The beginnings of the now multi-trillion dollar secondary market for residential mortgage loans date back to the federal government’s creation of Fannie Mae in 1938. Since then, the complexity of the secondary mortgage market has increased, especially as a result of the rapid growth and market acceptance of mortgage backed securities (“MBS”) that began in the 1980s. In contrast, the legal principles and processes by which mortgage-related promissory notes and security instruments (mortgages and deeds of trust) are assigned and transferred have centuries-old origins. Now, in the midst of the worst economic and housing crisis since the 1930s, some are questioning whether the traditional state law principles and processes of assignment and transfer can be fully reconciled with today’s complex holding, assignment and transfer systems for mortgage related promissory notes and security instruments, and what methods are legally effective for participants in the secondary mortgage market to establish, maintain and transfer mortgage notes and security instruments.

This post provides an overview of the legal principles and processes by which promissory notes and related mortgage security instruments are typically held, assigned, transferred and enforced in the secondary mortgage market in connection with loan securitizations and the creation of MBS.

1. Basic Principles

The two core legal documents in most residential mortgage loan transactions are the promissory note and the mortgage or deed of trust that secures the borrower’s payment of the promissory note. The promissory note contains a promise by the borrower to pay the lender a stated amount of money at a specified interest rate (which can be fixed or variable) by a certain date. The typical mortgage or deed of trust contains a grant of a mortgage lien or other security interest in the borrower’s real property to the lender or, in a deed of trust, to a trustee for the benefit of the lender, to secure the borrower’s obligations under the promissory note.

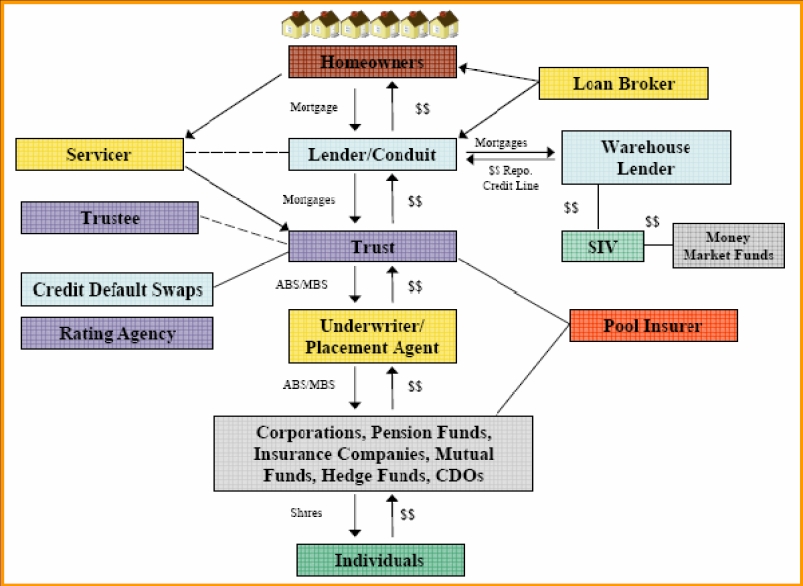

In a typical “private-label” mortgage loan securitization, each mortgage loan, which is evidenced by a mortgage note and secured by a mortgage, is sold, assigned and transferred to a trust through a series of steps:

• The loan originator or a subsequent purchaser sells, assigns and transfers the mortgage loans to a “sponsor,” which is typically a financial services company or a mortgage loan conduit or aggregator.

• The sponsor sells, assigns and transfers the mortgage loans to a “depositor,” which in turn sells, assigns and transfers the mortgage loans to the trustee, which will hold the mortgage loans in trust for the benefit of the certificate holders.

• The trustee issues the MBS pursuant to a pooling and servicing agreement or trust agreement entered into by the depositor, the trustee and a master servicer or servicers.

• The trustee administers the pool assets, typically relying on the loan servicer to perform most of the administrative functions regarding the pool of mortgage loans. In addition, a document custodian is often designated to conduct a review of the mortgage loan documents pursuant to the requirements of the pooling and servicing agreement and to hold

the mortgage loan documents for the loans included in the trust pool.

