special Purpose Vehicle,” “Real Estate Mortgage Investment Conduit” or “REMIC,” orsimply a “Mortgage-Backed Security.”

· Trustee/Custodian: The trustee of the securitization trust (not to be confused with the trustee of a deed of trust, which conducts non-judicial foreclosure sales in deed of trust states) holds loans on behalf of the individual security holders, receiving the borrower’s payments from the loan servicer.

· Individual Investors: Shares of mortgage-backed securities are purchased by investors who, when loans are paid on schedule, ultimately benefit from borrowers’ mortgage payments.

· Master Servicer: The master servicer under the PSA services the individual loans in the pool, interfacing with borrowers, collecting loan payments and transferring them to the trust, and often handling foreclosures and post-foreclosure property management.

The Effect of Securitization on Foreclosure

Securitization adds complexity to chain of title to the mortgage, and chain of ownership of the note. See, e.g., In re Almeida, 417 B.R. 140, 142-45 (Bankr. D. Mass. 2009) (describing chain of title to a mortgage securing a securitized note); In re Samuels, 415 B.R. 8, 16-22 (considering challenge to direct assignment of mortgage from originator to trustee, not including an intervening assignment to the trust).

Some borrowers have claimed that insurance contracts or credit default swap agreements preclude default—i.e., the trust was insured against loss, collected the insurance when the borrower defaulted, and should not be allowed to foreclose as well because such foreclosure would grant a “double recovery.” Larota-Florez v. Goldman Sachs Mortg. Co., 719 F. Supp. 2d 636, 642 (E.D. Va. 2010). These arguments have not gained traction. Horvath v. Bank of N.Y., N.A., 641 F.3d 617, 626 n.2 (4th Cir. 2011) (rejecting argument that trustee of securitization trust “should not have been able to foreclose on his property because they did not suffer any losses from his default,” because “that defense does not allow individuals in default on a mortgage to offset their outstanding obligations by pointing to the mortgagee’s unrelated investment income”); Commonwealth, 2011 UT App 232 ¶¶ 3, 10 (rejecting argument “that defendants, having been paid off in the sale of the loan, could not seek a second payoff by foreclosure of the Trust Deed” as a “mere conclusory allegation” that could not sustain a viable claim).

Other borrowers have commissioned “securitization audits,” which purportedly trace the history of the loan in an attempt to cast doubt upon whether the foreclosing entity has standing. These arguments have also generally failed. E.g., Norwood v. Bank of America, 2010 WL 4642447 (Bankr. N.D. Ga. Oct. 25, 2010); Dye v. BAC Home Loans Servicing, LP, 2012 WL 1340220 (D. Or. Apr. 17, 2012) (granting motion to dismiss despite findings of “Mortgage Securitization Audit”). Still other borrowers have challenged the foreclosing entity’s compliance with the PSA. As noted above, borrowers are not parties to these agreements; as such, courts have generally found that borrowers do not have standing to challenge the foreclosing entity’s compliance or lack thereof with it. See, e.g., In re Correia, 452 B.R. 319, 324 (1st Cir. B.A.P. 2011) (stating that debtors, who were not parties to the PSA or third-party beneficiaries thereof, lacked standing to challenge defendants’ compliance with PSA); Sami v. Wells Fargo Bank, 2012 WL 967051, at *5-6 (N.D. Cal. Mar. 21, 2012) (rejecting claim “that Wells Fargo failed to transfer or assign the note or Deed of Trust to the Securitized Trust by the ‘closing date,’ and that therefore, ‘under the PSA, any alleged assignment beyond the specified closing date’ is void”).

Which Securitization Parties May Foreclose?

As discussed above, there are several parties to a securitization. The parties most likely to be involved in a foreclosure are the trustee and servicer. On occasion, foreclosures have been conducted in the name of MERS.

As the party interfacing with the borrowers on a day-to-day basis, the servicer is often in best practical position to handle foreclosure proceedings, but may be required, under some states’ laws, to demonstrate its entitlement to foreclose on behalf of the securitization trustee. So, for example, in Maine, a judicial foreclosure state, the servicer must show its authority to enforce the note. See Bank of America, N.A. v. Cloutier, 2013 WL 453976, at *3 (Me. Feb. 7, 2013) (foreclosure plaintiff must “identify the owner or economic beneficiary of the note and, if the plaintiff is not the owner, to indicate the basis for the plaintiff’s authority to enforce the note pursuant to Article 3-A of the UCC”).

