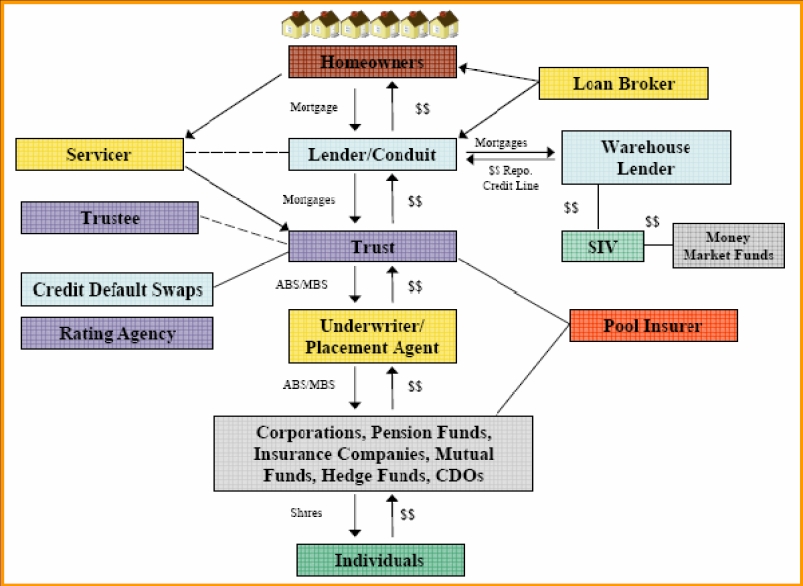

In recent times, we have seen that many foreclosure cases that were litigated by Homeowners involve Mortgage Backed Securities.

Nevada’s foreclosure stats jumped 334 percent in February from the same month a year ago, leading the nation in year-over-year percentage gains, online foreclosure listing service RealtyTrac reported late Wednesday.

Other states with huge spikes in foreclosure activity include Maryland (319 percent), Washington (172 percent), New York (139 percent) and New Jersey (70 percent).

RealtyTrac showed 15,281 foreclosure filings on U.S. properties in February, a 2 percent increase from the previous month but down 25 percent from a year ago. Foreclosure filings include default notices, scheduled auctions and bank repossessions.

Florida had the nation’s highest foreclosure rate for the sixth straight month with one in every 282 housing units receiving a foreclosure filing, more than three times the national average.

Nevada was No. 2 for the fifth straight month with one in every 320 housing units receiving a filing.

“At a high level, the U.S. foreclosure inferno has been effectively contained and should be reduced to a slow burn in the next two years,” said RealtyTrac Vice President Daren Blomquist. “But dangerous foreclosure flare-ups are still popping up in states where foreclosures have been delayed by a lengthy court process or by new legislation making it more difficult to foreclose outside of the court system.”

When Homeowners are faced with a hurdle of fighting foreclosure to save their homes, some of the argument that has been proven effective in the Courts involves Securitization of the mortgages and the assignments involved in the transfer of the mortgages.

The following cases were some of the cases where valid arguments involving securitizations were used to defeat the Banks and Lenders in the Courts. Orders to these cases shows that the case was either Dismissed without Prejudice or Summary Judgment that were reversed on Appeal.

CASE STUDIES:

Augenstein v. Deutsche Bank National Trust Company,

No. 2009-CA-000058-MR, Kentucky Ct. Appeals 2011

Trust: Soundview Home Loan Trust 2005-OPT4

Summary judgment for bank vacated and remanded.

“In this case, the complaint was filed on December 17, 2007, but the assignment of mortgage was not executed until January 3, 2008. Thus, Deutsche Bank had no present interest when it filed its complaint and failed to take any steps to correct this. Allowing Deutsche Bank to commence this action at a time when it lacked standing impermissibly allowed litigation to commence based upon mere expectancy of an interest.”

Bank of America v. Kabba,

276 P.3d 1006, 2012 OK 23

Trust: Structured Asset Investment Loan Trust Series 2004-BNC2

“In the present case, Appellee has only presented evidence of an indorsed-in-blank note and an “Assignment of Mortgage.” Appellee must prove that it is the holder of the note or the nonholder in possession who has the rights of a holder prior to the filing of the foreclosure proceeding. In the present matter the timeliness of the transfer is in question. Since Bank of America did not file the blank indorsement until it filed its motion for summary judgment it is impossible to determine from the record when Bank of America acquired its interest in the underlying note.”

Bank of New York v. Gindele,

1st Dist. No. C-090251, 2010-Ohio-542

Trust: CWALT Alternative Loan Trust 2006-40T1

“A thorough review of the record reveals that the sole indication of its interest as mortgagee is an after-acquired assignment; and the bank failed to produce any evidence in the trial court affirmatively establishing a preexisting interest. Bank of New York has also asserted both that it had acted as an agent, and that its predecessor in interest had later ratified its foreclosure complaint. But because at the time of filing neither agency nor ratification had been alleged or documented, we will not entertain this argument on appeal.”

Bank of NY v. Cupo,

2012 WL 611849 (N.J.Super.App. Div. 2011

Motion to vacate default judgment was reversed for further findings on issue of standing, suggesting that lack of standing might make a judgment void, rather than treating standing as waived by default judgment.

Bank of New York v. Mulligan,

Index 29399/07 (August 25, 2010)

Trust: CWALT 2006-OC1

Mortgage Amount: $392,000

Bank’s application for an order of reference was denied without prejudice.

“The Court will grant plaintiff, BNY an order of reference when it presents: an affidavit by either an officer of BNY or someone with a valid power of attorney from BNY, possessing personal knowledge of the facts; an affidavit from EJy Harless clarifying his employment history for the past three years and what corporation he serves as an officer; and, an affidavit by an officer of BNY, explaining why BNY would purchase a nonperforming loan from MERS, as nominee for DECISION ONE.”

Bank of New York v. Myers,

Index 18236/2008 (February 23, 2009)

Trust: CWABS 2006-22

The Bank’s summary judgment motion was denied, but within 60 days of the decision, the Bank was required to submit an Affidavit from Keri Selman explaining her employment history for the past three years and why Selman did not have a conflict of interest as the signor of many entities.

Bank of New York v. Orosco,

2007 NY SLIP OP 31501(U) (November 19, 2007)

Trust: CWABS, Series 2006-SD2

Mortgage Amount: $436,000

“Plaintiff must address a second matter if it applies for an order of reference after demonstrating that the alleged assignment was recorded. Plaintiff’s application is the third application for an order of reference received by me in the past several days that contain an affidavit from Keri Selman. In the instant action, she alleges to be an Assistant Vice-president of the Bank of New York. On November 16,2007, I denied an application for an order of reference in which Keri Selman, in her affidavit of merit claims to be “Vice President of COUNTRYWIDE HOME LOANS, Attorney in fact for BANK OF NEW YORK.” The Court is concerned that Ms. Selman might be engaged in a subterfuge, wearing various corporate hats. Before granting an application for an order of reference, the Court requires an affidavit from Ms. Selman describing her employment history for the past three years.”

Bank of New York v. Raftogianis,

13 A.3d 435 (2010), 418 N.J.Super. 323

Trust: American Home Mort. Investment Trust 2004-4

Mortgage Amount: $1,380,000

“Plaintiff, however, failed to establish that it was entitled to enforce the note as of the time the complaint was filed. In this case, there are no compelling reasons to permit plaintiff to proceed in this action. Accordingly, the complaint has been dismissed. That dismissal is without prejudice to plaintiff’s right to institute a new action to foreclose at any time, provided that any new complaint must be accompanied by an appropriate certification, executed by one with personal knowledge of the circumstances, confirming that plaintiff is in possession of the original note as of the date any new action is filed. That certification must indicate the physical location of the note and the name of the individual or entity in possession.”

Bank of New York v. Silverberg,

86 AD3d 274, 926 N.Y.S.2d 532 (2d Dept 2011)

Trust: CWALT 2007-14-T2

Mortgage Amount: $479,000

“In sum, because MERS was never the lawful holder or assignee of the notes described and identified in the consolidation agreement, the corrected assignment of mortgage is a nullity, and MERS was without authority to assign the power to foreclose to the plaintiff. Consequently, the plaintiff failed to show that it had standing to foreclose.”

Bank of New York Mellon v. Teague,

Case No. 27-2009-CA-003121, Hernando Co. FL 2012

Trust: Novastar Mortgage Funding Trust 2005-1

“Second, to be entitled to foreclose, Plaintiff had to have been the holder of the Note and Mortgage at the time it filed this lawsuit. The undisputed, summary judgment evidence before the Court was that Plaintiff was not the holder at the inception of this case as Plaintiff did not have the original Note in its possession when it filed suit and the Note did not contain the requisite endorsement. The fact that Plaintiff filed what it contends is an original note on June 28, 2012 does not change this result, as the endorsement on that Note is to a different company, not Plaintiff, and even if the Note had been properly endorsed, the fact that Plaintiff may have been the holder as of June, 2012 does not change its lack of standing at the inception of this case…

The motion is granted and this case is dismissed without prejudice.” (cites omitted)

Bank of New York v. Trezza,

14 Misc. 3d 1201(A), 2006 NY Slip Op 52367(U)

Trust: CWABS 2004-5

“In support of its motion, the plaintiff submits a purported assignment of the mortgage from MERS to the plaintiff; however, the mortgage does not empower MERS to assign the mortgage to any other entity. Furthermore, there is no proof that the Lender had previously assigned the mortgage to MERS, nor is there any other evidence to establish the plaintiff’s ownership rights under the mortgage.