• In general, the loan documents are assigned and transferred from the depositor to the trustee through the indorsement of the mortgage note and the transfer of possession of the mortgage note to the trustee or a custodian on behalf of the trustee. An assignment of the related mortgage is also typically delivered to the transferee or its custodian, except

in cases where the related mortgage identifies Mortgage Electronic Registration Systems (“MERS”) as the mortgagee. Such assignments generally are in recordable form, but unrecorded, and are executed by the transferor without identifying a specific transferee – a so called assignment in blank.

• In some mortgage loan transactions, MERS becomes the mortgagee of record as the nominee of the loan originator and its assignee in the local land records where the mortgage is recorded, either when the mortgage is first recorded or as a result of the recording of an assignment of mortgage to MERS. This means that MERS is listed as the record title holder of the mortgage. MERS’ name does not appear on the mortgage note, and the beneficial interest in the mortgage remains with the loan originator or its assignee. The documents pursuant to which MERS acts as nominee make clear that MERS is acting in such capacity for the benefit of the loan originator or its assignee. When a mortgage loan is originated with MERS as the nominal mortgagee (or is assigned to MERS post-origination), MERS

tracks all future mortgage loan and loan servicing transfers and other assignments of the mortgage loan unless and until ownership or servicing is transferred (or the loan is otherwise assigned) to an entity that is not a MERS member. In this way, MERS serves as a central system to track changes in ownership and servicing of the loan. Fannie Mae, Freddie Mac and Ginnie Mae, among other governmental entities, permit loans that they

purchase or securitize to be registered with MERS.

As part of the loan securitization process detailed above, a mortgage note and a mortgage may be sold, assigned and transferred several times from one entity to another. The legal principles that govern the assignment and transfer of mortgage notes and mortgages are generally determined by state law. See, e.g., In re Cook, 457 F.3d 561, 566 (6th Cir. 2006) (state law governed whether transferee had superior interest in promissory note secured by mortgage). As such, these principles can vary depending upon the state in which the assignor of the mortgage notes, the underlying property, or the relevant mortgage-related documents are located. The assignment and transfer of a mortgage note, on the one hand, and of a mortgage, on the other hand, are addressed separately below.

2. Transfer of Promissory Notes Secured by Mortgages

The residential mortgage notes in common use in the secondary mortgage market typically are negotiable instruments. The law of negotiable instruments developed over the centuries as a way to encourage commerce and lending by making such instruments, including negotiable mortgage notes, as liquid and transferable as possible. See, e.g., Overton v. Tyler, 3 Pa. 346, 347 (1846) (“[A] negotiable bill or note is a courier without luggage”); 2 Frederick M. Hart & William F. Willier, Negotiable Instruments Under the Uniform Commercial Code § 1.01 (“Negotiable instruments play such an important role in the modern commercial world that it is difficult to realize that the struggle for their existence could be as long and complex as it has been, yet the evolution of the concept took centuries.”). Similarly, the standardization of the forms of mortgage notes and mortgages over the past thirty years or more has contributed to the liquidity and transferability of mortgage notes and the underlying mortgages. See Peter M. Carrozzo, Marketing the American Mortgage: The Emergency Home Finance Act of 1970, Standardization and the Secondary Market Revolution, 39 Real Prop. Prob. & Tr. J. 765, 799-800 (2004-2005) (“standardization of mortgage documents created marketable commodities. Once mechanisms were in place for the secondary market to operate, events rapidly moved toward the ultimate goal: the creation of a security which has as its base land [and] yet which will be as freely transferable as stocks and bonds” (internal quotation omitted)).

The Uniform Commercial Code (“UCC”), which, with state-specific variations, has been adopted as law by all 50 states and the District of Columbia, governs, in significant part, the transfer of mortgage notes. Article 3 applies to the negotiation and transfer of a mortgage note that is a “negotiable instrument,” as that term is defined in Article 3. See UCC §§ 3-102, 3-201, 3-203 and 3-204; see, e.g., Swindler v. Swindler, 355 S.C. 245, 250 (S.C. Ct. App. 2003) (Article 3 governs negotiable mortgage note). In addition, Article 9 applies to the sale of “promissory notes,” a term that generally includes all mortgage notes (both negotiable and nonnegotiable). See UCC §§ 1-201(b)(35) and 9-109(a)(3)

The residential mortgage notes in common use today are typically negotiable instruments for UCC purposes. In addition, as a general matter, the securitization of a loan under a typical pooling and servicing agreement provides both for the negotiation of negotiable mortgage notes (by indorsement and transfer of possession to the securitization trustee or the custodian for the trustee) and for an outright sale and assignment of all of the mortgage notes and related mortgages. Thus, whether the mortgage notes in a given securitization pool are deemed “negotiable” (as we believe most typically are) or “non-negotiable” will have little or no

substantive effect under the UCC on the validity of the transfer of the mortgage notes. The typical securitization process effects valid transfers of the mortgage notes and related mortgages in accordance with the provisions of Articles 3 and 9 of the UCC.

