This post is intended to offer a general introduction to, and overview of, the course of a “typical” civil lawsuit for homeowners wishing to fight their foreclosure in other to save their homes. Because of the vast array of actions that may be pursued in Florida courts, an exhaustive discussion of the rights, remedies, and procedures available is beyond the scope of this post.

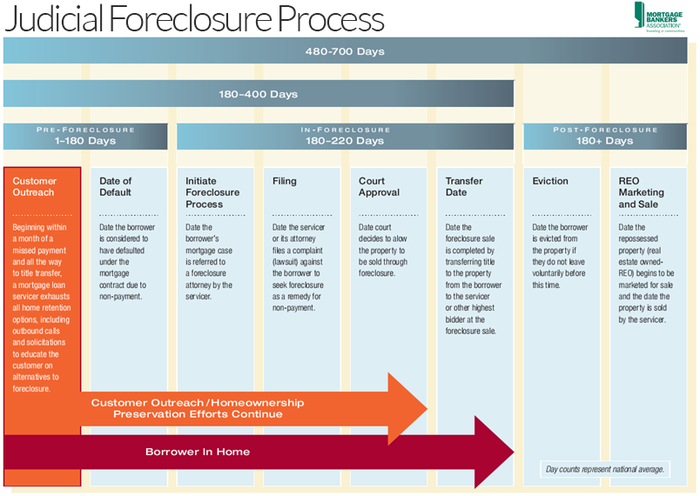

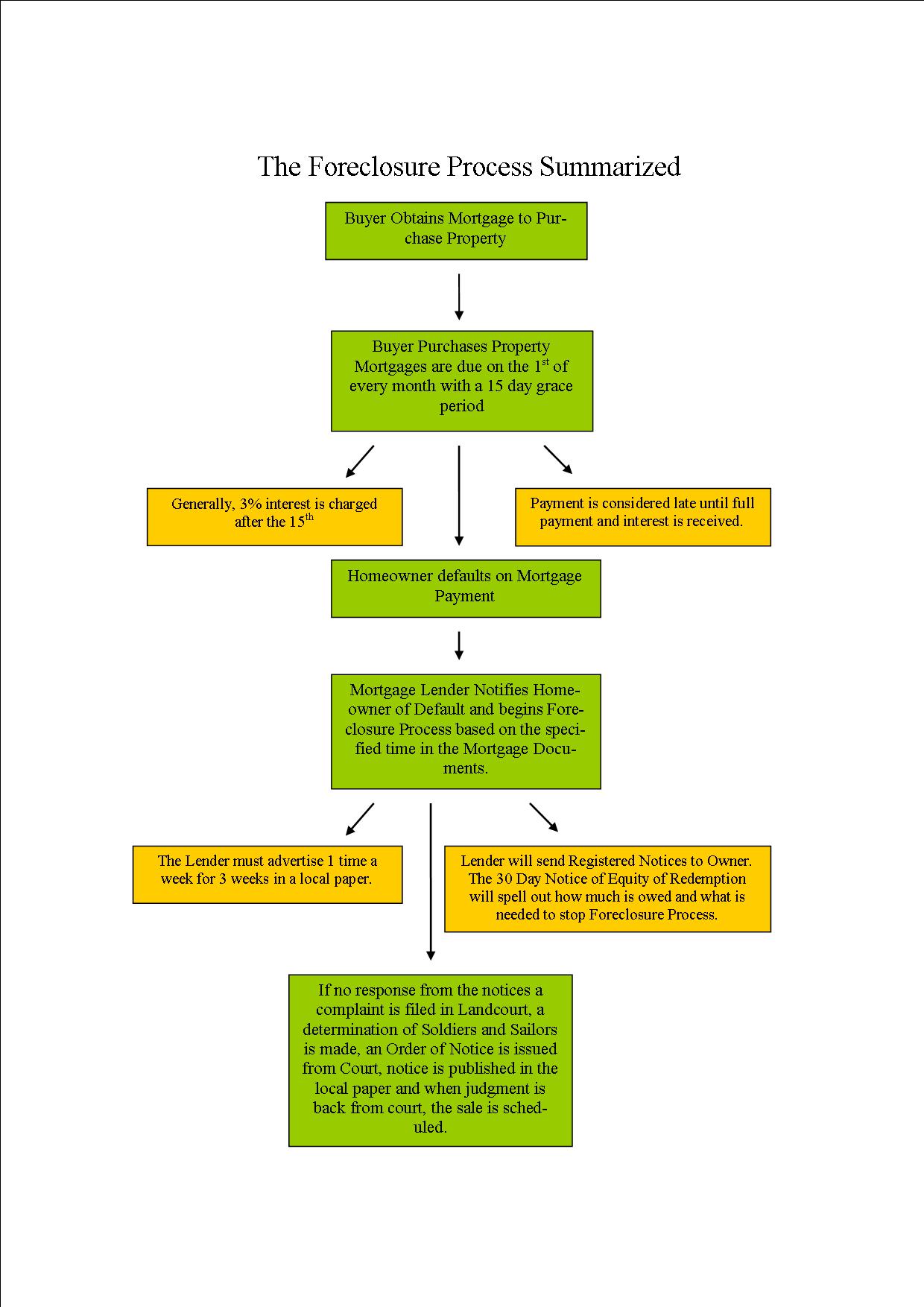

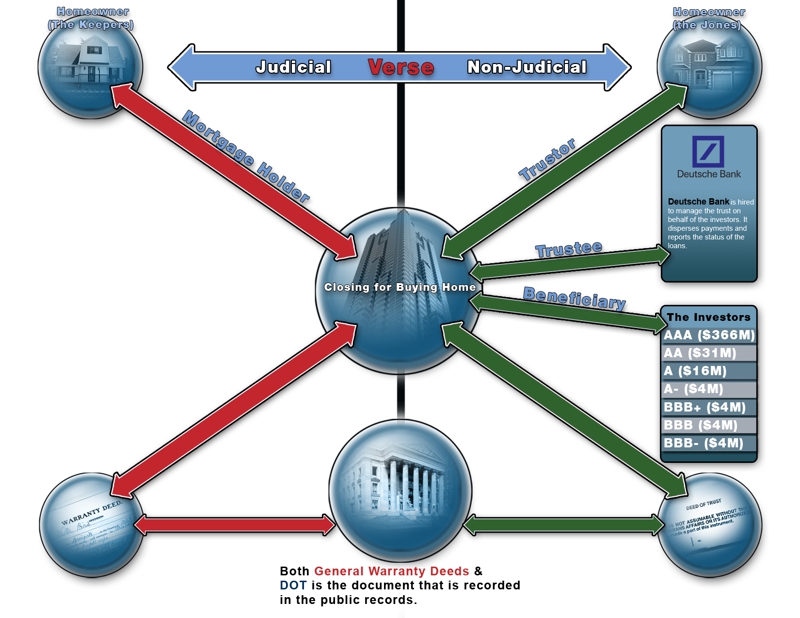

Moreover, this post will focus mainly on the pretrial proceedings, which tend to be more “mysterious” and less publicized than the actual trial. Indeed, pretrial proceedings can be a valuable way of savings your home as many banks and lenders who were in the business of illegal wrongful foreclosure with fraudulently manufactured sets of mortgage documents never take homeowners serious until it gets to that stage. The reason why they take a homeowner serious from that point on is that Banks and lenders will then start making major expenses on legal fees to attorneys retained to respond to the wrongful foreclosure complaints filed by homeowners. With an average wrongful foreclosure litigation lasting between 2 to 5 years, and many homeowners living in their homes mortgage free throughout the litigation period without making a dime in mortgage payments, most smart Lenders and Banks try to cut their loses by quickly modifying mortgage loans with terms most favorable to homeowners in order for homeowners to remain in their rightfully owned dream homes. This fit would not have been accomplished by simply asking the banks to modify a mortgage loan as most loans have been securitized to investors. Lenders and banks from that point on serves only as “servicers” (Not Owners) to the securitized investment trusts From that point after the securitization, they are no longer owners of the mortgage loans, but simply servicers of the trust, unless they later repurchase it after default. They may try to trick homeowners into thinking that they still own their mortgage loans, absolutely not! That’s why they are giving homeowners run around in order to foreclose and steal the home right behind your nose. Folks! they can’t modify mortgage loans for the simple fact that “they cannot modify what they don’t own” period! There are thousands of investors that own the mortgage pools. Mortgage pools are controlled by PSA (Pooling and Servicing Agreement) and they must obtain consent authorizations from all investors (Real Owners), in order to modify any loans in the securitized pools that is why it is nearly impossible to modify most loans unless you take them to Court to prove their ownership, which they cannot do. Then and only then will the Lenders and Banks get those consent from investors as investors do not want to lose assets and in most times the loans will simply be repurchased from the trust by your