Based on the foregoing, the plaintiff has failed to establish that it has standing as a plaintiff in this matter.”

Bank of New York v. Singh,

Index No. 22434/2007, Kings County (December 14, 2007)

Trust: CWABS, Series 2004-6

An order of reference was denied where the mortgage assignment was executed on June 28, 2007, with an antedated effective date of May 31, 2007. Suit was commenced on June 20, 2007. Judge Kurtz found that such an attempt to retroactively assign the mortgage was insufficient to establish plaintiff’s ownership interest at the time the action was commenced.

Bank of New York v. Torres,

Index No. 31704/2006, Kings County (March 11, 2008)

Trust: CWABS 2005-6

“ORDERED that the plaintiff’s ex parte application for an Order of Reference in Mortgage Foreclosure is denied without prejudice to renew due to plaintiffs failure to demonstrate its ownership of the note and mortgage sufficient to convey standing upon this plaintiff to commence this lawsuit on November 13,2006…”

Beaumont v. Bank of New York Mellon,

81 So.3d 553,554 (Fla. Dist. Ct. App. 2012)

Trust: NovaStar Mortgage Funding Trust 2005-3

Summary judgment for bank reversed and remanded.

“There is no evidence showing that Beaumont was on notice prior to the time his answer was filed that ownership of the note had been transferred from NovaStar to Mellon. In fact, the claimed transfer, alleged to have occurred on the day suit was filed, was either concealed by NovaStar for more than three years while it continued to pursue the action, or NovaStar backdated the assignment it finally produced on July 23, 2010, as justification for substituting Mellon as plaintiff. Under these circumstances, Beaumont may raise lack of standing when suit was filed as a defense.”

Congress v. U.S. Bank,

2100934, AL Ct. Civ. App.

Trust: 2007-EMX1

Mortgage Amount: $104,400

“The trial court should have evaluated the issue whether the allonge had been created after the first trial under the preponderance-of-the-evidence standard. Because it used the higher clear-and-convincing-evidence standard to evaluate Congress’s evidence, this court has no choice but to reverse the trial court’s judgment and remand the cause to the trial court for it to evaluate the evidence adduced at trial under the appropriate standard of proof.”

Cutler v. U.S. Bank, N.A.,

Case No. 2D10-5709 (Fla. 2d DCA 2012)

Trust: Structured Asset Investment Loan Trust, 2006- BNC3

Summary judgment for Bank reversed and remanded.

“Accordingly, a genuine issue of material fact remained as to whether U.S. Bank was the proper holder of the note at the time it initiated the foreclosure action. The note includes the allonge endorsed in blank, but the allonge is not dated. If indeed U.S. Bank cannot establish that the allonge took effect prior to the date of the complaint, it did not have standing to bring suit…

Because a genuine issue of material fact remains, the trial court erred in entering a final summary judgment.”

Davenport v. HSBC Bank USA,

739 N.W.2d 383 (Mich. Ct. App. 2007)

“In this case, defendant did not own the mortgage or an interest in the mortgage on October 27, 2005. Nonetheless, defendant proceeded to commence foreclosure proceedings at that time. Quite simply, defendant did not yet own the indebtedness that it sought to foreclose. The circuit court erred by determining that defendant’s noncompliance with the statutory requirements did not nullify the foreclosure proceedings. Because defendant lacked the statutory authority to foreclose, the foreclosure proceedings were void ab initio. We vacate the foreclosure proceedings and remand for proceedings consistent with this opinion.”

Deutsche Bank National Trust Co.v. Alemany,

Index: 11677/2007

(N.Y. Sup. Ct. Suffolk Co. 2008)

Trust: Soundview Home Loan Trust, 2006-OPT3

“ORDERED that plaintiffs ex parte application for an Order of Reference is denied without prejudice to resubmit due to plaintiffs failure to provide: … (2) proof on standing to commence this action as it appears plaintiff did not own the note and mortgage when the action was commenced…”

Deutsche Bank National Trust Company v. Barnett,

88 A.D.3d 636, 931 N.Y.S.2d 630

Trust: FFMLT 2005-FF11

Summary judgment of foreclosure in favor of bank reversed.

“However, the documentation submitted failed to establish that, prior to commencement of the action, the plaintiff was the holder or assignee of both the note and mortgage. The plaintiff submitted copies of two different versions of an undated allonge which was purportedly affixed to the original note pursuant to UCC 3-202 (2). Moreover, these allonges purporting to endorse the note from First Franklin, a Division of National City Bank of Indiana (hereinafter Franklin of Indiana) to the plaintiff conflict with the copy of the note submitted, which contains undated endorsements from Franklin of Indiana to First Franklin Financial Corporation (hereinafter Franklin Financial), then from Franklin Financial in blank.

“…The plaintiff also failed to establish that the note was physically delivered to it prior to the commencement of this action.”

Deutsche Bank National Trust Company v. Bialobrzeski,

3 A.3d 183 (Conn App. Ct. 2010)

Trust: Long Beach Mortgage Loan Trust 2006-3

The judgment for the trust was reversed and the case was remanded for a hearing on the motion to dismiss.

“The key to resolving the defendant’s claim is a determination of when the note came into the plaintiff’s possession. We cannot review the claim because Judge Domnarski made no factual finding as to when the plaintiff acquired the note. Without that factual determination, we are unable to say whether Judge Domnarski improperly denied the defendant’s motion to dismiss. Although it is the appellant’s responsibility to provide an adequate record for review; see Practice Book §§ 60-5 and 61-10; that cannot be the end of the matter because it concerns the trial court’s subject matter jurisdiction.

Deutsche Bank National Trust Company v. Brumbaugh,

2012 OK 3, 270 P.3d 151

Trust: Long Beach Mortgage Loan Trust 2002-1

Summary judgment for bank reversed and remanded.

“To commence a foreclosure action in Oklahoma, a plaintiff must demonstrate it has a right to enforce the note and, absent a showing of ownership, the plaintiff lacks standing… Being a person entitled to enforce the note is an essential requirement to initiate a foreclosure lawsuit. In the present case, there is a question of fact as to when Appellee became a holder, and thus, a person entitled to enforce the note. Therefore, summary judgment is not appropriate. If Deutsche Bank became a person entitled to enforce the note as either a holder or nonholder in possession who has the rights of a holder after the foreclosure action was filed, then the case may be dismissed without prejudice and the action may be re-filed in the name of the proper party. We reverse the granting of summary judgment by the trial court and remand back for further determinations as to when Appellee acquired its interest in the note.” (cites omitted)

Deutsche Bank National Trust Co. v. Byrams,

2012 OK 4, 275 P.3d 129

Trust: Argent Securities, Inc. ABPT Certs., Series 2006-W2

Mortgage amount: $526,320

Summary judgment of foreclosure in favor of bank reversed and remanded.

“The assignment of a mortgage is not the same as an assignment of the note. If a person is trying to establish it is a nonholder in possession who has the rights of a holder it must bear the burden of establishing its status as a nonholder in possession with the rights of a holder. Appellee must establish delivery of the note as well as the purpose of that delivery. In the present case, it appears Appellee is trying to use the assignment of mortgage in order to establish the purpose of delivery. The assignment of mortgage purports to transfer “the following described mortgage, securing the payment of a certain promissory note(s) for the sum listed below, together with all rights therein and thereto, all liens created or secured thereby, all obligations therein described, the money due and to become due thereon with interest, and all rights accrued or to accrue under such mortgage.” This language has been determined by other jurisdictions to not effect an assignment of a note but to be useful only in identifying the mortgage. Therefore, this language is neither proof of transfer of the note nor proof of the purpose of any alleged transfer.” (cites omitted)

Deutsche Bank National Trust Company v. Cabaroy,

Index: 9245/2007

(N.Y. Sup. Ct. Suffolk Co. 2008)

Trust: New Century Home Equity Loan Trust, 2006-1

“ORDERED that the plaintiffs ex parte application for an Order of Reference in Mortgage Foreclosure is denied without prejudice to resubmit due to plaintiffs failure to provide: (1) proof of plaintiffs standing to commence this action;”

Deutsche Bank National Trust Company v. Castellanos,

2008 NY Slip Op 50033(U)

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Argent Mort. Sec., Inc. ABPT Certs., Series 2005-W4

Mortgage Amount: $382,500

“Did Mr. Rivas somehow change employers on July 21, 2006 or he is concurrently a Vice President of both assignor Argent Mortgage Company, LLC and assignee Deutsche Bank? If he is a Vice President of both the assignor and the assignee, this would create a conflict of interest and render the July 21, 2006-assignment void.