What Constitutes a “Negotiable Instrument?

A “negotiable instrument” is defined as:

an unconditional promise or order to pay a fixed amount of money, with or without interest or other charges described in the promise or order, if it:

(1) is payable to bearer or to order at the time it is issued or first comes into possession of a holder;

(2) is payable on demand or at a definite time; and

(3) does not state any other undertaking or instruction by the person promising or ordering payment to do any act in addition to the payment of money, but the promise or order may contain (i) an undertaking or power to give, maintain, or protect collateral to secure payment, (ii) an authorization or power to the holder to confess judgment or realize on or dispose of collateral, or (iii) a waiver of the benefit of any law intended for the advantage or protection of an obligor.

UCC § 3-104(a).

Reference in a mortgage note to a mortgage does not affect the mortgage note’s status as a negotiable instrument. See UCC § 3-106(b) (“A promise or order is not made conditional [] by a reference to another writing for a statement of rights with respect to collateral, prepayment, or acceleration….”); see also Int’l Minerals & Chem. Corp. v. Matthews, 321 S.E.2d 545, 547 (N.C. Ct. App. 1984) (“referring to a mortgage or other collateral [in a mortgage note] does not impair negotiability” of the note); In re AppOnline.com, 285 B.R. 805, 815-16 (Bankr. E.D.N.Y. 2002) (reference in mortgage notes to underlying mortgages does not affect the negotiability of the notes).

The fact that a mortgage note contains a variable or adjustable interest rate also does not affect the mortgage note’s status as a negotiable instrument. That is because UCC § 3-112(b) provides that “[i]nterest may be stated in an instrument[7] as a fixed or variable amount of money or it may be expressed as a fixed or variable rate or rates. The amount or rate of interest may be stated or described in the instrument in any manner and may require reference to information not contained in the instrument.” UCC § 3-112(b).

How is a Negotiable Mortgage Note Transferred?

A negotiable mortgage note is transferred when it is “delivered” by a person other than the mortgagor for the purpose of giving the transferee the right to enforce the note. See UCC § 3-203(a). “Delivery” of a mortgage note occurs when there has been a voluntary transfer of possession of the mortgage note. See UCC § 1-201(b)(15). As a general matter, the “[t]ransfer of an instrument, whether or not the transfer is a negotiation, vests in the transferee any right of the transferor to enforce the instrument . . . .” UCC § 3-203(b). Accordingly, a person in possession of the note becomes a “person entitled to enforce” if it can prove that it is the transferee. See UCC § 3-301.

The easiest and most common way to transfer a negotiable mortgage note is through “negotiation.” Article 3 defines “negotiation” as “a transfer of possession, whether voluntary or involuntary, of an instrument by a person other than the issuer to a person who thereby becomes its holder.” UCC § 3-201(a). The “negotiation” of a negotiable mortgage note that is payable to an identified person or entity (such as the entity that originated a mortgage loan and whose name appears as the payee in the mortgage note) – “requires transfer of possession of the instrument and its indorsement by the holder.” UCC § 3-201(b) (emphasis added). As explained below, “indorsement” and “holder” are both defined terms in the UCC.

The “holder” of a negotiable mortgage note is “the person in possession of [the mortgage note] that is payable either to bearer or to an identified person that is the person in possession.” UCC § 1-201(b)(21)(A). In other words, upon the closing of a mortgage loan, the “holder” of the mortgage note is the entity that is the payee on the mortgage note and that possesses the note (either actually or constructively). After a negotiable mortgage note has been negotiated, such as in connection with a loan securitization, the “holder” of the mortgage note is the entity that possesses the mortgage note if the mortgage note was indorsed to that entity or if the mortgage note was indorsed in blank or to bearer.