lender after default before modification. Once repurchased, your loan is ‘get this’, “no longer a secured debt” but an unsecured debt and your “home” is no longer used as a collateral to your mortgage loan debt. Your mortgage loan may also have been paid off by forced place insurance your lender placed on your loan when you took out your loan, as that is taken out to cover their loses in the event of your default on the mortgage loan. That this why they are charging you the forced placed insurance premium when you took out your mortgage loan, in order to collect large sums of money that reduces your mortgage debt and in most cases, “pays off your entire mortgage loan” when you default. But they will still try to foreclose on you as if your loan is still a secured debt which it is not. They perpetrate those fraud due to your ignorance. That’s of course if you keep quite and let them steal your home right under your nose.

While many homeowners are familiar with the general procedures applicable in criminal cases, they may be less familiar with civil proceedings. For example, unlike criminal defendants, civil litigants enjoy no constitutional speedy trial rights. As a result, civil proceedings may seem unduly lengthy, particularly in counties where the court dockets are especially congested. Courts try to speed up the process and encourage extra-judicial resolution of disputed claims, for example, through court-annexed mediation or arbitration.

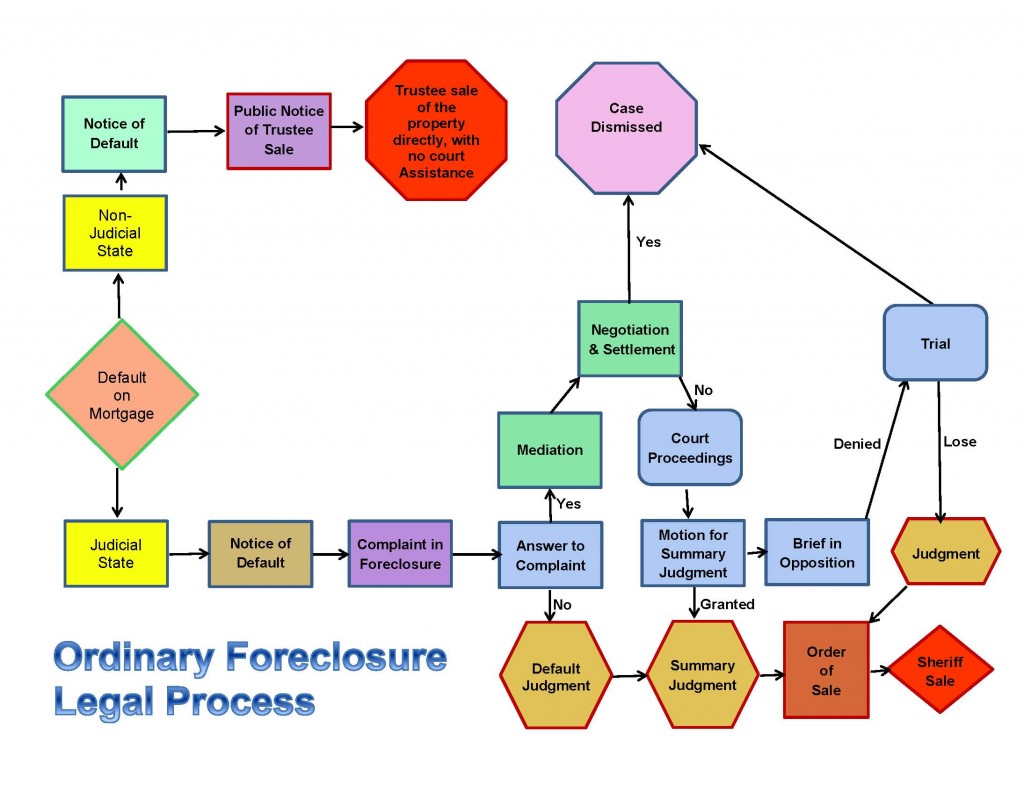

I. The Pleadings

A. The Complaint

B. Answer

C. Responsive Motions

D. Counterclaims

E. Crossclaims and Third-Party Claims

F. Amendment

II. Pretrial Procedure

A. Discovery

B. Discovery Methods

C. Protective Orders

D. Sanctions

III. Dismissal

A. Voluntary Dismissal

B. Involuntary Dismissal

C. Summary Judgment

IV. Non-Judicial Methods of Resolution

A. Mediation

B. Arbitration

C. Offers of Judgment

V. Trial

A. Demand for Jury

B. Jury Selection

C. Opening Statements

D. Motion for Directed Verdict

E. Closing Argument

F. Jury Instructions

G. Verdict

VI. Conclusion

————————–

I. The Pleadings.

The term “pleadings” often is used synonymously (and incorrectly) to refer to any documents filed with the court. However, this term has a more limited and technical meaning. The “pleadings” in a lawsuit are simply those filings that set forth either (a) the complaining party’s allegations and causes of action; or (b) the defending party’s responses to those allegations along with any defenses or causes of action the defending party may assert. This becomes significant only when the Florida Rules of Civil Procedure distinguish between “pleadings” and other documents. For example, a motion to dismiss for failure to state a cause of action is directed solely to the “pleadings” and the court may not consider any other filings, such as exhibits, deposition testimony, interrogatory answers, etc.

