Mortgage fraud has continued to increase since the 2005. Declining economic conditions, liberal underwriting standards, and declining housing values contributed to the increased level of fraud. Market participants are perpetrating mortgage fraud by modifying old schemes, such as property flip, builder-bailout, and short sale fraud, as well as employing newer schemes, such as buy and bail, reverse mortgage fraud, loan modification, refinance fraud, and mortgage servicing fraud.

This Post defines schemes as the big picture or secret plan of action used to perpetrate a fraud. There are a variety of “schemes” by which mortgage fraud can take place. These schemes can involve individuals inside the financial institution or third parties. Various combinations of these schemes may be implemented in a single fraud. The descriptions provided below are examples of traditional and emerging schemes that are used to facilitate mortgage fraud.

Builder Bailout

This scheme is used when a builder, who has unsold units in a tract, subdivision, or condominium complex, employs various fraudulent schemes to sell the remaining properties.

Buy and Bail

This scheme typically involves a borrower who is current on a mortgage loan, but the value of the house has fallen below the amount owed. The borrower continues to make loan payments, while applying for a purchase money mortgage loan on a similar house that cost less due to the decline in market value. After obtaining the new property, the borrower “walks” or “bails” on the first loan.

Chunking

Chunking occurs when a third party convinces an uninformed borrower to invest in a property (or properties), with no money down and with the third party acting as the borrower’s agent. The third party is also typically the owner of the property or part of a larger group organizing the scheme. Without the borrower’s knowledge, the third party submits loan applications to multiple financial institutions for various properties. The third party retains the loan proceeds, leaving the borrower with multiple loans that cannot be repaid. The financial institutions are forced to foreclose on the properties.

Double Selling

Double selling occurs when a mortgage loan originator accepts a legitimate application and documentation from a buyer, reproduces or copies the loan file, and sends the loan package to separate warehouse lenders to each fund the loan.

Equity Skimming

Equity skimming is the use of a fraudulent appraisal that over-values a property, creating phantom equity, which is subsequently stripped out through various schemes.

Fictitious Loan

A fictitious loan is the fabrication of loan documents or use of a real person’s information to apply for a loan which the applicant typically has no intention of paying. A fictitious loan can be perpetrated by an insider of the financial institution or by external parties such as loan originators, real estate agents, title companies, and/or appraisers.

Loan Modification and Refinance Fraud

This scheme occurs when a borrower submits false income information and/or false credit reports to persuade the financial institution to modify or refinance the loan on more favorable terms.

Mortgage Servicing Fraud

This fraud is perpetrated by the loan servicer and generally involves the diversion or misuse of loan payments, proceeds from loan prepayments, and/or escrow funds for the benefit of the service provider.

Phantom Sale

This scheme generally involves an individual or individuals who falsely transfer title to a property or properties and fraudulently obtain funds via mortgage loans or sales to third parties.

Property Flip Fraud

A fraudulent property flip is a scheme in which individuals, businesses, and/or straw borrowers, buy and sell properties among themselves to artificially inflate the value of the property.

Reverse Mortgage Fraud

Reverse Mortgage Fraud involves a scheme using a reverse mortgage loan to defraud a financial institution by stripping legitimate or fictitious equity from the collateral property.

Short Sale Fraud

Fraud occurs in a short sale when a borrower purposely withholds mortgage payments, forcing the loan into default, so that an accomplice can submit a “straw” short-sale offer at a purchase price less than the borrower’s loan balance. Sometimes the borrower is truly having financial difficulty and is approached by a fraudster to commit the scheme. In all cases, a fraud is committed if the financial institution is misled into approving the short-sale offer, when the price is not reasonable and/or when conflicts of interest are not properly disclosed.