Also, Mr. Rivas claims that Argent Mortgage Company, LLC is located at 1100

Town and Country Road, Suite 200, Orange, California, while Deutsche Bank has its offices at One City Boulevard West, Orange, California. Did Mr. Rivas execute the assignment at 100 Town and Country Road, Suite 200, and then travel to One City Boulevard West, with the same notary public, M. Reveles, in tow? The Court is concerned that there may be fraud on the part of Deutsche Bank, Argent Mortgage Company, LLC, and/or MTGLQ Investors, L.P., or at least malfeasance. If plaintiff renews its motion for a judgment of foreclosure and sale, the Court requires a satisfactory explanation by Mr. Rivas of his recent employment history.”

Deutsche Bank National Trust Co. v. Clouden,

Index No. 277/07

(N.Y. Sup. Ct. Kings Co. 2007)

Trust: Argent Mort. Sec., Inc. ABPT Certs., Series 2005-W3

Mortgage Amount: $382,500

“In the instant action, Argent’s defective assignment to Deutsche Bank affects the standing of Deutsche Bank to bring this action. The recorded assignment from Argent to Deutsche Bank, made by “Tamara Price, as Authorized Agent” on behalf of “AMC Mortgage Services Inc. as authorized agent,” lacks any power of attorney granted by Argent to AMC Mortgage Services, Inc. and/or Tamara Price to act on its behalf.”

Deutsche Bank National Trust Company v. Benjamin Cruz,

Index No. 31645/06

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Soundview Home Loan Trust 2005-OPT3

“In support of plaintiff’s application, it submits a purported assignment of the mortgage from the original lender to plaintiff. The purported assignment is dated October 27, 2006. However, such an attempt to retroactively assign the mortgage is insufficient to establish plaintiff’s ownership interest at the time the action was commenced.”

Deutsche Bank National Trust Company v. Yobanna Cruz,

Index No. 2085/07

(N.Y. Sup. Ct. Kings Co. 2007)

Trust: Long Beach Mort. Loan Trust 2006-2

Mortgage Amount: $382,500

“In support of plaintiffs application, it submits a purported assignment of the mortgage from the original lender to plaintiff. The purported assignment is dated January 18, 2007 and states in pertinent part “effective January 12, 2007.” However, such an attempt to retroactively assign the mortgage is insufficient to establish plaintiff’s ownership interest at the time the action was commenced.”

Deutsche Bank National Trust Company v. Cuesta,

2012 NY Slip Op 32590(U) (N.Y. Sup. Ct. Suffolk Co. 2012)

Trust: American Home Mortgage Investment Trust,

Series 2007-2

Deutsche Bank’s motion for an order of reference was denied without prejudice, and Deutsche Bank was warned that if it chose to refile, it must include:

“4) Evidentiary proof, including an affidavit from an individual with personal knowledge of the facts as to the proper and timely assignment of the subject note and mortgage or endorsement of the subject note and assignment of the subject mortgage, sufficient to establish that plaintiff was the owner or holder of the subject note and mortgage at the time the action was commenced…

In his affidavit, the plaintiff’s representative has not addressed the particulars of the transfer of the note or the assignment of the mortgage to the plaintiff. Additionally, the assignment dated January 27, 2011, which is referred to in the plaintiff’s complaint, has not been attached to the moving papers.”

Deutsche Bank v. Decker,

Case 09-20548-CI-13 (Pinellas County, Florida, 2010)

Trust: Morgan Stanley Dean Witter Cap. PSA dated 5-1- 2001

“However, there remain two concerns.

The first is related to evidence that the Plaintiff had standing at the time the original complaint was initially filed. The “new” assignment does not solve this problem because it was executed on February 17, 2010, and thus does not demonstrate standing in 2009…

The second problem is related to the ownership issue but is focused on the validity of the newly obtained assignment. At the hearing Defendant’s counsel indicated concerns regarding this document based upon his assertion that the 2010 assignment was from a company that went bankrupt years ago…”

(Dismissal granted of bank/plaintiff’s first amended complaint)

Deutsche Bank National Trust Co. v. Ezagui,

Index: 3724/07

(N.Y. Sup. Ct. Kings Co. 2007)

Trust: Ameriquest Mortgage Securities, Inc., ABPT

Certificates, Series 2004-R10

Mortgage Amount: $412,250

“According to plaintiff’s application, defendant Ezaguis’ default began with the nonpayment of principal and interest due on September 1, 2006. Yet, more than five months later, plaintiff DEUTSCHE BANK was willing to take an assignment of a nonperforming loan from AMERIQUEST. Further, both assignor AMC, as Attorney in Fact for AMERIQUEST, and assignee, DEUTSCHE BANK, have the same address, 505 City Parkway West, Orange, CA 92868. Plaintiff’s “affidavit of amount due,” submitted in support of the instant application for a default order of reference was executed by Tamara Price, on February 16, 2007. Ms. Price states that “I am the Vice President for DEUTSCHE BANK NATIONAL TRUST COMPANY, AS TRUSTEE OF AMERIQUEST MORTGAGE SECURITIES, INC., ASSET-BACKED PASS THROUGH CERTIFICATES, SERIES 2004-R10, UNDER THE POOLING AND SERVICING AGREEMENT DATED AS OF OCTOBER 1, 2004, WITHOUT RECOURSE (DEUTSCHE BANK).” However, the February 7, 2007 assignment from AMERIQUEST, by AMC, its Attorney in Fact, is executed by Tamara Price, Vice President of AMC. The Tamara Price signatures on both the February 7, 2007 affidavit and the February 16, 2007 assignment are identical. Did Ms. Price change employers from February 7, 2007 to February 16, 2007? The Court is concerned that there may be fraud on the part of AMERIQUEST, or at least malfeasance. Before granting an application for an order of reference, the Court requires an affidavit from Ms. Price, describing her employment history for the past three years. Further, irrespective of her employment history, Ms. Price must explain why DEUTSCHE BANK would purchase a nonperforming loan from AMERIQUEST, and why DEUTSCHE BANK shares office space in Orange, California, with AMERIQUEST.”

Deutsche Bank National Trust Company v. Gilbert,

2012 IL App (2d) 120164, No. 2-12-0164 (September 25, 2012)

Trust: GSAMP Trust 2005-WMC2

“Deutsche Bank attempted to rebut this apparent lack of standing by pointing to the Assignment and the Loch affidavit. However, these items lack evidentiary value. Before the trial court, Deutsche Bank argued that the language of the Assignment established that the transfer of the mortgage had occurred years earlier, on November 1, 2005. On appeal, however, Deutsche Bank wisely abandons that argument (which finds no support in the actual language of the Assignment), and now concedes that the Assignment “does not establish anything about when Plaintiff [Deutsche Bank] obtained its interest in the subject loan.” We agree with this statement. Although the Assignment contains two dates—the date of the trust for which Deutsche Bank is a trustee, and the date on which the Assignment was executed and notarized—it does not explicitly state when the mortgage was assigned to Deutsche Bank. All that can be known about when the assignment took place is that it was no later than the date on which the Assignment was executed.”

Deutsche Bank National Trust Company v. Grant,

Index: 39192/07

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Soundview Home Loan Trust 2006-OPT2

Mortgage Amount: $456,000

“Also, the Court requires an explanation from an officer of plaintiff DEUTSCHE BANK as to why, in the middle of our national subprime mortgage financial crisis, DEUTSCHE BANK purchased a non-performing loan [from] OPTION ONE. The Court wonders if DEUTSCHE BANK violated a corporate fiduciary duty to its stockholders with the purchase of a loan that defaulted more than five months prior to its assignment to DEUTSCHE BANK.”

Deutsche Bank National Trust Co. v. Haque,

36 Misc. 3d 1203(A)

(N.Y. Sup. Ct. Queens Co. 2012)

Trust: Home Equity Mortgage Loan Trust, Series INABS

2005-B

Mortgage Amount: $279,200

“In addition, to the extent Plaintiff Deutsche Bank asserts the note was transferred to ”the trust,” pursuant to a “pooling and servicing” agreement between IndyMac ABS, Inc. as depositor, IndyMac Bank SM as seller and “master servicer” and Home Equity Mortgage Loan Asset-Backed Trust, Series INABS 2005-B, issuer, such agreement does not establish that IndyMac assigned the note to plaintiff Deutsche Bank. Plaintiff Deutsche Bank does not otherwise allege a basis for a valid assignment of the note.” (cites omitted)

Deutsche Bank National Trust Co. v. Harris,

Index: 35549/07

(N.Y. Sup. Ct. Kings Co. 2008)

Mortgage Amount: $408,000

Deutsche Bank’s Motion was denied without prejudice, with leave to renew, providing the Court:

“…a satisfactory explanation to various questions with respect to: the October 23, 2007 assignment of the instant mortgage to plaintiff, DEUTSCHE BANK NATIONAL TRUST COMPANY (DEUTSCHE BANK); the employment history of one Erica Johnson-Seck, who executed the affidavit of facts in the instant application as an officer of DEUTSCHE BANK; plaintiff DEUTSCHE BANK’S purchase of the instant non- performing loan; and why does INDYMAC BANK, F.S.B., (INDYMAC), MORTGAGE ELECTRONIC REGISTRATION SYSTEMS, INC. (MERS), and plaintiff DEUTSCHE BANK all share office space at 460 Sierra Madre Villa, Pasadena, CA 91107.”