A. The Complaint.

A civil action is commenced by filing a complaint or petition. Fla. R. Civ. P. 1.050. This initial pleading filed by the complaining party generally consists of factual allegations, a description of the legal claims based on those allegations, and a request for relief. Fla. R. Civ. P. 1.110(b). Some pleadings are subject to special rules. For example, in actions alleging injury or death arising out of medical malpractice, the pleadings are required to include a certificate that counsel has conducted “a reasonable investigation as permitted by the circumstances to determine that there are grounds for a good faith belief that there has been negligence in the care or treatment of the claimant.” Fla. Stat. Sec. 766.104(1) (2003). “Good faith” may be demonstrated by a written expert opinion that there is evidence of medical negligence. Id. Failure to comply with this section may subject the party to an award of fees and costs. Id. These special pleading rules are in addition to the pre-suit notice requirements applicable to medical malpractice claims. See Fla. Stat. Sec. 766.106 (2003). A lawsuit may involve one defendant, multiple defendants, or even a class of defendants. The procedures and requirements for certifying a class of plaintiffs or defendants are found in Fla. R. Civ. P. 1.220. Similarly, the lawsuit may involve multiple plaintiffs or a class of plaintiffs.

A complaint may assert more than one count. It may state different causes of action, even if they are inconsistent. This common practice is called pleading “in the alternative.” Sometimes the conduct complained about may support more than one cause of action, depending on what discovery reveals. For example, Adam contracts to sell a piece of commercial real estate to Bob. Adam decides to accept a better offer from Charles. Bob brings a lawsuit against Adam after Adam reneges on their agreement. Bob may seek monetary damages because he will have to incur additional expenses in finding another suitable property. However, Bob also may sue in the alternative, for “specific performance,” which simply means that the original contract between Bob and Adam would be enforced and Adam would be required to sell the property to Bob, instead of paying Bob money damages.

Therefore, a party often does not have to choose initially which theory it will proceed on; however, the party ultimately can recover only once. Therefore, Bob cannot have both remedies and will have to choose which one he wants.

A party also may plead claims that are inconsistent with each other. As one court has noted, this is because “the pleadings in a cause are merely a tentative outline of the position which the pleader takes before the case is fully developed on the facts.” Hines v. Trager Constr. Co., 188 So. 2d 826, 831 (Fla. 1st DCA), cert. denied, 194 So. 2d 618 (Fla. 1966). This rule applies equally to defendants. Therefore, a defendant may raise defenses that are inconsistent with each other.

The relief most commonly sought is money damages. Compensatory damages are intended to compensate the injured party for its loss. Punitive or exemplary damages are awarded beyond the actual loss and are intended to punish the wrongdoer and to deter similar conduct by others. The availability of punitive damages is limited by statute and court rule. See Fla. Stat. Sec. 768.72 (2003). This statute prevents a party from even including a claim for punitive damages in the complaint until that party has presented record evidence sufficient to support a jury verdict for punitive damages. This is important because the party seeking punitive damage is not entitled to the discovery of information concerning the other party’s financial net worth until the court is satisfied that a triable claim for punitive damages has been established. Id. In 2003, these requirements were incorporated into Fla. R. Civ. P. 1.190(f).

A party also may seek injunctive relief, i.e., an order by the court directing a party to do some act (positive) or to refrain from doing some act (negative). Once such an order is entered by a court, noncompliance with that order may be punishable as contempt of court.

One form of injunctive relief frequently requested is “specific performance,” which is essentially a direction to a party to perform its contract. Specific performance may be requested in land sales contracts and non-compete agreements. However, this remedy is not available to enforce certain types of contracts, such as personal service contracts.

A party also may seek declaratory relief. The trial courts have jurisdiction “to declare rights, status, and other equitable or legal relations whether or not further relief is or could be claimed.” Fla. Stat. Sec. 86.011 (2003). This may include the interpretation and declaration of rights under “a statute, regulation, municipal ordinance, contract, deed, will, franchise, or other article, memorandum, or instrument in writing.” Fla. Stat. Sec. 86.021 (2003). The declaration may be affirmative or negative and “has the force and effect of a final judgment.” Fla. Stat. Sec. 86.011 (2003). For example, declaratory judgment proceedings frequently are initiated by insurance companies seeking a determination of their obligation to defend against another action.

B. Answer.

After being served with the initial pleading, the defendant (or respondent) must respond to it. A defendant has a couple of options at this stage.

Typically the defendant files an answer, which responds to each allegation of the complaint and which may set forth one or more defenses. Fla. R. Civ. P. 1.110(c). Under the rules of civil procedure, “affirmative defenses” must be asserted in a responsive pleading or motion to dismiss or they will be waived. Fla. R. Civ. P. 1.110(d). Affirmative defenses are those defenses that “avoid” rather than deny. For example, the statute of limitations is an affirmative defense. By raising this defense, the defendant asserts that even if the defendant committed all of the horrible acts alleged by the plaintiff, the plaintiff has no cause of action because the action was not filed in a timely fashion. In that respect the claim is “avoided,” rather than denied.

C. Responsive Motions.

In lieu of, or in addition to, filing an answer, the defendant may move to challenge the legal sufficiency of the claims raised by the plaintiff. Fla. R. Civ. P. 1.140. These rules apply equally to counterclaims, crossclaims, and third-party claims. This motion is not a “pleading.” The defendant may argue that the complaint “fails to state a claim,” that is, even assuming that the facts alleged in the complaint are true, the law does not recognize a cause of action. Fla. R. Civ. P. 1.140(b)(6). For example, a store patron sues the grocery store for damages after he is assaulted by a third person in the vacant lot next door. The grocery store will move to dismiss, claiming that the store patron has failed to state a cause of action because it has no duty to protect customers off the premises. An out-of-state defendant might argue that the court lacks “personal jurisdiction” over him or her Fla. R. Civ. P. 1.140(b)(2). because he or she lacks sufficient “contacts” with the state, such as an office or business transactions in the state. This is based on the federal due process clause. Before a court may exercise personal jurisdiction over a nonresident defendant, that defendant must possess “certain minimum contacts with the state” so that “maintenance of the suit does not offend ‘traditional notions of fair play and substantial justice’.” Walt Disney Co. v. Nelson, 677 So. 2d 400, 402 (Fla. 5th DCA 1996) (quoting International Shoe Co. v. Washington, 326 U.S. 310, 316 (1945)).