The term “indorsement” is defined to include “a signature . . . that alone or accompanied by other words is made on an instrument [in our case, a negotiable mortgage note] for the purpose of . . . negotiating the instrument.” UCC § 3-204(a). Such an indorsement may be either a “special indorsement” or a “blank indorsement.” See UCC § 3-205. A “special indorsement” is a written indorsement that specifically “identifies a person to whom it makes the instrument payable.” UCC § 3-205(a). A “blank indorsement” is an indorsement that does not identify a person to whom the instrument is payable. See UCC § 3-205(b). Mortgage notes that are transferred in connection with loan securitizations are typically indorsed in blank with language such as “Pay to the order of _____________,” where no name is filled in the blank. The effect of an indorsement in blank is significant: “When indorsed in blank, an instrument becomes payable to bearer and may be negotiated by transfer of possession alone until specially indorsed.” UCC § 3-205(b) (emphasis added).10 See also UCC § 3-201(b) (The negotiation of a negotiable mortgage note that is payable to bearer (such as a negotiable mortgage note that has been indorsed in blank) is effected by “transfer of possession alone.”).

The term “possession” is not defined in the UCC. Thus, courts rely on common law definitions of possession to interpret that concept in the context of the negotiation of an instrument such as a mortgage note. See, e.g., In re Kelton Motors, Inc., 97 F.3d 22, 26 (2d Cir. 1996) (because Article 3 does not define “possession,” a court must look to the general law of the jurisdiction in determining whether a party is in possession of a negotiable instrument).

Possession can be, and very often is, effected by an agent, nominee or designee, such as the designated custodian for the securitization trust. See, e.g., Midfirst Bank, SB v. C.W. Haynes and Co., Inc., 893 F. Supp. 1304, 1314-15 (D.S.C. 1994) (constructive possession exists when an authorized agent of the owner holds the note on behalf of the owner); Jenkins v. Evans, 31 A.D.2d 597, 598 (N.Y. App. Div. 3d Dept. 1968) (agent had authority to possess instruments for principal). In such cases, while the designated custodian has “physical” possession of the mortgage note, the trustee for which the custodian holds the mortgage note has “constructive” or “legal” possession. See Midfirst Bank, 893 F.Supp. at 1314-15; see also UCC § 9-313 cmt. (“if the collateral is in [the] possession of an agent of the secured party for the purposes of possessing on behalf of the secured party, and if the agent is not also an agent of the debtor, the secured party has taken actual possession” (emphasis added)).

Who May Enforce A Negotiable Mortgage Note?

The maker of a mortgage note is obligated to pay the note to the “person entitled to enforce the instrument.” UCC § 3-412. The “person entitled to enforce” a negotiable mortgage note includes “(i) the holder of the instrument, [and] (ii) a nonholder in possession of the instrument who has the rights of a holder.” UCC § 3-301. Accordingly, to enforce a mortgage note against the borrower, a person must generally prove either that it is a “holder” or that it is a transferee with the rights of a holder. See UCC § 3-301. The first category of persons that may enforce a mortgage note is a “holder.” A “holder” of a negotiable mortgage note is “the person in possession of [the mortgage note] that is payable either to bearer or to an identified person that is the person in possession.” UCC § 1-201(b)(21)(A). The manner in which one becomes a “holder” is described in the section above.

The second category contemplated by UCC § 3-301– a “nonholder in possession who has the rights of a holder” – is more difficult to define. Under this clause, a person would qualify as a “nonholder in possession” if possession of the mortgage note was transferred to him from the transferor, but the transferor did not indorse the mortgage note. See UCC § 3-203 cmt. In this circumstance, the transferee is entitled to enforce the instrument, but to do so, the transferee must first prove both possession of the unindorsed mortgage note and prove the transfer of the mortgage note by the holder to the transferee. See id. Under both clauses, the person seeking to enforce the mortgage note must have possession of the note.