Deutsche Bank National Trust Co. v. Maraj,

2008 NY Slip Op 50176 (U)

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: INDX 2006-AR6

Mortgage Amount: $440,000

“With the assignor MERS and assignee DEUTSCHE BANK appearing to be engaged in possible fraudulent activity by: having the same person execute the assignment and then the affidavit of facts in support of the instant application; DEUTSCHE BANK’s purchase of a non-performing loan from INDYMAC; and, the sharing of office space in Suite 400/500 in Kansas City, the Court wonders if the instant foreclosure action is a corporate “Kansas City Shuffle,” a complex confidence game…

A Kansas City Shuffle is when everybody looks right, you go left . . .

It’s not something people hear about. Falls on deaf ears mostly . . .

No small matter. Requires a lot of planning. Involves a lot of people. People connected by the slightest of events. Like whispers in the night, in that place that never forgets, even when those people do.

In this foreclosure action is plaintiff DEUTSCHE BANK, with its “principal place of business” in Kansas City attempting to make the Court look right while it goes left?”

Deutsche Bank National Trust Co. v. Marche,

Index: 9156/07

(N.Y. Sup. Ct. Kings Co. 2009)

Trust: Securitized AB Receivable LLC Trust 2006-FR4

“Why an Order should not be made and entered:

VACATING the order of foreclosure and dismissing the instant action in its entirety upon the grounds that (i) Plaintiff has misrepresented itself by alleging that it is the owner and holder of the mortgage in order to fraudulently commence this action when in fact no valid assignment has been made to Plaintiff from Fremont Investment & Loan; (ii) that this Court lacks subject matter jurisdiction where Plaintiff is not and has not been the true owner and holder of the note and mortgage at issue; and (iii) that the assignment at issue is champertous in violation of Section 489 of the New York State Judiciary Law because the sole purpose of the defective assignment was to facilitate fraudulent litigation begun by Plaintiff prior to the assignment’s execution.”

Deutsche Bank National Trust Co. v. Matthews,

2012 OK 14, 273 P.3d 43 (2012)

Trust: JP Morgan Mortgage Acquisition Trust 2007-CH3

Summary Judgment for bank reversed and remanded.

“However, the Assignment of Real Estate Mortgage attached to its motion for summary judgment is executed on June 9, 2009, by a Vice President of Chase Bank USA, N.A. The note attached to its motion for summary judgment, however, shows an allonge from Chase Bank USA, N.A., to Chase Home Finance, LLC. Further, this purported transfer of the note occurred six months after the action was commenced. Deutsche Bank also by its own admission states it acquired its interest in the note and mortgage subsequent to the filing of this action.”

Deutsche Bank v. McCarthy,

Case No. 1:07 3071 (N.D. Ohio) (Judge Dowd)

Trust: Argent Mortgage Securities, ABPT Certs., Series 2005-W5

“The Northern District of Ohio is swamped with foreclosure cases brought in diversity. A large number of these cases are brought by plaintiffs who declare that they are holders of the note and mortgage but who initially supply no proof of that fact. When pressed, it is typically the case, as here, that the plaintiff actually is not the holder of the note and mortgage until some time after the filing of the complaint (often mere days!) and had, therefore, made a false statement to the court. Sometimes that statement of ownership is only in the complaint; sometimes, as in the instant case, it is actually in a sworn affidavit. See Doc. No. 1-4, ¶ 7. This is completely unacceptable, especially because this situation is likely to be repeated if not stopped by Court order.”

Deutsche Bank National Trust Company v. McRae

27 Misc.3d 247 (Sup. Ct. Alleghany County 2010)

Trust: not identified.

To establish standing, the bank submitted an additional copy of a note which was different from the one attached to the complaint. The court rejected it, stating: “Obviously, the endorsements…post-date the commencement of this case…and are ineffective.”

Deutsche Bank National Trust Co. v. Mitchell,

27 A.3d 1229 – NJ Appellate Div. 2011

Trust: Long Beach Mortgage Loan Trust 2006-3

Mortgage Amount: $150,000

Summary judgment reversed.

“After reviewing the record in light of the contentions advanced on appeal, we reverse the grant of summary judgment and final judgment and vacate the sheriff’s sale, holding that Deutsche Bank did not prove it had standing at the time it filed the original complaint. The assignment was not perfected until after the filing of the complaint, and plaintiff presented no evidence of having possessed the underlying note prior to filing the complaint. If plaintiff did not have the note when it filed the original complaint, it lacked standing to do so, and it could not obtain standing by filing an amended complaint. Given that Deutsche Bank has not demonstrated standing, we cannot decide at this time whether it was a holder in due course of the mortgage.”

Deutsche Bank National Trust Co. v. Nicholls.

Index 2248/07

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Long Beach Mort. Loan Trust 2005-WL2

“In support of plaintiff’s application, it submits a purported assignment of the mortgage from the original lender to plaintiff. The purported assignment is dated January 24, 2007 and states in pertinent part “[e]ffective January 17, 2007.” However, such an attempt to retroactively assign the mortgage is insufficient to establish plaintiff’s ownership interest at the time the action was commenced. … Plaintiffs attempt to foreclose upon a mortgage in which it had no “legal or equitable interest was without foundation in law or fact…”

Deutsche Bank National Trust Company v. Parisella,

VT App. Ct., 2010, Docket No. S0758-09 CnC

Trust: FFMLT Trust 2005-FF11

Homeowner’s Motion to Dismiss granted.

“The court concludes that a plaintiff seeking foreclosure lacks standing unless it can show it was entitled to enforce the mortgage at the time it filed its complaint for foreclosure…

Here, there is no evidence in the record indicating that Deutsche Bank was the assignee of the note when it filed its complaint on June 15, 2009. Nor is there even an allegation to that effect. There is an allegation that the mortgage was assigned to Deutsche Bank before it filed its complaint, but since the note is a negotiable instrument, the transfer of the mortgage does not also transfer the note…

Deutsche Bank National Trust Company v. Richardson,

2012 OK 15, __P.3d__

Trust: MASTR 2007-02

Summary Judgment for bank reversed and remanded.

“In the present case, Appellee has presented evidence in support of the motion for summary judgment of an indorsed-in-blank note, and an “Assignment of Mortgage” both arguably obtained after the filing of the petition. Appellee must prove it is the holder of the note or the nonholder in possession who has the rights of a holder prior to the filing of the foreclosure proceeding. In the present matter the timeliness of the transfer is a disputed fact issue. Since Deutsche Bank did not file the blank indorsement until it filed its motion for summary judgment it is impossible to determine from the record when Deutsche Bank acquired its interest in the underlying note.”

Deutsche Bank National Trust Co. v. Ryan,

Index 33315/07 (January 29, 2008)

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Long Beach Mort. Loan Trust 2005-WL1

An order of reference was denied by Judge Kurtz where the bank plead a mortgage assignment executed, September 31, 2007, after the suit was commenced August 31, 2007, but with an attempted backdate to July 30, 2007.

Deutsche Bank National Trust Co. v. Ryan,

Case No. 2011-12070, Hillsborough Co. Fla. 2012

Trust: Novastar Mortgage Funding Trust, 2006-5

“Second, Plaintiff lacked standing at the inception of this case. Though Plaintiff alleged it had standing, the Note attached to its Complaint lacked an endorsement, and Plaintiff introduced no sworn evidence to overcome Defendant’s affidavit that it lacked standing when it filed suit…

In light of the foregoing, this case is dismissed without prejudice and without leave to amend.”

Deutsche Bank National Trust Co. v. Sampson III,

Index 26320/07 (January 16, 2008)

(N.Y. Sup. Ct. Kings Co. 2009)

Trust: HSBC Bank USA, Inc., Series HASCO 2006-HE1

“The purported assignment is dated August 10, 2007 and states in pertinent part “this assignment is effective as of the 22nd day of June, 2007.” However, such an attempt to retroactively assign the mortgage is insufficient to establish plaintiff’s ownership interest at the time the action was commenced. Plaintiff’s attempt to foreclose upon a mortgage in which it had no “legal or equitable interest was without foundation in law or fact…” (cites omitted)

Deutsche Bank National Trust Company v. Seidlin,

Index:105162/2009 NY County, 2011NY Slip Op

31551(U)

Trust: American Home Mortgage Assets Trust 2006-5

Mortgage Amount: $580,000

Bank’s motion granted for leave to voluntarily discontinue the action “due to the assignment of mortgage being incorrectly and/or incompletely acknowledged” after two years of litigation.

Deutsche Bank National Trust Co. v. Steele,

2008 U.S. Dist. LEXIS 4937 (S.D. Ohio January 8, 2008)

“I cannot tell from the exhibits plaintiff has submitted in support of its motion whether Deutsche Bank owned the note and mortgage when the complaint was filed. Plaintiff alleges ownership in the complaint, but defendants’ answer does not admit the truth of that allegation…The Court cannot grant summary judgment unless Deutsche Bank offers evidence from which a finder could conclude by a preponderance that it owned the note and mortgage when the complaint was filed. Further, if plaintiff has evidence of ownership, it must explain how that ownership is consistent with the uncontroverted evidence that when the complaint was filed, MERS was the mortgage holder acting on behalf of Mortgageit, Inc.”