Other defenses that might be raised at this stage include failure to join an indispensable party, Fla. R. Civ. P. 1.140(b)(7). lack of subject matter jurisdiction, Fla. R. Civ. P. 1.140(b)(1). Subject matter jurisdiction refers to the court’s authority or competence to preside over certain matters. For example, by statute, circuit courts lack subject matter jurisdiction to hear matters involving amounts less than $15,000.00. The subject matter for such actions is vested in the county courts. See Fla. Stat. Sec. 34.01(1)(c) (2003). improper venue, Fla. R. Civ. P. 1.140(b)(3). Venue is governed by Fla. Stat. Ch. 47 (2003), except where the Legislature has provided for special venue rules. See, e.g., Fla. Stat. Sec. 770.05 (2003) (limiting choice of venue in actions involving “libel or slander, invasion of privacy, or any other tort founded upon any single publication, exhibition, or utterance”). and insufficiency of process Fla. R. Civ. P. 1.140(b)(4). “Insufficiency of process” refers to the actual document which is served. To determine if the process is adequate, one should examine it to determine that it is signed by a clerk of court or the clerk’s deputy, it bears the clerk’s seal, a correct caption, the defendant’s correct name, the name of the appropriate state, the return date, the name and address of the party or lawyer causing process to be issued, and the name of any defendant organization. If it is not a summons, it should comply with the statute or rule that authorizes its issuance. See H.

Trawick, Florida Practice & Procedure Sec. 8-22, at 170-72 (1999). or service of process. Fla. R. Civ. P. 1.140(b)(5). A defect in the “service of process” claims that the defendant was not served appropriately: for example, he or she was not served personally, when required. Service of process is governed by Fla. R. Civ. P. 1.070 and by Fla. Stat. Chs. 48, 49 (2003). Certain defenses are waived if not raised either by an answer (or other responsive pleading) or by motion to dismiss, such as personal jurisdiction, improper venue, and insufficiency of process or service of process. Fla. R. Civ. P. 1.140(h)(1).

A defendant also may move for “a more definite statement” if the pleading is so vague or ambiguous that the defendant cannot frame a sufficient response to it Fla. R. Civ. P. 1.140(e). or it may move to “strike” portions as “redundant, immaterial, impertinent or scandalous.” Fla. R. Civ. P. 1.140(f).

D. Counterclaims.

In addition to its responsive pleading, a defendant may file a counterclaim, which operates like a complaint, except that the defendant is now the counterclaim plaintiff. Fla. R. Civ. P. 1.170. Thus, a counterclaim sets out factual allegations, legal claims, and a request for relief, just like a complaint. Id. A counterclaim requires a response by the “counterclaim defendant,” who was the plaintiff in the initial complaint. See Fla. R. Civ. P. 1.100(a) and 1.110(c).

Counterclaims may be “permissive” or “compulsory.” Fla. R. Civ. P. 1.170(a), (b). A counterclaim is “compulsory” and, therefore, must be raised in he current action if it “arises out of the transaction or occurrence that is the subject matter of the opposing party’s claim and does not require for its adjudication the presence of third parties over whom the court cannot acquire jurisdiction.” Fla. R. Civ. P. 1.170(a). On the other hand, a counterclaim is “permissive” if it does not arise out of the transaction or occurrence that is the subject matter of the opposing party’s claim. Fla. R. Civ. P. 1.170(b). This designation determines whether the counterclaim must be raised at this time or whether the defendant/counterclaim plaintiff can bring a separate action on the counterclaim. Fla. R. Civ. P. 1.170(a), (b).

E. Crossclaims and Third-Party Claims.

A defendant may file a crossclaim against another defendant Fla. R. Civ. P. 1.170(g). or may file a third-party complaint against a nonparty. Fla. R. Civ. P. 1.170(h). Crossclaims and third-party claims include factual allegations, legal claims, and requests for relief. They also require a response by the crossclaim or third-party defendants. Fla. R. Civ. P. 1.100(a). In practice, the pleadings can become quite complicated because of the number of possible claims which may be asserted. For example, a crossclaim defendant can assert a counterclaim against the crossclaim plaintiff and can assert a third-party claim against other nonparties. Multiple plaintiffs who are subject to a counterclaim can assert cross-claims against each other or third-party claims against other nonparties. There may be fourth party complaints. Understanding the availability of crossclaims, counterclaims and third-party claims by various parties aids in comprehension when one is faced with a lengthy caption identifying one party as a defendant, a counterclaim plaintiff, a crossclaim defendant, and a third-party plaintiff, all at the same time.

F. Amendment.

A party may amend the pleading once as a matter of right if there has been no responsive pleading. Otherwise, leave of court or written consent of the other side is required. Fla. R. Civ. P. 1.190(a). Leave of court is “given freely when justice so requires.” Id. Frequently a party will amend the pleading to cure any deficiencies addressed by a motion to dismiss. Amendments may be allowed even after trial under certain circumstances. Fla. R. Civ. P. 1.190(b).

II. Pretrial Procedure.

After responsive pleadings or motions are due, the court may schedule a case management conference to try to expedite and streamline litigation, for example, by scheduling service of papers, coordinating complex litigation, addressing discovery issues, pretrial motions and settlement issues, requiring the parties to file stipulations, etc. Fla. R. Civ. P. 1.200(a).

Later, the court may schedule a pretrial conference to address simplification of issues, amendments, admissions by one party, experts, etc. The failure of a party or its attorney to cooperate in these conferences may result in sanctions. Fla. R. Civ. P. 1.200(b), (c); Fla. Stat. Sec. 768.75(1) (2003).

A. Discovery.

Discovery occupies a large part of most civil lawsuits because Florida courts do not favor trial “by ambush.” Therefore, the rules of civil procedure encourage, indeed mandate, complete discovery. In practice, however, discovery disputes occupy a large amount of attorney and judge time.

Generally, discovery is allowed of “any matter, not privileged, that is relevant to the subject matter of the pending action.” Fla. R. Civ. P. 1.280(b)(1). In this context, “relevance” has a very broad meaning. Information is discoverable if it “appears reasonably calculated to lead to the discovery of admissible evidence.” Id.

The goals of discovery are several. Each party desires to know what the other party intends to present at trial so as to avoid any nasty surprises. Each party also seeks to obtain evidence either to support its claims and/or defenses or rebut the opposing party’s claims and/or defenses, whether directly or through impeachment. Discovery permits a party to obtain information concerning what documents the other side intends to introduce, what that party’s experts and other witnesses will say and how that party intends to prove its claims and/or defenses. In cases in which punitive damages legitimately have been sought, the plaintiff may obtain financial worth information from the alleged wrongdoer. However, keep in mind that punitive damages only may be requested with prior permission of the court. See Fla. Stat. Sec. 768.72 (2003).