Most non-judicial states do not apply special requirements to loan servicers; the only significant inquiry is whether the trustee of the deed of trust was properly appointed by the beneficiary of record. In Utah, for example, “the statute governing non-judicial foreclosure in Utah does not contain any requirement that the trustee demonstrate his or her authority in order to foreclose. The court declines to create a requirement where the legislature chose not to include one. Therefore, the court holds that, under the terms of the relevant documents and the current statute, [a trustee] is not required to demonstrate its authority to foreclose before initiating a foreclosure proceeding.” Hoverman v. CitiMortgage, Inc., 2011 U.S. Dist. LEXIS 86968, at *16-17 (D. Utah Aug. 4, 2011); see also Trotter, 275 P.3d at 861 (Idaho 2012) (“A trustee is not required to prove it has standing before foreclosing on a deed of trust” as long as “the Appointment of Successor Trustee, Notice of Default, and Notice of Trustee’s Sale complied with the statutoryrequirements and were recorded as specified in the statute”).

The situation can change, however, if the loan becomes involved in a judicial proceeding, such as a bankruptcy. To move for relief from stay in bankruptcy—even in a deed of trust state—a servicer must somehow show authority to enforce the note, though assignment of the security instrument may not be necessary. E.g., In re Tucker, 441 B.R. 638, 645 (Bankr. W.D. Mo. 2010) (“even if, as here, the deed of trust is recorded in the name of the original lender…, the holder of the note, whoever it is, would be entitled to foreclose, even if the deed of trust had not been assigned to it.”). And, conversely, failure to show authority to enforce the note can lead to denial of motions for relief from stay. E.g., In re Wilhelm, 407 B.R. 392 (Bankr. D. Idaho 2009) (denying relief from stay to group of movants that included both servicers and securitization trustees because they presented insufficient proof that they owned the notes in question); In re Mims, 438 B.R. 52, 57 (Bankr. S.D.N.Y. 2010) (servicer that held title to themortgage but did not show it had been assigned the note was not a “real party in interest” in proceeding to lift stay).

In addition to the servicer, the trustee is often the foreclosing party. As the party holding title to the loan on behalf of the loan investors, the trustee is certainly a proper party to foreclose—if it has the right to do so under state law, which may require that it have been formally assigned the mortgage.

In Massachusetts, for instance—and as discussed more above—the trustee must also hold an assignment of the mortgage. In Ibanez, the trustee commenced foreclosures before they had been assigned the mortgages, and did not record assignments until after the foreclosure was completed. The trustee argued it had already received the note when the loan had been securitized years earlier, and that gave it all it needed to foreclose. The court rejected that argument—Massachusetts, as a “title theory” state, requires assignment of mortgage to foreclose. Securitization may have showed intent to assign mortgages, but was not an actual assignment.

Lien-theory states often take a different position, and do not require a trustee to also hold the mortgage, which is nothing more than the right to enforce a lien. See, e.g., Edelstein v. Bank of N.Y. Mellon, 286 P.3d 249, 254 (Nev. 2012);KCB Equities, Inc. v. HSBC Bank USA, N.A. , 2012 Tex. App. LEXIS 4418, at *4-5 (Tex. App.—Dallas).

Conclusion

The recent Massachusetts foreclosure case law is likely some what atypical, driven as it has been by some relatively unusual aspects of Massachusetts law.

But the questions the Massachusetts Supreme Judicial Court has been called upon to answer, concerning the necessary relationship between the lien of the security interest, the debt and the foreclosing creditor, are universal and have been the subject of considerable litigation across the country during the recent “foreclosure crisis.” And the questions are controlled for the most part by state law, and state property and foreclosure law are much less uniform than the law governing the notes themselves as negotiable instruments. This paper has identified the principal issues and arguments so practitioners can ask the right questions and try to determine the law in their particular jurisdiction before proceeding.

For More Information How You Can Use Solid Augments To Effective Challenge and Save Your Home Visit: http://www.fightforeclosure.net