Deutsche Bank National Trust Company v. Vasquez,

Index: 4924/11, 2012 NY Slip Op 31395(U)

Trust: Morgan Stanley ABS Cap. I, Inc. Trust, 2007-HE7

Mortgage Amount: $435,100

“A foreclosure plaintiff has the requisite standing to commence a mortgage foreclosure action if “it is both the holder or assignee of the subject mortgage and the of the underlying note at the time the action is commenced”… In this action plaintiff does not allege that it is an assignee of the Note, but instead, as previously referenced, produced a copy of the original Note between defendants and New Century. They argue that delivery of the unindorsed Note was sufficient to confer standing. On the prior motion the court overlooked the necessity of proper indorsement required to transfer ownership and render the transferee a holder…

Also influencing this court’s determination on reargument are the repeated issues regarding standing which revolve around proper assignments, particularly of mortgage notes which have ensued following creation of the MERS system and the birth of mortgage backed securities.”

Deutsche Bank National Trust Company v. Williams,

Case No. 11-00632 (D. Hawaii 2011)

Trust: Morgan Stanley ABS Capital I, Inc. Trust 2007- NC1

“This evidence presents two problems for Plaintiff. First, if Plaintiff did indeed obtain the Mortgage and Note through a 2007 PSA, then the 2007 PSA is yet another reason why the January 13, 2009 assignment is a nullity and the Complaint’s assertion that Plaintiff obtained the Mortgage and Note from Home 123 is untrue. Second, the evidence presented does not actually establish that Plaintiff received the Mortgage and Note through the PSA — there is no evidence on the record establishing what mortgages were included in the PSA. Thus, although Plaintiff might have obtained the Mortgage and Note through this PSA, there is no evidence showing or even suggesting that this is indeed the case. As a result, there is no evidence — at least on the record presented before the court –creating a genuine issue of material fact that Plaintiff was assigned the Mortgage and Note on which it now seeks to foreclose.”

Deutsche Bank National Trust Company v. Wilson,

Case A-1384-09T1, N.J. App. Div. 2011

Trust: WaMu 2007-HEI Trust

Summary judgment of foreclosure was reversed and remanded “to resolve the issue of the bona fides of the assignment.” The issue regarding the assignment was discussed in Footnote 1:

“The assignment was executed by an individual identified as Laura Hescott who signed the assignment as an assistant vice-president of Washington Mutual Bank. Ms. Hescott has been identified as an employee of Lender Processing Services, Inc. (“LPS”), a servicer of default mortgages. The bona fides of the practices of this service provider have been the subject of increased judicial scrutiny. See, e.g., In re Taylor, 407 B.R. 618, 623 (Bankr. E.D. Pa. 2009).”

Deutsche Bank Trust Company Americas v. McCoy,

20 Misc 3d 1202 (A) 2010 NY Slip Op 51664(U)

Trust not disclosed.

“Although the February 28, 2008 assignment states it is “effective January 19, 2008,” such attempt at retroactivity is ineffectual. If an assignment is in writing, the execution date is generally controlling and a written assignment claiming an earlier effective date is deficient, unless it is accompanied by proof that the physical delivery of the note and mortgage was, in fact, previously effectuated…A retroactive assignment cannot be used to confer standing upon the assignee in a foreclosure action commenced prior to the execution of the assignment… (Plaintiff’s failure to submit proper proof, including an affidavit from one with personal knowledge, that the plaintiff was the holder of the note and mortgage at the time the action was commenced, requires denial of the plaintiff’s application for an order of reference. (cites omitted)

Deutsche Bank Trust Company Americas v. Peabody,

866 N.Y.S. 2d 91 (N.Y. Sup. Ct. 2008)

Trust not disclosed.

Mortgage Amount: $320,000

Foreclosure dismissed.

“Again, here, there is no evidence that it took physical delivery of the note and mortgage before commencing this action, and again, the written assignment was signed after the defendant was served. The assignment’s language purporting to give it retroactive effect, absent a prior or contemporary delivery of the note and mortgage, is insufficient to grant it standing.”

Feltus v. U.S. Bank, N.A.

80 So.3d 375 (Fla. 2nd DCA 2011)

Trust: MASTR Adj. Rate Mortgage Trust 2007-3

Summary judgment for bank reversed.

“The properly filed pleadings before the court when it heard U.S. Bank’s motion for summary judgment were a complaint seeking to reestablish a lost note to which was attached a copy of a note made payable to Countrywide, N.A., Feltus’s answer and affirmative defenses alleging that the note attached to the complaint contradicts the allegation of the complaint that U.S. Bank is the owner of the note, a motion for summary judgment alleging a lost note of which U.S. Bank is the owner, and an affidavit of indebtedness alleging that U.S. Bank was the owner and holder of the note described in the complaint. The endorsed note that U.S. Bank claimed was now in its possession was not properly before the court at the summary judgment hearing because U.S. Bank never properly amended its complaint.2 In addition, the complaint failed to allege that U.S. Bank “was entitled to enforce the instrument when loss of possession occurred, or has directly or indirectly acquired ownership of the instrument from a person who was entitled to enforce the instrument when loss of possession occurred.” § 673.3091(a). The affidavit of indebtedness provided no assistance in this regard because the affiant did not assert any personal knowledge of how U.S. Bank would have come to own or hold the note.” (cites omitted)

Federal Home Loan Mortgage Corporation v. Schwartwald,

Slip Opinion No. 2012-Ohio-5017

On October 31, 2012, the Ohio Supreme Court addressed the issue of standing in foreclosures. Although this case did not involve a mortgage-backed trust, it will have a significant impact on foreclosures by trusts because the Court ruled that the Federal Home Loan Mortgage Corporation lacked standing to sue when it obtained the mortgage by an assignment from the real party in interest after the foreclosure suit was commenced. This was yet another case where the note was “not available” at commencement. Later in the case, Federal Home Loan filed a copy of the note, with undated endorsements. The motion for summary judgment was supported by an Affidavit signed by well-known Wells Fargo robo-signer John Herman Kennerty. The appellate court had ruled that Federal Home Loan cured the lack of standing defect by the assignment of the mortgage and transfer of the note prior to entry of judgment. The Ohio Supreme Court disagreed – citing decisions taken by Courts in Connecticut, Florida, Maine, Missouri, Oklahoma and Vermont.

Gascue v. HSBC USA, N.A.,

__So.3d__ (Fla. 4th DCA 2012)

Trust: Deutsche Alt-B Securities Mortgage Loan Trust, Series 2006-AB4

Reversal and remand of denial of motion to vacate final judgment of foreclosure.

“There is no evidence on the record indicating that Bank was the holder of the mortgage at the time the complaint was filed. Just as in Rigby, Bank attached a mortgage to its complaint in which it was not listed as the lender, but rather “Pinnacle Direct Funding” was. The only evidence that Bank is the owner and holder of the note is a sworn affidavit. However, this affidavit was filed three years after the complaint and does not establish when Bank became the holder of either the note or the mortgage, much less establish that Bank was the holder of said instruments at the time the complaint was filed. See id. (reversing the trial court in part because the supporting affidavit in that case did not establish the date on which the bank acquired possession of the note).”

Gee v. U.S. Bank, N.A.,

72 So.3d 211 (Fla. 5th DCA 2011)

Trust: Structured Asset Investment Loan Trust 2005-10

“Here, the record does not contain the original Mortgage. To prove its ownership, U.S. Bank filed a copy of the Mortgage as well as two assignments. The first assignment transferred the Mortgage from Advent Mortgage, the original mortgagee, to Option One. The second assignment purported to transfer the mortgage from American Home, as successor in interest of Option One, to U.S. Bank. However, and significant to our consideration, U.S. Bank provided nothing to demonstrate how American Home came to be the successor in interest to Option One.

Incredibly, U.S. Bank argues that “[i]t would be inequitable for [Ms. Gee] to avoid foreclosure based on the absence of an endorsement to [it].” But that argument flies in the face of well-established precedent requiring the party seeking foreclosure to present evidence that it owns and holds the note and mortgage in question in order to proceed with a foreclosure action.” (cites omitted)

(Summary Judgment reversed.)

Gonzalez v. Deutsche Bank National Trust Company,

Case No. 2D10-5561 (Fla. 2d DCA 2012)

Trust: American Home Mortgage Investment Trust

2006-1

“The problem is that the additional stamp and handwritten notation transferring the note from American Home Mortgage to Deutsche Bank is not dated. Accordingly, Deutsche Bank failed to establish its standing by showing that it possessed the note when it filed the lawsuit. See Country Place Cmty. Ass’n v. J.P. Morgan Mortg. Acquisition Corp., 51 So. 3d 1176, 1179 (Fla. 2d DCA 2010) (“Because J.P. Morgan did not own or possess the note and mortgage when it filed its lawsuit, it lacked standing to maintain the foreclosure action.”). As a result, Deutsche Bank has not refuted Gonzalez’s affirmative defense, and a genuine issue of material fact exists that should have precluded the entry of summary judgment.”