While discovery is very broad, it is not without limitation. For example, the other side generally cannot discover privileged information. Fla. R. Civ. P. 1.280(b)(1). Examples of evidentiary privileges recognized by statute are: journalist’s privilege, Fla. Stat. Sec. 90.5015 (2003); attorney-client communications, Fla. Stat. Sec. 90.502 (2003); psychotherapist-patient communications, Fla. Stat. Sec. 90.503 (2003); sexual assault counselor-victim communications, Fla. Stat. Sec. 90.5035 (2003); domestic violence advocate-victim communications, Fla. Stat. Sec. 90.5036 (2003); husband-wife communications, Fla. Stat. Sec. 90.504 (2003); communications to clergy, Fla. Stat. Sec. 90.505 (2003); accountant-client communications, Fla. Stat. Sec. 90.5055 (2003); and trade secrets, Fla. Stat. Sec. 90.506 (2003). The rules also restrict a party’s ability to obtain documents and tangible things prepared “in anticipation of litigation” by the other side. Fla. R. Civ. P. 1.280(b)(3). This is also known as the “work-product” privilege. The rules severely limit a party’s ability to discover information concerning experts who have been retained by the other side in anticipation of litigation but who are not expected to testify at trial. Fla. R. Civ. P. 1.280(b)(4)(B).

B. Discovery Methods.

There are several mechanisms for obtaining discovery. To a large extent, the type of discovery method employed and its timing depend on the information desired and the particular style of the legal practitioner.

1. Depositions.

A “deposition” is an oral examination of a person under oath that is recorded by a stenographer and may be videotaped or audiotaped. Fla. R. Civ. P. 1.310. A party deponent may be required to produce documents during the examination. Fla. R. Civ. P. 1.310(b)(5). Depositions of parties may be used by the other side for any purpose. Fla. R. Civ. P. 1.330(a)(2). Depositions may be taken by telephone. Fla. R. Civ. P. 1.310(b)(7). Depositions frequently are used to impeach subsequent testimony. Sometimes, depositions may be taken prior to the filing of a civil action or during appeal to preserve testimony. Fla. R. Civ. P. 1.290. Depositions may or may not be transcribed, depending upon the wishes of the parties. Depositions also may be conducted on written questions. See Fla. R. Civ. P. 1.320. This method is not used frequently.

2. Interrogatories.

“Interrogatories,” another common discovery method, are written questions that are served on a party Although the rules allow for any person to be deposed, interrogatories and requests for admission may be directed only to parties. See Fla. R. Civ. P. 1.340(a) (“a party may serve upon any other party written interrogatories”) and 1.370(a) (“[A] party may serve upon any other party a written request for the admission of the truth of any matters within the scope of rule 1.280(b)”). and that require written responses within thirty (30) days. Fla. R. Civ. P. 1.340(a). The rules limit the number of questions to thirty (30) without court approval. Id. Form interrogatories pre-approved by the Florida Supreme Court must be used if applicable. Id. Interrogatories must be answered separately, fully, in writing, and under oath unless objections are made. Id. Like deposition testimony, interrogatory answers frequently are used to impeach subsequent testimony.

A party may produce records in lieu of answering an interrogatory if the answer may be derived from those records and if it is equally burdensome for the party to determine the answer as it is for the party seeking the information. Fla. R. Civ. P. 1.340(c).

3. Production of Documents and Things by Parties.

A party may be required to produce documents or other tangible things for inspection and/or copying by the other side. Fla. R. Civ. P. 1.350(a). “Documents” are defined broadly to include writings, drawings, graphs, charts, photographs, phono-records and other “data compilations” from which information may be obtained or translated. See Fla. R. Civ. P. 1.350. The party seeking the information may test and sample the tangible items. Fla. R. Civ. P. 1.350(a)(2). A party may request to enter upon designated land or property to inspect some object or operation. Fla. R. Civ. P. 1.350(a)(3).

4. Production of Documents and Things by Nonparties.

A party also may obtain documents from nonparties by issuing a subpoena directing production of documents or things without deposition. See Fla. R. Civ. P. 1.351(a). Other parties must be notified at least ten (10) days before the subpoena issues so that they may object. Fla. R. Civ. P. 1.351(b). If another party objects, this method of nonparty discovery becomes unavailable. Fla. R. Civ. P. 1.351(c). If there is no objection, the nonparty may comply with the subpoena by providing copies of the documents or things sought. Fla. R. Civ. P. 1.351(e).

5. Mental and Physical Examinations.

In certain circumstances, a party may request that a qualified expert conduct a physical or mental examination of a party, or a person in that party’s control or custody. Fla. R. Civ. P. 1.360(a). This discovery method is utilized most often in personal injury cases and otherwise when a person’s physical or mental condition is in controversy. The party requesting the examination must demonstrate good cause. Fla. R. Civ. P. 1.360(a)(2).

6. Request for Admissions.

An important, but often under-utilized, form of discovery is the “request for admissions.” Fla. R. Civ. P. 1.370. One party serves upon another party a written request that the party admit to the truth of certain matters, including statements or opinions of fact or the application of law to fact, or the genuineness of documents. Fla. R. Civ. P. 1.370(a). If the other side fails to respond or object within thirty (30) days, the facts are considered admitted, which means that they are conclusively established. Fla. R. Civ. P. 1.370(b). The requesting party also may move to determine the sufficiency of the responses. Fla. R. Civ. P. 1.370(a). If the court decides that a response does not comply with the rule, the matter may be deemed admitted or an amended answer required. Id. If a party fails to admit a matter and the other side later proves that matter, the party may have to pay the costs incurred by the other side in making that proof. Id. Recently, the Florida Supreme Court revised the rules of civil procedure to limit the number of requests for admissions to thirty (30).Fla. R. Civ. P. 1.370(a).

C. Protective Orders.

At any time, a party or nonparty from whom discovery is sought may ask the court to enter a protective order to protect that person from “annoyance, embarrassment, oppression, or undue burden or expense.” Fla. R. Civ. P. 1.280(c). Such a protective order may prohibit discovery, limit its scope, or effectuate other protective measures. Id.

D. Sanctions.

A party who is dissatisfied with the other side’s cooperation in discovery may seek an order compelling discovery. Fla. R. Civ. P. 1.380(a). If a motion to compel is granted, the opposing party shall pay the moving party’s expenses incurred in obtaining the order, which may include attorney’s fees, unless the opposition to the motion was justified or other circumstances make an award of expenses unjust. Fla. R. Civ. P. 1.380(a)(4). Similarly, if the motion is denied, the moving party shall pay the nonmoving party’s expenses unless the motion was substantially justified or other circumstances make an award of expenses unjust. Id.