UCC § 3-301 also permits a person without possession to enforce a mortgage note where the mortgage note has been lost, stolen, or destroyed within the meaning of UCC § 3-309. See UCC § 3-301.12 Courts have consistently affirmed the use of UCC § 3-309 to enforce lost, stolen or destroyed negotiable mortgage notes that a party, such as a securitization trustee, seeks to enforce when the party has proven the terms of the mortgage notes and its right to enforce the mortgage notes (i.e., it has proven the transfer of the mortgage note from the transferee). See, e.g., In re Montagne, 421 B.R. 65, 79 (D. Vt. 2009) (finding that plaintiff who satisfied requirements of UCC § 3-309 could enforce lost mortgage note); Waggoner v. Mortgage Elect. Registration Sys., Inc., No. 2003-CA-002666-MR, 2005 WL 2175439, at *1 n.1 (Ky. App. Ct. Sept. 9, 2005) (“The promissory note was proven … by an affidavit concerning a lost or destroyed promissory note.”).

What Rights Against Borrower Defenses are Available to the Holder of a Negotiable Mortgage Note?

A key concept relating to the negotiation of negotiable mortgage notes is the “holder in due course” doctrine. That is because where the “holder” of a negotiable mortgage note is deemed a “holder in due course,” the holder takes the mortgage note subject only to specific limited defenses of the borrower. The following is a brief summary of an expansive area of law. Under UCC § 3-302(a):

[A] “holder in due course” means the holder of an instrument if:

(1) the instrument when issued or negotiated to the holder does not bear such apparent evidence of forgery or alteration or is not otherwise so irregular or incomplete as to call into question its authenticity; and

(2) the holder took the instrument (i) for value, (ii) in good faith, (iii) without notice that the instrument is overdue or has been dishonored or that there is an uncured default with respect to payment of another instrument issued as part of the same series, (iv) without notice that the instrument contains an unauthorized signature or has been altered, (v) without notice of any claim to the instrument described in Section 3-306 [regarding claims of a property or possessory right in the instrument or its proceeds, including a claim to rescind a negotiation and to recover the instrument or its proceeds], and (vi) without notice that any party has a defense or claim in recoupment described in Section 3-305(a).

UCC § 3-302(a).

Under Article 3, a holder in due course of a negotiable mortgage note takes the mortgage note free of (a) all prior claims to or regarding the mortgage note by any person and (b) most defenses to enforceability of the mortgage note that may be raised by parties with whom the holder in due course has not dealt. See UCC §§ 3-305 and 3-306; see also Provident Bank v. Community Home Mortgage Corp., 498 F. Supp. 2d 558, 565 (E.D.N.Y. 2007). The defenses to which a holder in due course may be subject are found in UCC § 3-305, and

include:

a defense of the obligor based on (i) infancy of the obligor to the extent it is a defense to a simple contract, (ii) duress, lack of legal capacity, or illegality of the transaction which, under other law, nullifies the obligation of the obligor, (iii) fraud that induced the obligor to sign the instrument with neither knowledge nor reasonable opportunity to learn of its character or its essential terms, or (iv) discharge of the obligor in insolvency proceedings.

UCC § 3-305(a)(1).

How Is a Mortgage Note Transferred Under Article 9 of the UCC?

The sale of mortgage notes is also governed, in significant part, by Article 9. Article 9 establishes

(1) whether the interests of a transferee of a mortgage note have both “attached” and become “perfected” so that those interests will prevail over conflicting claims of third parties and (2) the rights of the transferee in and to the underlying mortgage that secures the mortgage note.

Article 9 addresses the sale of mortgage notes, regardless of whether they are negotiable or nonnegotiable. More specifically, Article 9 applies to “a sale of . . . promissory notes.” UCC § 9-109(a)(3). A “promissory note” is defined as “an instrument that evidences a promise to pay a monetary obligation, does not evidence an order to pay, and does not contain an acknowledgment by a bank that the bank has received for deposit a sum of money or funds.” UCC § 9-102(a)(65). Given this broad definition, residential mortgage notes in common use today are typically “promissory notes” for purposes of Article 9.

Under Article 9, the sale of a mortgage note (whether or not the mortgage note is negotiable) is deemed a secured transaction and the transferee’s “security interest” is automatically perfected when it attaches (more on “attachment” and “perfection” below). See UCC § 9-309(4). While security interests are most commonly thought of as the liens obtained by lenders, the UCC defines the term “security interest” to also include “any interest of a . . . buyer of . . . a promissory note in a transaction that is subject to Article 9.” UCC § 1-201(b)(35) (emphasis added). In addition, the definition of “secured party” includes “a person to which . . . promissory notes have been sold.” UCC § 9-102(a)(72)(D).