(Summary judgment for Deutsche Bank reversed.)

HSBC Bank USA, N.A. v. Antrobus,

20 Misc 3d 1127(A), 2008 NY Slip Op 51639(U)

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Renaissance Home Equity Loan Trust 2006-4

Mortgage Amount: $465,000

“Therefore, the instant application for an order of reference is denied without prejudice, with leave to renew. The Court will grant an order of reference to plaintiff HSBC upon presentation to this court of: an affidavit by either an officer of HSBC or someone with a valid power of attorney from HSBC, possessing personal knowledge of the facts; an affidavit from Scott Anderson clarifying his employment history for the past three years and what corporation he serves as an officer; and, an affidavit by an officer of HSBC explaining why HSBC purchased a nonperforming loan from Delta Funding Corporation, and why HSBC, OCWEN, MERS, Deutsche Bank and Goldman Sachs all share office space in Suite 100.”

HSBC Bank USA v. Beirne,

212-Ohio-1386, Ohio App. Ct. 9th District

Summary judgment for bank reversed.

“In the affidavit that was attached to the supplement to the motion for summary judgment, Mr. Spradling averred that HSBC had been assigned the loan on June 5, 2009, and that “[a] true and correct copy of the Assignment was attached to the Complaint filed by HSBC.” However, a review of the complaint and the exhibits attached thereto reveals that there was no evidence that the note had been assigned to HSBC. Moreover, an assignment dated June 5, 2009, could not have been attached to the complaint which was filed on May 11, 2009.”

HSBC Bank USA, N.A. v. Charlevagne,

20 Misc 3d 1128(A), 2008 NY Slip Op 51652(U)

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Renaissance Home Equity Loan Trust 2005-3

Mortgage Amount: $480,000

“Therefore, the instant application for an order of reference and related relief is denied without prejudice. The Court will grant plaintiff HSBC an order of reference and related relief when it submits an affidavit by either an officer of HSBC, or someone with a valid power of attorney from HSBC, possessing personal knowledge of the facts.”

HSBC Bank USA v. Cherry,

18 Misc3d 1102 (A), 2007 NY Slip Op 52378(U)

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Renaissance Home Equity Loan Trust 2005-4

“Further, the Court, upon renewal of the application for an order of reference requires a satisfactory explanation to questions with respect to: the assignment of the instant nonperforming mortgage loan from the original lender, Delta Funding Corporation to HSBC Bank; the employment history of one Scott Anderson, who assigned this mortgage to HSBC and then swears to be HSBC’s servicing agent; and the relationship between HSBC, Ocwen Federal Bank, FSB (OCWEN), Deutsche Bank and Goldman Sachs, who all seem to share office space at Suite 100 of 1661 Worthington Road, West Palm Beach, Florida 33409 (Suite 100).”

HSBC Bank USA v. Cipriani,

Index: 12365-2007

(N.Y. Sup. Ct. Suffolk Co. 2008)

Trust: SG Mort. Sec. Trust 2005-OPT1

Order for reference denied without prejudice. To resubmit, plaintiff must provide “proof on standing to commence this action as it appears that the plaintiff did not own the note and mortgage when the action was commenced.”

HSBC Mortgage Services, Inc. v. Jack,

Index No: 14750/2007

(N.Y. Sup. Ct. Suffolk County 2008)

Denied without prejudice due to bank’s failure to provide proof that it had standing to bring the action.

HSBC Bank USA v. Palladino,

2011 IL App (2d) No. 08-CH-4548

Trust: Fremont Home Loan Trust 2006-D

Summary judgment reversed and remanded.

“In the present case, there are genuine issues of material fact with respect to whether there was an assignment of the mortgage and note from Fremont to HSBC Bank. Although HSBC Bank represents that it produced the assignment, the document on which it relies, by its very terms, was, at worst, not an assignment and, at best, inherently inconsistent as to whether it was an assignment. Indeed, the document states that MERS as nominee for Fremont “did” assign (past tense) the mortgage and note to HSBC Bank prior to November 13, 2008, yet also states that the assignment “is” made (present tense) without recourse and without representation or warranty.

In addition to the purported assignment’s inconsistent terms, the document upon which HSBC Bank relies is vague with respect to the date of the purported assignment. The document has a stamp which appears to reflect that it was recorded on December 17, 2008, but states that the assignment was made “prior to” November 13, 2008. The document itself is undated, as is the notary’s certificate. The date of the assignment is material because standing to sue must exist at the time the action is commenced.” (cites omitted)

HSBC Bank USA v. Perez,

Case No. EQ4970 (Washington County, Iowa 2009)

Trust: Fieldstone Mort. Investment Trust 2005-2

“The Perezs argue that the Pooling and Servicing Agreement for Fieldstone Mortgage Investment Trust Series 2005-2 governs when and how the Trustee in this case, HSBC Bank, the Plaintiff, may acquire notes and mortgages. Additionally, that agreement governs when and how a mortgage owned by the trust may be foreclosed upon. The Perezs further state that the agreement prohibits the acquisition of mortgages that are in default…The Plaintiff has also submitted documentation that shows the transfer of interest in the mortgage from Fieldstone to HSBC occurred on February 9, 2009. Clearly, based upon the Plaintiff’s own documentation, the default occurred prior to the transfer.

According to the Transfer and Servicing Agreement submitted by the Perezs, and allegedly applicable to the Plaintiff, the trust servicer is only allowed to “substitute a defaulted Mortgage Loan with a Qualifying Substitute Mortgage Loan…This document seems to state that the mortgage at issue could only be transferred if it were current on the date it was transferred. Accordingly, it appears that this mortgage was inappropriately transferred to the Plaintiff as it was in default at the time of transfer. As such, a question is raised regarding whether the present Plaintiff has standing to bring this foreclosure action.”

HSBC Bank USA, N.A. v. Sene,

34 Misc 3d 1232 (A), 2012 NY Slip Op 50352(U)

(N.Y. Sup. Ct. Kings Co. 2012)

Trust: Ace Securities Corp. Home Equity Loan Trust

2007-HE4

“During the bad faith hearing, two separate notes with attendant assignments were put into evidence by the plaintiff…

This Court emphatically now joins the judicial chorus who have been wary of the paperwork supplied by plaintiffs and their representatives. There is ample reason for Chief Judge’s requirement for an attorney affirmation in residential foreclosure cases. As stated by Chief Judge Jonathan Lippman, “we cannot allow the courts in New York State to stand idly and be party to what we now know is a deeply flawed process, especially when that process involves basic human needs – such as a family home – during this period of economic crisis…

It is clear in this case, without further hearings, that a fraud has been committed upon this Court. Thus, the only remedy that can be utilized by this Court is to stay these proceedings and any mortgage foreclosure until this matter is cleared up to the satisfaction of this Court.”

James v. U.S. Bank, N.A.,

D. Maine, No. 2:09-cv-84-JHR, January 31, 2011

Trust: BAFC 2006-1

Sanctions were imposed because of an Affidavit submitted by GMAC employee and exposed robo-signer Jeffrey Stephan:

“In the case at hand, however, GMAC, the party that submitted the affidavit and the affiant’s employer, was on notice that the conduct at issue here was unacceptable to the courts, which rely on sworn affidavits as admissible evidence in connection with motions for summary judgment. In 2006, an identical jurat signed under identical circumstances resulted in the imposition of sanctions against GMAC in Florida. Affidavit of Thomas A Cox (Docket No. 153) ¶ 4 & Exhs. B-D. GMAC’s assertion that these sanctions applied only “within the State of Florida,” Plaintiff and GMAC Mortgage LLC’s Memorandum in Opposition to Defendant’s Motion for Relief Pursuant to Fed. R. Civ. P. 56(g) (Docket No. 177) at 7, is specious. It would be clear to any lawyer representing GMAC in any court action, including those involved in the Florida action, that a jurat should not be signed under the circumstances involved in that case or here and that such a jurat will never be acceptable to any court. Stephan’s actions in this case strike at the heart of any court’s procedures, are egregious under the circumstances, and must be deemed worthy of sanctions.

LaSalle Bank, N.A. v. Ahearn,

59 A.D.3d 911, 875 N.Y.S. 2d 595 (N.Y. App. Div. 2009)

Trust: Bear Stearns Asset-Backed Securities I, LLC,

Series 2004-FR3

Mortgage Amount: $180,000

“Here, the written assignment submitted by plaintiff was indisputably written subsequent to the commencement of this action and the record contains no other proof demonstrating that there was a physical delivery of the mortgage prior to bringing the foreclosure action (see id.). In fact, the language in the amended complaint indicating that the assignment to plaintiff had not yet occurred would clearly contradict any assertion to the contrary. Accordingly, Supreme Court correctly found that plaintiff did not have standing and the amended complaint must be dismissed, without prejudice.”

LaSalle Bank v. Charleus

Index No. 22733/2007 (January 3, 2008)

(N.Y. Sup. Ct. Kings Co. 2008)

An order of reference was denied by Judge Kurtz where the bank plead a mortgage assignment executed, July 2, 2007, after the suit was commenced June 22, 2007, but with an attempted backdate to June 21, 2007.