If the court orders discovery, failure to obey that order may be punishable as contempt. Fla. R. Civ. P. 1.380(b). The court has many available sanctions for discovery violations, particularly when the recalcitrant person is a party. Certain matters may be deemed established or a party may be prevented from opposing or supporting claims or defenses or from introducing evidence. Fla. R. Civ. P. 1.380(b)(2). The court may strike pleadings, dismiss the action, or enter a default judgment. Id. However, the failure to submit to a physical or mental examination is not punishable by contempt. Fla. R. Civ. P. 1.380(b)(2)(E).

III. Dismissal.

Frequently, civil actions are dismissed before a trial on the merits of the underlying claims. In addition to settlement, dismissal of a civil action may come about under a number of circumstances.

A. Voluntary Dismissal.

A party’s ability to dismiss its own action is limited by the rules of civil procedure. Fla. R. Civ. P. 1.420. The dismissal rules also apply to counterclaims, crossclaims, and third-party claims. A party may dismiss its lawsuit voluntarily without a court order prior to trial, as long as no motion for summary judgment has been heard or one has been denied and the case has not been submitted to the fact-finder. Fla. R. Civ. P. 1.420(a)(1)(A). An action may be dismissed by stipulation of the parties. Fla. R. Civ. P. 1.420(a)(1)(B). If the plaintiff previously has dismissed a similar case, this second dismissal will operate as an adjudication on the merits and the plaintiff will not be permitted to refile the action. Fla. R. Civ. P. 1.420(a)(1). Otherwise, the plaintiff may be able to refile the action. However, the plaintiff may be required to pay costs before bringing a similar action against the same party. Fla. R. Civ. P. 1.420(d).

B. Involuntary Dismissal.

The court may enter an order of dismissal as a sanction for failure to comply with court rules or orders. Fla. R. Civ. P. 1.420(b). In evaluating whether the compliance merits this drastic sanction, the court considers the intent of the noncompliant party, the existence of previous sanctions, the involvement of the client, the degree of prejudice to the other side, and any justification for noncompliance. See H. Trawick, Florida Practice & Procedure Sec. 21-5, at 335-37 (1999).

If a case is tried to the court (i.e., without a jury), a party may seek involuntary dismissal if the other side, after completing its presentation of evidence, has failed to show a right to relief. Fla. R. Civ. P. 1.420(b).

Unless the order states that the dismissal is without prejudice, an involuntary dismissal under this rule is an adjudication on the merits and precludes the plaintiff from refiling the action. See, e.g., Drady v. Hillsborough County Aviation Auth., 193 So. 2d 201 (Fla. 2d DCA 1967), cert. denied, 210 So. 2d 223 (Fla. 1968).

An action shall be dismissed by the court for failure to prosecute if there has been no record activity for one year unless the court has stayed the action or a party shows good cause prior to the hearing. Fla. R. Civ. P. 1.420(e). In practice, this rule is strictly enforced.

C. Summary Judgment.

After the lawsuit has been filed, either party may move for summary judgment, subject to certain time restrictions. Fla. R. Civ. P. 1.510. Unlike a motion to dismiss, a motion for summary judgment does more than challenge the legal sufficiency of the complaint. Of course, a summary judgment motion may be directed to a counterclaim, crossclaim, or third-party claim in the same manner. In moving for a summary judgment, one argues that the opposing party cannot present evidence that would be sufficient to demonstrate a “genuine issue as to any material fact” and that the moving party is entitled to judgment as a matter of law. Fla. R. Civ. P. 1.510(c). Orders granting summary judgment are scrutinized closely on appeal.

The motion for summary judgment may be supported or opposed by competent affidavits made on personal knowledge that set forth admissible facts. Fla. R. Civ. P. 1.510(a), (b), (e). The parties also may rely upon depositions and answers to interrogatories. Fla. R. Civ. P. 1.510(e). However, in evaluating a motion for summary judgment, a trial judge may not weigh evidence or assess credibility. If the material facts are in dispute, summary judgment may not be entered and the litigation continues.

IV. Non-Judicial Methods of Resolution.

There are several ways in which a case may be resolved by the parties before trial, with the assistance of “alternative dispute resolution” techniques.

A. Mediation.

Mediation is “a process whereby a neutral third person called a mediator acts to encourage and facilitate the resolution of a dispute between two or more parties. It is an informal and nonadversarial process with the objective of helping the disputing parties reach a mutually acceptable and voluntary agreement.” Fla. Stat. Sec. 44.1011(2) (2003). The parties also may stipulate to mediation. Fla. R. Civ. P. 1.710(b). Mediation does not suspend the discovery process. Fla. R. Civ. P. 1.710(c).

Some civil actions are never ordered to mediation, including bond estreatures, habeas corpus and extraordinary writs, bond validations, criminal or civil contempt proceedings, or any other matters specified by the chief judge of that court. Fla. R. Civ. P. 1.710(b).

The mediator may be chosen by the parties or may be appointed by the court. The chief judge maintains a list of mediators who have been certified by the Florida Supreme Court. Fla. Stat. Sec. 44.102(5) (2003). When possible, qualified individuals who have volunteered their time to serve as mediators shall be appointed. Fla. Stat. Sec. 44.102(5)(a) (2003). Often parties agree on a particular mediator in order to select someone with specialized knowledge or expertise in the area under consideration.

Parties who fail to appear at mediation without good cause are subject to sanctions. Fla. R. Civ. P. 1.720(b). The mediator controls the mediation process. Fla. R. Civ. P. 1.720(d). Counsel are permitted to communicate privately with their clients. Id. If the parties and mediator agree, mediation can proceed without counsel. Id. The mediator can meet privately with the parties or their counsel. Fla. R. Civ. P. 1.720(e).

If the mediation results in no agreement, the mediator reports this to the court without comment or recommendation. Fla. R. Civ. P. 1.730(a). The mediator also may identify pending motions or outstanding legal issues, discovery process or other actions whose resolution could facilitate the possibility of a settlement. Id. If an agreement is reached, it is reduced to writing and signed by the parties and their counsel. Fla. R. Civ. P. 1.730(b). Mediation proceedings are privileged, subject to limited exceptions. Fla. Stat. Sec. 44.102(3) (2003). Written communications in mediation are also exempt from Florida’s Public Records Act.Fla. Stat. Sec. 44.102(3) (2003).

B. Arbitration.

There are generally two types of court-ordered arbitration: mandatory non-binding arbitration and voluntary binding arbitration. In addition, arbitration often is ordered when the parties previously have agreed contractually to submit their claims to arbitration. See Fla. Stat. Sec. 682.02 (2003).