Before a buyer’s “security interest” in a mortgage note can be perfected under Article 9, the security interest must “attach.” A security interest attaches when (1) value has been given for the sale, (2) the seller has rights in the mortgage note or the power to transfer rights in the mortgage note to the buyer and (3) either (a) the mortgage note is in the possession of the buyer pursuant to a security agreement of the seller or (b) the seller has signed a written or electronic security agreement that describes the mortgage note. See UCC § 9-203(b). Article 9 defines “security agreement” as “an agreement that creates or provides for a security interest,” UCC § 9-102(a)(73), which, in the context of a mortgage loan securitization, would include an agreement pursuant to which mortgages and mortgage notes are sold and transferred from one entity to another. Such an agreement, normally a pooling and servicing agreement or trust agreement, typically will provide that the transfer of the mortgage note pursuant thereto effects a sale of the mortgage note, which would thus, under Article 9, constitute a “security agreement.”

Significantly, the attachment of a security interest in a mortgage note that is itself “secured by a security interest or other lien on personal or real property is also attachment of a security interest in the security interest, mortgage or other lien.” UCC § 9-203(g) (emphasis added). Similarly, under UCC § 9-308(e), perfection of a security interest in a promissory note “also perfects a security interest in a security interest, mortgage, or other lien on personal or real property securing the right.” UCC § 9-308(e) (emphasis added). In other words, perfection of a security interest (which includes a sale to a buyer) in a mortgage note pursuant to Article 9 also perfects a security interest in the mortgage that secures the note.

Perfection of the interest in the mortgage note is important because it provides the transferee of the mortgage note with a right in the mortgage note and mortgage superior to that of a subsequent lien creditor of the seller. And, perfection provides the transferee of the mortgage note with a right in the mortgage superior to that of a subsequent lien creditor of the mortgagee, which includes a bankruptcy trustee (see UCC § 9-102(a)(52)). See UCC § 9-308 cmt.

Transfer of Mortgage Notes: Conclusion

In summary, under the UCC, the transfer of a mortgage note that is a negotiable instrument is most commonly effected by indorsing the note, which may be a blank or special indorsement, and delivering the mortgage note to the transferee (or the agent acting on behalf of the transferee). As the residential mortgage notes in common usage typically are “negotiable instruments,” this is the most common method of transfer.

In addition, even without indorsement, the assignment can be effected by transferring possession under UCC § 3-203(a). Moreover, the sale of any mortgage note also effects the assignment and transfer of the mortgage under Article 9. The attachment and perfection of the buyer’s interest in the mortgage note attaches and perfects the buyer’s interest in the underlying mortgage that secures the mortgage note. Securitization agreements often

provide both for (a) the indorsement and transfer of possession to the trustee or the custodian for the trustee, which would constitute a negotiation of the mortgage note under Article 3 of the UCC and (b) an outright sale and assignment of the mortgage note. Thus, regardless of whether the mortgage notes in a securitization trust are deemed “negotiable” or “non-negotiable,” the securitization process generally includes a valid transfer of the mortgage notes to the trustee in accordance with the explicit requirements of the UCC.

3. Assignment and Transfer of Ownership of Mortgages

As described above, when a mortgage loan is assigned and transferred as part of the securitization of the loan in the secondary market, both the mortgage note and the mortgage itself are typically sold, assigned, and physically transferred to the trustee that is acting on behalf of the MBS investors or to a trustee-designated document custodian pursuant to a custody agreement. The assignment and transfer are usually documented and performed in accordance with a pooling and servicing agreement.

What is the Relationship Between the Transfer of a Mortgage Note and the Transfer of Ownership of the Mortgage?

When a mortgage note is transferred in accordance with common mortgage loan securitization processes, the mortgage is also automatically transferred to the mortgage note transferee under the UCC and the general common law rule that “the mortgage follows the note.” See, e.g., Carpenter v. Longan, 83 U.S. 271, 275 (1873) (“The transfer of the note carries with it the security, without any formal assignment or delivery, or even mention of the latter.”); Mortgage Elect. Registration Sys., Inc. v. Coakley, 41 A.D.3d 674, 674 (N.Y. App. Div. 2d Dept. 2007) (“the mortgage . . . passed as an incident to the promissory note”); Restatement (Third) of Property, Mortgages § 5.4(a) (1997) (“A transfer of an obligation secured by a mortgage also transfers the mortgage . . . . ”).