LaSalle Bank v. Lamy,

12 Misc.3d 1191(A), 824 N.Y.S.2d 769

“The court thus finds that this purported, undated, indorsement by “allonge” to the note by the original lender in favor of the plaintiff and the December 29, 2005 written assignment of the note and mortgage by MERS to the plaintiff failed to pass ownership of the note and mortgage to the plaintiff prior or subsequent to the commencement of this action. Consequently, the original lender remains the owner of both the note and mortgage since no proper assignment of the either the note or the mortgage was ever made by the original lender/owner to the plaintiff or to the plaintiff’s purported assignee. Under these circumstances, the plaintiff has no cognizable claims for the relief demanded in its complaint.”

LaSalle Bank v. Smalls,

Index No. 28128/2007 (January 3, 2008)

(N.Y. Sup. Ct. Kings Co. 2008)

An order of reference was denied by Judge Kurtz where the bank plead a mortgage assignment executed, September 31, 2007, after the suit was commenced August 31, 2007, but with an attempted backdate to July 30, 2007.

McLean v. JP Morgan Chase Bank, N.A.,

79 So.3d 170 (Fla. 4th DCA 2012)

Trust: Structured Asset Mortgage Investments II, Inc.,

Series 2006-ARS

“Nonetheless, the record evidence is insufficient to demonstrate that Chase had standing to foreclose at the time the lawsuit was filed. The mortgage was assigned to Chase three days after Chase filed the instant foreclosure complaint. More importantly, the original note contained an undated special endorsement in Chase’s favor, and the affidavit filed in support of summary judgment did not state when the endorsement was made to Chase. Furthermore, the affidavit, which was dated after the lawsuit was filed, did not specifically state when Chase became the owner of the note and mortgage, nor did the affidavit indicate that Chase was the owner of the note and mortgage before suit was filed. Therefore, Chase failed to submit any record evidence proving that it had the right to enforce the note on the date the complaint was filed.” (footnotes omitted)

Naranjo v. SBMC Mortgage,

No. 3:11-cv-02229-L-WVG, Dkt. #20

(S.D. Cal. July 24, 2012)

Trust: WMALT 2006-AR4

Mortgage Amount: $825,000

Defendant Trustee’s Motion to Dismiss Denied in Part.

“The vital allegation in this case is the assignment of the loan into

the WAMU Trust was not completed by May 30, 2006 as required by the Trust Agreement. [*10] This allegation gives rise to a plausible inference that the subsequent assignment, substitution, and notice of default and election to sell may also be improper. Defendants wholly fail to address that issue. (See Defs.’ Mot. 3:16-6:2; Defs.’ Reply 2:13-4:4.) This reason alone is sufficient to deny Defendants’ motion with respect to this issue.”

Pino v. Bank of New York,

76 So. 3d 927 (Fla. 4th DCA 2011)

Trust: CWALT 2006-OC8

Mortgage Amount: $162,400

Florida Supreme Court decision pending. The appeal court certified the question to the Florida Supreme Court because “many, many mortgage foreclosures appear tainted with suspect documents.”

“As conveyed by the Fourth District in the decision below, the plaintiffs and now respondents in this Court, the Bank of New York Mellon, et al. (BNY Mellon), commenced an action in the trial court to foreclose a mortgage against the defendant and now petitioner in this Court, Roman Pino. See Pino v. Bank of New York Mellon, 57 So.3d 950, 951 (Fla. 4th DCA 2011). Thereafter, Pino moved for sanctions, alleging that BNY Mellon had filed a fraudulent assignment of mortgage. Id. In response, BNY Mellon filed a notice of voluntary dismissal of the foreclosure action. Id. at 952. Five months later, BNY Mellon refiled an identical action to foreclose the same mortgage. Id. In the original, dismissed action, Pino filed a motion seeking to vacate the voluntary dismissal pursuant to Florida Rule of Civil Procedure 1.540(b)on the grounds of fraud on the court and requesting dismissal of BNY Mellon’s newly filed action as a consequent sanction. Pino, 57 So.3d at 952. The trial court denied Pino’s motion, essentially holding that because the prior action had been voluntarily dismissed, the court lacked jurisdiction, and thus the authority, to consider any relief. Id.” (footnotes omitted)

Richards v. HSBC Bank,

__So.3d__, 2012 WL 2359656 (Fla. 5th DCA 2012)

Trust: PHH 2007-2

Summary judgment for bank reversed on appeal.

“While the assignment reflected that the mortgage had been assigned from Century 21 to HSBC, the allonge to the note reflected that Bishops Gate Residential Mortgage Trust was to be the note’s payee…

Thus the allonge was inconsistent with the assignment and contradicted the allegation in the complaint that HSBC was the holder of the note…

Furthermore, the affidavits filed by HSBC did not explain the relationship between HSBC and Bishops Gate Residential Mortgage Trust, nor otherwise aver facts conclusively showing that HSBC was the holder of the note.

Rigby v. Wells Fargo, N.A.,

__So.3d__, 2012 WL1108428 (Fla. 4th DCA 2012)

Trust: Option One Mortgage Loan Trust 2007-FXD2

Mortgage Amount: $165,600

“The Bank has not shown that it was holder of the note at the time the complaint was filed. The note containing a special endorsement in favor of the bank was not dated. The assignment of mortgage, dated May 22, 2008, indicates that Bank did not acquire the mortgage until the day after the complaint was filed. Finally, neither the affidavit, nor the technical admissions made by the Rigbys, establishes the date on which Bank acquired possession of the note and there is no evidence in the record establishing that an equitable transfer of the mortgage occurred prior to the date the complaint was filed.”

(Summary judgment reversed and remanded.)

Servedio v. U.S. Bank, N.A.,

46 So. 3d 1105 (Fla. 4th DCA 2010)

Trust: Terwin Mortgage Trust 2007-AHL1

Mortgage Amount: $252,000

“The issue presented in this appeal is whether the trial court erred in granting a final summary judgment of foreclosure where appellee failed to file with the court a copy of the original note and mortgage prior to the entry of judgment. Because the absence of the original note created a genuine issue of material fact regarding appellee’s standing to foreclose on the mortgage, summary judgment was not proper. We reverse.”

U.S. Bank v. Alexander,

2012 OK 43

Trust: Credit Suisse First Boston HEAT 2005-4

Mortgage Amount: $63,920

“As previously identified, the dispositive issue is whether or not Appellee had standing at the time Appellee filed their first amended petition. We hold that the issue of standing as well as other material issues of fact remain that must be determined by the trial court. Therefore summary judgment was inappropriate.”

U.S. Bank, N.A. v. Auguste,

Index: 18695-2007 (November 27, 2007)

(N.Y. Sup. Ct. Kings Co. 2007)

Trust: CSMC Mort. Backed PT Certs., Series 2007-1

“In support of plaintiffs application, it submits a purported assignment of the mortgage from Mortgage Electronic Registration Systems, Inc., acting as Nominee for First United, to plaintiff. The purported assignment is dated July 9, 2007, and states in pertinent part “this assignment is effective on or before November 22, 2006.” However, such an attempt to retroactively assign the mortgage is insufficient to establish plaintiff’s ownership interest at the time the action was commenced.”

U.S. Bank, N.A. v. Baber,

280 P.2d 956 (2012 OK 55)

Trust: Security National Mortgage Loan Trust 2006-1

“Being a person entitled to enforce the note is an essential requirement to initiate a foreclosure lawsuit. In the present case, there is a question of fact as to when Appellee became a holder, and thus, a person entitled to enforce the note. Therefore, summary judgment is not appropriate. If Deutsche Bank became a person entitled to enforce the note as either a holder or nonholder in possession who has the rights of a holder after the foreclosure action was filed, then the case may be dismissed without prejudice and the action may be re-filed in the name of the proper party. We reverse the granting of summary judgment by the trial court and remand back for further determinations as to when Appellee acquired its interest in the note.”