1. Mandatory (Non-Binding) Arbitration.

The court may direct the parties to participate in mandatory, non-binding arbitration. See Fla. Stat. Sec. 44.103(2) (2003). Unlike mediation, which is relatively informal, arbitration is similar to a mini-trial because arbitrators may administer oaths, take testimony, issue subpoenas and apply to the court for orders compelling attendance and production. Fla. Stat. Sec. 44.103(4) (2003). The arbitrator (or arbitration panel) renders a written decision that will become final if the parties do not submit a timely request for a trial de novo. Fla. Stat. Sec. 44.103(5) (2003). If a party requests a trial de novo and does not achieve a result that is more favorable than the arbitration award, that party may be assessed costs, including fees. Fla. Stat. Sec. 44.103(6) (2003).

2. Voluntary (Binding) Arbitration.

The parties also may agree in writing to submit their action to binding arbitration, except when constitutional issues are involved. Fla. Stat. Sec. 44.104(1) (2003). The parties may agree on the selection of one or more arbitrators; otherwise, they will be appointed by the court. Fla. Stat. Sec. 44.104(2) (2003). As in mandatory non-binding arbitration, the arbitrator has the power to administer oaths, issue subpoenas, etc. Fla. Stat. Sec. 44.104(7) (2003). A majority of the arbitrators may render a decision. Fla. Stat. Sec. 44.104(8) (2003). The Florida Rules of Evidence apply to voluntary binding arbitration proceedings. Fla. Stat. Sec. 44.104(9) (2003). Appeals to the circuit court are limited to statutorily defined issues, such as failure of the arbitrators to comply with procedural or evidentiary rules, misconduct, etc. Fla. Stat. Sec. 44.104(10) (2003). Disputes involving child custody, visitation, or child support, or the rights of a nonparty to the arbitration are non-arbitrable. Fla. Stat. Sec. 44.104(14) (2003). In addition, the court may require the parties in a medical malpractice action to submit to non-binding arbitration before a panel of arbitrators consisting of a plaintiff’s attorney, a health care practitioner or defense attorney, and a trial attorney. See Fla. Stat. Sec. 766.107(1) (2003). The panel considers the evidence and decides the issues of liability, amount of damages, and apportionment of responsibility among the parties, but may not award punitive damages. Fla. Stat. Sec. 766.107(3)(b) (2003). Voluntary binding arbitration is also available in medical malpractice actions. See Fla Stat. Sec. 766.207 (2003).

C. Offers of Judgment.

Before trial, a party may submit a written “offer of judgment” that offers to settle a claim on specified terms, e.g., for a specified amount, etc. Fla. Stat. Sec. 768.79(1) (2003). The other side has thirty (30) days to accept the offer in writing. If the plaintiff rejects an offer by a defendant under this section and ultimately obtains a judgment of no liability or at least twenty-five percent (25%) less than the offer, the plaintiff will be responsible for costs and fees from the date of the filing of the offer. Id. Likewise, if the defendant rejects a demand for judgment by the plaintiff under this section, and the plaintiff subsequently obtains a judgment that is at least twenty-five percent (25%) greater than the offer, the defendant will be responsible for plaintiff’s fees and costs incurred after the date of the filing of the demand. Id. An offer or demand may be withdrawn in writing at any time prior to its acceptance. Fla. Stat. Sec. 768.79(5) (2003). Another statute provides for the assessment of costs and fees against a party whose rejection of an offer of settlement subsequently is determined by the court to have been “unreasonable.” Unlike Fla. Stat. Sec. 768.79 an award of fees and costs under this section is not mandatory. However, this section does not apply to causes of action which accrue after October 1, 1990 and, therefore, the statute is all but obsolete. See Fla. Stat. Sec. 45.061 (2003). Given the availability of fees and costs under this section, it is a powerful mechanism for encouraging parties to consider settlement offers seriously.

V. Trial.

Although the majority of civil cases are resolved without a trial, many still proceed to trial. Once all motions directed to the last “pleading” Recall that “pleading” has a specialized meaning and refers to complaint and answer, counterclaim and response to counterclaim, crossclaim and response to crossclaim, etc.have been resolved of or, if no such motions were served, within twenty (20) days of the service of the last pleading, an action is “at issue,” and a party may notify the court that it is ready to be set for trial. Fla. R. Civ. P. 1.440(b). Typically, the court directs the parties to mediation if mediation already has not occurred. Otherwise, a trial date may be scheduled.

A. Demand for Jury.

The right to a jury trial in a civil case is not absolute and, in fact, may be waived if it is not demanded in a timely fashion. Fla. R. Civ. P. 1.430(d).

Typically, the demand for a jury trial is appended to the plaintiff’s complaint. A plaintiff may choose, however, for strategic purposes or otherwise, not to assert its jury trial right. However, both parties enjoy the right to a jury trial Fla. R. Civ. P. 1.430(a); Art. I, Sec. 22, Fla. Const. and a defendant who desires a jury trial typically will demand one in its answer or other responsive pleading. If a jury trial is not demanded within the time limits imposed by the rules of civil procedure, it is deemed waived. Fla. R. Civ. P. 1.430(d). If a jury trial is demanded, the demand thereafter may not be withdrawn without consent of the parties. Id.

A matter may be tried completely or partially to a jury. Fla. R. Civ. P. 1.430(c). However, parties are not entitled automatically to a jury trial in all cases because some matters, such as injunction proceedings, are not triable to a jury.

B. Jury Selection.

Assuming that a jury trial has been demanded, the first step in the trial process is jury selection. Prospective jurors may be provided with a questionnaire to determine any legal disqualifications (e.g., felony conviction). Fla. R. Civ. P. 1.431(a)(1). Fla. Stat. Sec. 40.013 (2003), disqualifies from jury service (1) those individuals who have been convicted of a felony and (2) the Governor, Lieutenant Governor, Cabinet officers, clerk of court, and judges. Fla. Stat. Sec. 40.013(1), (2)(a) (2003). This chapter also permits other individuals to be excused upon request, including law enforcement officers and their investigative personnel, expectant mothers and non-full-time employed single parents of children under six years old, practicing attorneys and physicians, the physically infirm, individuals over seventy (70) years old, individuals who demonstrate hardship, extreme inconvenience, or public necessity, and persons who care for certain incapacitated individuals. Id. Jurors also may be provided with questionnaires to assist in voir dire, or the oral examination of prospective jurors. Fla. R. Civ. P. 1.431(a)(2). The parties have the right to examine jurors orally on voir dire. Fla. R. Civ. P. 1.431(b). The court also may question prospective jurors. Id.

The parties may challenge any prospective juror “for cause,” i.e., if the juror is biased, incompetent, or related to a party or attorney for a party or has some interest in the action. Fla. R. Civ. P. 1.431(c)(1). There is no limit to the number of “for cause” challenges that may be raised. On the other hand, a party generally is limited to three (3) “peremptory” challenges, which do not require that the party establish cause, or any other reason for that matter. Fla. R. Civ. P. 1.431(d). However, there are constitutional limitations on peremptory challenges. For example, a party may not utilize its peremptory challenges to exclude prospective jurors in a racially discriminatory manner. See, e.g., State v. Johans, 613 So. 2d 1319, 1321 (Fla. 1993); State v. Neil, 457 So. 2d 481 (Fla. 1984); Laidler v. State, 627 So. 2d 1263 (Fla. 4th DCA 1993).