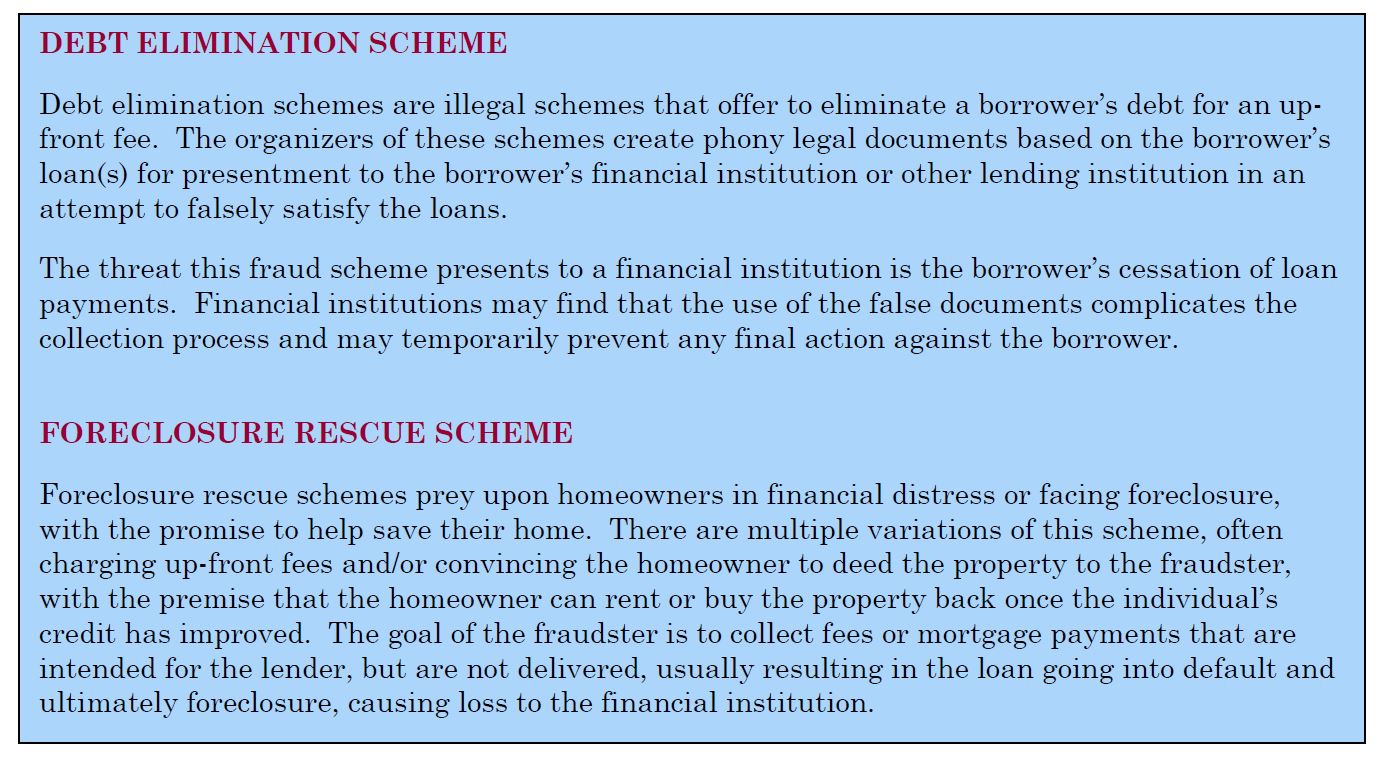

Two additional fraud schemes, which are briefly addressed below, are debt elimination and foreclosure rescue schemes. While these schemes are typically not perpetrated directly on financial institutions, and therefore not expanded upon to the same degree as the above-mentioned schemes, the end result of the scheme can have a negative impact on the financial institution.

COMMON MECHANISMS OF MORTGAGE FRAUD SCHEMES

This Post Paper defines mechanism as the process by which fraud is perpetrated. A single mortgage fraud scheme can often include one or more mechanisms and may involve collusion between two or more individuals working in unison to implement a fraud.

The following is a list of common mechanisms used to perpetrate mortgage fraud schemes:

Asset Rental

Cash or other assets are temporarily placed in the borrower’s account/possession in order to qualify for a mortgage loan. The borrower usually pays a “rental” fee for the temporary “use” of the assets.

Fake Down Payment

In order to meet loan-to-value requirements, a fake down payment through fictitious, forged, falsified, or altered documents is used to mislead the lender.

Fraudulent Appraisal

Appraisal fraud can occur when an appraiser, for various reasons, falsifies information on an appraisal or falsely provides an inaccurate valuation on the appraisal with the intent to mislead a third party.

Fraudulent Documentation

Fraudulent documentation consists of any forged, falsified, incomplete, or altered document that the financial institution relied upon in making a credit decision.