The rule that “the mortgage follows the note” has been codified in the UCC, but the rule’s common law origins date back hundreds of years, long before the creation of the UCC. As stated in the official comments to UCC § 9-203(g), that section “codifies the common-law rule that a transfer of an obligation secured by a security interest or other lien on personal or real property also transfers the security interest or lien.” UCC §9-203 cmt.

All states follow this rule.16 In addition to the codification of the rule under UCC § 9-203(g), reported court cases in nearly every state and non-UCC statutory provisions in some states make clear that “the mortgage follows the note”:

Alabama: Armour Fertilizer Works v. Zills, 177 So. 136, 138 (Ala. 1937) (“when the note is secured by a mortgage, such mortgage follows the note”).

Arizona: Ariz. Rev. Stat § 33-817 (“The transfer of any contract or contracts secured by a trust deed shall operate as a transfer of the security for such contract or contracts.”).

Arkansas: Leach v. First Cmty. Bank, No. CA 07-05, 2007 WL 2852599, at *1 (Ark. App. Ct. Oct. 3, 2007) (“Arkansas has long followed the rule that, in the absence of an agreement or a plain manifestation of a contrary intention, the security of the original mortgage follows the note or renewal thereof.”).

California: Cal. Civ. Code § 2936 (“The assignment of a debt secured by mortgage carries with it the security”); In re Staff Mortgage & Invest. Corp., 625 F.2d 281, 284 (9th Cir. 1980) (in California, “[A] deed of trust is a mere incident of the debt it secures and . . . an assignment of the debt ‘carries with it the security.” (internal quotation omitted)).

Colorado: Carpenter v. Longan, 83 U.S. 271, 275 (1873) (in an appeal from the Supreme Court of Colorado Territory, the United States Supreme Court stated: “The transfer of the note carries with it the security, without any formal assignment or delivery, or even mention of the latter.”).

Connecticut: Conn. Gen. Stat. § 49-17 (“When any mortgage is foreclosed by the person entitled to receive the money secured thereby but to whom the legal title to the mortgaged premises has never been conveyed, the title to such premises shall, upon the expiration of the time limited for redemption and on failure of redemption, vest in him in the same manner and to the same extent as such title would have vested in the mortgagee if he had foreclosed, provided the person so foreclosing shall forthwith cause the decree of foreclosure to be recorded in the land records in the town in which the land lies.”); In re AMSCO, Inc., 26 B.R. 358, 361 (Bankr. D. Conn. 1982) (“An assignment of the note carries the mortgage with it . . . .”).

District of Columbia: Hill v. Hawes, 144 F.2d 511, 513 (D.C. Cir. 1944) (after mortgage note has been cancelled, cancellation of “any mortgage follows as a matter of course and does not require a separate action”).

Florida: Capital Investors Co. v. Ex’rs of Estate of Morrison, 484 F.2d 1157, 1163 n.12 (4th Cir. 1973) (“That the mortgage follows the note it secures and derives negotiability, if any, from the note is the rule in Florida where the land under mortgage in this case was located.” (citing Daniels v. Katz, 237 So.2d 58, 60 (Fla. App. 1970); Meyerson v. Boyce, 97 So.2d 488, 489 (Fla. App. 1957))); Margiewicz v. Terco Properties, 441 So.2d 1124, 1125 (Fla. Dist. Ct. App. 1983) (when a note secured by a mortgage is assigned, the mortgage follows the note into the hands of the mortgagee).

Illinois: Federal Nat’l Mort. Ass’n v. Kuipers, 314 Ill. App.3d 631, 635, 732 N.E.2d 723, 727 (Ill. Ct. App. 2000) (“The assignment of a mortgage note carries with it an equitable assignment of the mortgage by which it was secured. The assignee stands in the shoes of the assignor-mortgagee with regard to the rights and interests under the note and mortgage. . . . [I]n Illinois, the assignment of the mortgage note is sufficient to transfer the underlying mortgage.”) (citations omitted).

Indiana: Lagow v. Badollet, 1 Blackf. 416, 1826 WL 1087, at *3 (Ind. 1826) (“a mortgage . . . follows the debt into whose hands soever it may pass”).