U.S. Bank, N.A. v. Collymore,

68 AD3d 752 (2009), 890 NYS2d 578

“Contrary to the Bank’s contentions, it failed to demonstrate its prima facie entitlement to judgment as a matter of law because it did not submit sufficient evidence to demonstrate its standing as the lawful holder or assignee of the subject note on the date it commenced this action. The Bank’s evidentiary submissions were insufficient to establish that MERS effectively assigned the subject note to it prior to the commencement of this action…, and the mere assignment of the mortgage without an effective assignment of the underlying note is a nullity…Furthermore, the Bank failed to establish that the note was physically delivered to it prior to the commencement of the action. The affidavit of a vice-president of the Bank submitted in support of summary judgment did not indicate when the note was physically delivered to the Bank, and the version of the note attached to the vice-president’s affidavit contained an undated indorsement in blank by the original lender. Furthermore, the Bank’s reply submissions included a different version of the note and an affidavit from a director of the Residential Funding Corporation which contradicted the affidavit of the Bank’s vice-president in tracing the history of transfers of the mortgage and note to the Bank. In view of the Bank’s incomplete and conflicting evidentiary submissions, an issue of fact remains as to whether it had standing to commence this action.” (cites omitted)

U.S. Bank v. Dellarmo,

94 A.D.3d 746 (2012), 942 N.Y.S.2d 122

Trust: First Franklin Mortgage Loan Trust, 2006-FF2

“However, inasmuch as the complaint does not allege that the note was physically delivered to the plaintiff, and nothing in the plaintiff’s submission in opposition to Dellarmo’s motion could support a finding that such physical delivery occurred, the corrective assignment cannot be given retroactive effect… Moreover, both the unrecorded April 11, 2006, assignment and the recorded corrective assignment indicate only that the mortgage was assigned to the plaintiff. Since an assignment of a mortgage without the underlying debt is a nullity… the plaintiff has failed to demonstrate that it had standing to commence this action…

Accordingly, the Supreme Court should have granted Dellarmo’s motion pursuant to CPLR 3211 (a) to dismiss the complaint insofar as asserted against him for lack of standing.” (cites omitted)

U.S. Bank, N.A. v. Duvall,

Cuyahoga App. No. 94714, 2010-Ohio-6478

Trust: CMLTI 2007-WFHE2

Mortgage Amount: $92,000

“Accordingly, we conclude that plaintiff had no standing to file a foreclosure action against defendants on October 15, 2007, because, at that time, Wells Fargo owned the mortgage. Plaintiff failed in its burden of demonstrating that it was the real party in interest at the time the complaint was filed. Plaintiff’s sole assignment of error is overruled.”

U.S. Bank, N.A. v. Githira,

17 LCR 697 (2009), MISC 08-386385 (Essex Co. Mass. 2009)

Trust: Home Equity Asset Trust, Series 2005-9

Plaintiff U.S. Bank was seeking to remove a cloud on its title to a parcel of land stemming from plaintiff’s exercise of the power of sale contained in the mortgage before it received authority to do so under the provisions of the Servicemembers’ Civil Relief Act. The complaint did not mention any other title defects.

Citing Justice Long’s ruling in Ibanez, Justice Charles W. Trombly, Jr., dismissed plaintiff’s petition to remove the cloud on the title, holding that plaintiff was not even the holder of the mortgage, by record or in fact, on the day of the foreclosure sale. Specifically, the Court found that the foreclosure auction took place and was recorded prior to the execution and recording of an assignment of mortgage that made plaintiff the holder of the mortgage upon which it had foreclosed.

U.S. Bank, N.A. v. Grant,

Index: 11133-2007

(N.Y. Sup. Ct. Kings Co. 2007)

Trust: Asset Backed Securities Corp. Home Equity Loan

Trust, Series OOMC 2006-HE3

“In support of plaintiffs application, it submits a purported assignment of the mortgage from Option One to plaintiff. The purported assignment is dated July 9, 2007, and states in pertinent part “Effective Date: March 28, 2007.” However, such an attempt to retroactively assign the mortgage is insufficient to establish plaintiff’s ownership interest at the time the action was commenced.”

U.S. Bank, N.A. v. Ibanez,

941 N.E. 2d 40, (Mass. 2011)

Trust: Structured Asset Securities Corp. Mortgage PT

Certs., Series 2006-Z

The court in Ibanez rejected application of the “mortgage follows the note” rule, holding that mere possession of properly indorsed negotiable instruments did not give the foreclosing parties authority to conduct a valid non-judicial sale. In other words, one’s status as a party entitled to enforce a note did not satisfy the requirement under state law to be a mortgagee. The court acknowledged that a transferee of a note might have an equitable right to obtain a court order that that the mortgage be transferred to it. However, the potential to assert such a claim did not make the noteholder a “mortgagee.” The Massachusetts statute required that the foreclosing party have an actual assignment of the mortgage when proceeding to sale., and further held that Assignments in Blank assign nothing and that retroactive assignments are not effective even if it was an industry-wide practice.

U.S. Bank, N.A. v. Madero,

80 AD3d 751, 915 N.Y.S. 2d 612

Trust: not identified

Mortgage Amount: $570,000

“Here, the plaintiff failed to demonstrate its prima facie entitlement to judgment as a matter of law because it did not establish that it had standing, as the lawful holder or assignee of the subject note on the date it commenced this action, to commence the action.” (cites omitted)

U.S. Bank, N.A. v. Merino,

16 Misc.3d 209

(N.Y. Sup. Ct. Suffolk Co. 2007)

“First, the assignment from Argent to Ameriquest was executed by Jose Burgos as agent for Argent. On the same date, however, the purported assignment from Ameriquest to the plaintiff was also executed by Mr. Burgos, this time as agent for Ameriquest. In effect, the mortgage was purportedly assigned by Mr. Burgos to Mr. Burgos, and then, in turn, by Mr. Burgos to the plaintiff…The moving papers contain no proof that Mr. Burgos had either entity’s authority to act in a dual agency capacity. Therefore, the court is unable to conclude that the assignments were validly executed, or that the plaintiff had an ownership interest in the subject mortgage at the time of the filing of this action. Since a party has no foundation in law or fact to foreclose upon a mortgage without establishing its legal or equitable interest, the plaintiff’s motion must be denied.”

U.S. Bank, N.A. v. Middlekauff,

Case No. 10 19844, Hillsborough Co. Fla. 2012

Trust: CSFB Mortgage-Backed Trust, Series 2005-9

“First, Plaintiff lacked standing at the inception of this case. Although the Note attached to the Amended Complaint contains an allonge, the undisputed summary judgment evidence before the Court establishes that this allonge was created post-filing. As Plaintiff lacked standing when it filed this lawsuit, dismissal is required.” (cite omitted)

U.S. Bank v. Moore,

2012 OK 32

GSAA Home Equity Trust 2006-6

Mortgage Amount: $282,000

“It is a fundamental precept of the law to expect a foreclosing party to actually be in possession of its claimed interest in the Note, and to have the proper supporting documentation in hand when filing suit, showing the history of the Note, so that the defendant is duly apprised of the rights of the plaintiff. This is accomplished by showing the party is a holder of the instrument or a nonholder in possession of the instrument who has the rights of a holder, or a person not in possession of the instrument who is entitled to enforce the instrument…”

U.S. Bank, N.A. v. Roundtree,

Index: 009148/2007

(N.Y. Sup. Ct. Suffolk Co. 2007)

Trust: MASTR Alternative Loan Trust 2006-HE1

“Since MERS, Inc. had no ownership interest in said note, it could not assign it to the plaintiff and any assignment purportedly transferring the ownership interest from Fremont Investment and Loan to the plaintiff by a MERS, Inc. assignment of said note is a nullity.” (cites omitted)

… In view of the foregoing, the instant motion (#001) is denied as it is apparent from the documentary submissions of the plaintiff that it was not the owner of the note at the time of the commencement of this action.”

U.S. Bank, N.A. v. Villaruel,

Index: 25277/2008

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: SG Mort. Sec. AB Certs., Series 2006-FRE2

“The purported assignment is dated August 3, 2007 and states in pertinent part “[t]his assignment is effective as of the 10th day of June, 2007.” However, such an attempt to retroactively assign the mortgage is insufficient to establish plaintiff’s ownership interest at the time the action was commenced. Plaintiff’s attempt to foreclose upon a mortgage in which it had no “legal or equitable interest was without foundation in law or fact…” (cites omitted)

Verizzo v. Bank of New York,

28 So.3d 976 (Fla. 2d DCA 2010)

Trust: Novastar Mortgage Funding Trust, Series 2006-3

“In addition to the procedural error of the late service and filing of the summary judgment evidence, those documents reflect that at least one genuine issue of material fact exists. The promissory note shows that Novastar endorsed the note to “JPMorgan Chase Bank, as Trustee.” Nothing in the record reflects assignment or endorsement of the note by JPMorgan Chase Bank to the Bank of New York or MERS. Thus, there is a genuine issue of material fact as to whether the Bank of New York owns and holds the note and has standing to foreclose the mortgage.”

(Summary judgment reversed and remanded.)

Wells Fargo Bank, N.A. v. Ford,

418 N.J. Super. 592 (App. Div. 2011)

Mortgage Amount: $403,750

“For these reasons, the summary judgment granted to Wells Fargo must be reversed and the case remanded to the trial court because Wells Fargo did not establish its standing to pursue this foreclosure action by competent evidence. On the remand, defendant may conduct appropriate discovery, including taking the deposition of Baxley and the person who purported to assign the mortgage and note to Wells Fargo on behalf of Argent.”

Wells Fargo Bank, N.A. v. Hampton,

Index: 25957/2007 (January 3, 2008)

(N.Y. Sup. Ct. Kings Co. 2008)

Trust: Option One Mort. Loan Trust 2007-1

“The purported assignment is dated August 1, 2007 and states in pertinent part “[e]ffective as of June 10, 2007.” However, such an attempt to retroactively assign the mortgage is insufficient to establish plaintiff’s ownership interest at the time the action was commenced. Plaintiff’s attempt to foreclose upon a mortgage in which it had no “legal or equitable interest was without foundation in law or fact…” (cites omitted)

Wells Fargo Bank, N.A. v. Heath,

212 OK 54

Trust: Option One Mortgage Loan Trust 2005-4