Fraudulent Use of Shell Company

A business entity that typically has no physical presence, has nominal assets, and generates little or no income is a shell company. Shell companies in themselves are not illegal and may be formed by individuals or business for legitimate purposes. However, due to lack of transparency regarding beneficial ownership, ease of formation, and inconsistent reporting requirements from state to state, shell companies have become a preferred vehicle for financial fraud schemes.

Identify Theft

Identity theft can be defined as assuming the use of another person’s personal information (e.g., name, SSN, credit card number, etc.) without the person’s knowledge and the fraudulent use of such knowledge to obtain credit.

Straw/Nominee Borrower

An individual used to serve as a cover for a questionable loan transaction.

COMMON PARTICIPANTS

Various individuals participate in mortgage fraud schemes. The following list consists of common participants in such schemes and each is linked to the glossary:

Appraiser – One who is expected to perform valuation services competently and in a manner that is independent, impartial, and objective.

Processor – The processor is an individual who assembles all the necessary documents to be included in the loan package.

Borrower – One who receives funds in the form of a loan with the obligation of repaying the loan in full with interest. The borrower may be purchasing property, refinancing an existing mortgage loan, or borrowing against the equity of the property for other purposes.

Real Estate Agent – An individual or firm that receives a commission for representing the buyer or seller, in a RE purchase transaction.

Buyer – A buyer is a person who is acquiring property.

Seller – Person offering to sell a piece of real estate.

Closing/Settlement Agent – An individual or company that oversees the consummation of a mortgage transaction at which the note and other legal documents are signed and the loan proceeds are disbursed. Title companies, attorneys, settlement agents, and escrow agents can perform this service. Local RE law may dictate the party conducting the closing.

Title Agent – The title agent is a person or firm that is authorized on behalf of a title insurer to conduct a title search and issue a title insurance report or title insurance policy.

Loan Servicer – A loan servicer is a public or private entity or individual engaged to collect and process payments on mortgage loans.

Underwriter – The credit decision-making process which can be automated, manual or a combination of both. In an automated process, application information is entered into a decision-making model that makes a credit determination based on pre-determined criteria. In a manual process an individual underwriter, usually an employee of the financial institution, makes the credit decision after evaluating all of the information in the loan package, including the credit report, appraisal, and verification of deposit, income, and employment. Financial institutions often use a combination of both, with the automated decision representing one element of the overall credit decision. In each case, the decision may include stipulations or conditions that must be met before the loan can close.

Originator – The individual or entity that gathers application data from the borrower. Alternatively, a person or entity, such as a loan officer, broker, or correspondent, who assists a borrower with the loan application.

Warehouse Lender – A short-term lender for mortgage bankers. Using mortgage loans as collateral, the warehouse lender provides interim financing until the loans are sold to a permanent investor.

CONCLUSION

Mortgage fraud continues to result in significant losses for financial institutions, as well as, the Homeowners. It is imperative that homeowners understand the nature of the various schemes and recognize red flags related to mortgage fraud. This knowledge and use of best practices will help with the prevention of mortgage fraud, and financial losses to the homeowner.

When Homeowner’s good faith attempts to amicably work with the Bank in order to resolve the issue fails;

Home owners should wake up TODAY! before it’s too late by mustering enough courage for “Pro Se” Litigation (Self Representation – Do it Yourself) against the Lender – for Mortgage Fraud and other State and Federal law violations using foreclosure defense package found at https://fightforeclosure.net/foreclosure-defense-package/ “Pro Se” litigation will allow Homeowners to preserved their home equity, saves Attorneys fees by doing it “Pro Se” and pursuing a litigation for Mortgage Fraud, Unjust Enrichment, Quiet Title and Slander of Title; among other causes of action. This option allow the homeowner to stay in their home for 3-5 years for FREE without making a red cent in mortgage payment, until the “Pretender Lender” loses a fortune in litigation costs to high priced Attorneys which will force the “Pretender Lender” to early settlement in order to modify the loan; reducing principal and interest in order to arrive at a decent figure of the monthly amount the struggling homeowner could afford to pay.

If you find yourself in an unfortunate situation of losing or about to lose your home to wrongful fraudulent foreclosure, and need a complete package that will show you step-by-step litigation solutions helping you challenge these fraudsters and ultimately saving your home from foreclosure either through loan modification or “Pro Se” litigation visit: https://fightforeclosure.net/foreclosure-defense-package/