After the trial jury is selected, the court may provide for the selection of alternate jurors, and the parties generally are allowed one peremptory challenge for this process. Fla. R. Civ. P. 1.431(g). Alternate jurors are selected in the same manner as trial jurors, and are in all respects identical except that they are discharged if they are not needed when the jury retires to deliberate. Fla. R. Civ. P. 1.431(g)(1).

C. Opening Statements.

After a jury is selected, the parties present opening statements. Opening statements are not supposed to be arguments; rather, the parties should advise the jury of what the evidence will prove. After opening statements, the parties or the court may “invoke the rule,” which simply means that nonparty witnesses are excluded from the courtroom while others are testifying. Fla. Stat. Sec. 90.616 (2003). In addition, the witnesses are directed not to discuss the case with anyone other than the attorneys. H. Trawick, Florida Practice & Procedure Sec. 22-7, at 356 (1999).

D. Motion for Directed Verdict.

After the plaintiff presents its case-in-chief, the defendant may move for a directed verdict on the grounds that the plaintiff has failed to present sufficient evidence to justify submission of the case to the jury. Fla. R. Civ. P. 1.480(a). If the action is being tried to the court without a jury, the proper motion is a motion for involuntary dismissal under Fla. R. Civ. P. 1.420(b), as discussed earlier. If the motion is denied or reserved, the case proceeds, subject to the defendant’s ability to renew the motion at the close of the evidence. However, in a nonjury trial, renewal of the motion for involuntary dismissal at the close of the evidence is not authorized.

Orders granting directed verdict are unusual and scrutinized closely on appeal. Courts commonly “reserve ruling” on a motion for directed verdict and allow the case to proceed to the jury. This is a preferred approach because if the trial court grants a directed verdict and does not submit the case to the jury, and the directed verdict is overturned on appeal, the entire case must be retried. On the other hand, if the judge reserves ruling on the motion for directed verdict, the judge may override a subsequent plaintiff’s verdict and if that decision is overturned on appeal, the verdict may simply be reinstated without the necessity of a new trial.

After the plaintiff presents its case and any motions for directed verdict by either side are addressed, the defendant presents its case-in-chief. At the close of the defendant’s case, either party may move for a directed verdict. The plaintiff may present rebuttal evidence.

E. Closing Argument.

After the close of all the evidence, each side has an opportunity to present closing arguments. Because the plaintiff bears the burden of proof, the plaintiff is permitted to argue first and last (i.e., in rebuttal to defendant’s argument). The attorneys are required to confine their closing arguments to the evidence presented, along with its reasonable inferences. Alford v. Barnett Nat’l Bank, 137 Fla. 564, 188 So. 322 (1939). Case law restricts the types of arguments that may be presented in closing argument. For example, an attorney may not express a personal belief in his client or his client’s case. Miami Coin-O-Wash, Inc. v. McGough, 195 So. 2d 227 (Fla. 3d DCA 1967). He may not request that the jury place itself in his client’s shoes, i.e., the so-called “Golden Rule” argument. Bullock v. Branch, 130 So. 2d 74 (Fla. 1st DCA 1961).

F. Jury Instructions.

If the judge does not direct a verdict following the parties’ respective presentations, the case is submitted to a jury. Prior to the close of evidence, the parties must submit requested jury instructions. Fla. R. Civ. P. 1.470(b). These may include numerous form instructions pre-approved by the Florida Supreme Court. Additional instructions may need to be drafted and often there will be great debate between the parties on their wording.

The judge instructs the jurors on the manner in which they are expected to deliberate and the law that they must follow. Finally, the jurors retire to deliberate. Id. Frequently, the jury has questions during the deliberation process. The parties and their attorneys are notified of such questions. There may be some discussion or debate on how such questions are to be answered and the attorneys may object on the record to the answers ultimately provided to the jury.

G. Verdict.

Once the jury’s deliberations are complete, the verdict is announced in open court. A verdict may be either a “general” verdict or a “special” verdict. A general verdict “finds for a party in general terms on all issues within the province of the jury to determine.” H. Trawick, Florida Practice & Procedure Sec. 24-2, at 399 (1999). On the other hand, the court might employ a “special verdict,” which asks the jury to answer specific questions that determine the disputed facts. H. Trawick, Florida Practice & Procedure Sec. 24-3, at 400 (1999). For example, a special verdict form in a negligence action might require the jury to determine whether the defendant owed a duty to the plaintiff. If the answer to this question were negative, the court would enter judgment for the defendant because duty is an essential element of a negligence claim. A general verdict, on the other hand, might simply ask whether the jury’s verdict was for the plaintiff and, if so, for how much. Regardless of the form of verdict that is used, a separate verdict on each count must be required if requested by either party. H. Trawick, Florida Practice & Procedure Sec. 24-2, at 399 (1999). The verdict form is written and signed by the foreperson.

In negligence actions, the verdict is required to be itemized according to economic loss, noneconomic loss, and punitive damages (if awarded). Fla. Stat. Sec. 768.77(1) (2003). “Economic damages” refers to “past lost income and future lost income reduced to present value; medical and funeral expenses; lost support and services; replacement value of lost personal property; loss of appraised fair market value of real property; costs of construction repairs, including labor, overhead, and profit; and any other economic loss which would not have occurred but for the injury giving rise to the cause of action.” Fla. Stat. Sec. 768.81(1) (2003). In addition, damages must be itemized further into past and future damages. Fla. Stat. Sec. 768.77(2) (2003). Economic damages are computed before and after reduction to present value, but no other damages are reduced to present value. Id. After the verdict is read, either party may request that the individual jurors be polled. Each juror is asked then to confirm that the verdict read is his or her verdict. Once the requested polling is complete, the jury is discharged.

VI. Conclusion.

This post provides a general overview of the route of a civil lawsuit. Every lawsuit is different and the steps often vary dramatically. Pretrial proceedings frequently are overlooked as a valuable source of information. Although access to various components of the pretrial process is beyond the scope of this post, homeowners should view this post as a guide for successful wrongful foreclosure defense. Hopefully, this post will serve to “demystify” the pretrial process and assist homeowners gearing up to fight the wrongful foreclosure shops that are illegally snatching away their dream homes.

If you find yourself in an unfortunate situation of losing or about to lose your home to wrongful fraudulent foreclosure, and needed solutions to defend or reclaim your home please visit: http://www.fightforeclosure.net

27.664827

-81.515754