Iowa: Bremer County Bank v. Eastman, 34 Iowa 392, 1872 WL 254, at *1 (Iowa 1872) (“The transfer of the note, secured by the mortgage, carried the mortgage with it as an incident to the debt, and the indorsee of the note could maintain an action in his own name, to foreclose the mortgage without any assignment thereon whatever.”).

Kansas: Kan. Stat. Ann § 58-2323 (“The assignment of any mortgage as herein provided shall carry with it the debt thereby secured.”); Bank Western v. Henderson, 255 Kan. 343, 354, 874 P.2d 632, 640 (1994) (“[T]he mortgage follows the note. A perfected claim to the note is equally perfected as to the mortgage.”).

Maryland: In re Bird, No. 03-52010-JS, 2007 WL 2684265, at *2-4 (Bankr. D.Md. Sept. 7, 2007) (“The note and mortgage are inseparable; the former as essential, the latter as an incident. An assignment of the note carries the mortgage with it . . . .”).

Massachusetts: The transfer of a mortgage note, without the express transfer of the mortgage, vests in the note holder an equitable interest in the mortgage (an interest that can be enforced by the note holder) and the mortgage holder is deemed to hold the mortgage in constructive trust for the benefit of the note holder. See Weinberg v. Brother, 263 Mass. 61, 62 (1928); Barnes v. Boardman, 149 Mass. 106, 114 (1889); Morris v. Bacon, 123 Mass. 58, 59 (1877); First Nat’l Bank of Cape Cod v. North Adams Hoosac Savs. Bank, 7 Mass. App. Ct. 790, 796 (1979); see also In re Ivy Properties, Inc., 109 B.R. 10, 14 (Bankr. D. Mass. 1989) (“[U]nder Massachusetts common law the assignment of a debt carries with it the underlying mortgage, without necessity for the granting or recording of a separate mortgage assignment.”).

Despite the above cited authorities, the Massachusetts Land Court in a recent opinion cast doubt on the “mortgage follows the note” rule:

[E]ven a valid transfer of the note does not automatically transfer the mortgage. . . . The holder of the note may have an equitable right to obtain an assignment of the mortgage by filing an action in equity, but that is all it has. . . . The mortgage itself remains with the mortgagee (or, if properly assigned, its assignee) who is deemed to hold the legal title in trust for

the purchaser of the debt until the formal assignment of the mortgage to the note holder or, absent such assignment, by order of the court in an action for conveyance of the mortgage.

. . . But . . . the right to get something and actually having it are two different things.

U.S. Bank Nat’l Ass’n v. Ibanez, Nos. 08 MISC 384283 (KCL), 08 MISC 386755 (KCL), 2009 WL 3297551, at *11 (Mass. Land Ct. Oct. 14, 2009) (citations omitted).

The Ibanez case appears to stand in stark contrast to the principles embodied in the UCC.

The Ibanez case was affirmed and Judges concurred on appeal before the Massachusetts Supreme Judicial Court, that state’s highest court.

Michigan: Prime Fin. Serv. v. Vinton, 279 Mich. App. 245, 257, 761 N.W.2d 694, 704 (Mich. Ct. App. 2008) (“the transfer of a note necessarily includes a transfer of the mortgage with it”) (citing Ginsberg v. Capitol City Wrecking Co., 300 Mich. 712, 717, 2 N.W.2d 892 (1942)); Jones v. Titus, 208 Mich. 392, 397, 175 N.W. 257, 259 (Mich. 1919) (when a note given with a mortgage was indorsed over to a third party it carried with it the equitable title to the mortgage).

Minnesota: Jackson v. Mortgage Elect. Registration Sys., Inc., 770 N.W.2d 487, 497 (Minn. 2009) (“Absent an agreement to the contrary, an assignment of the promissory note operates as an equitable assignment of the underlying security interest.”) (emphasis in original).

Mississippi: Holmes v. McGinty, 44 Miss. 94, 1870 WL 4406, at *4 (“[T]he mortgage . . . follows the debt as an incident, and is a security for whomsoever may be the beneficial owner of it.”).

Missouri: George v. Surkamp, 76 S.W.2d 368, 371 (Mo. 1934) (when the holder of the promissory note assigns or transfers the note, the deed of trust is also transferred).

Montana: First Nat’l Bank v. Vagg, 65 Mont. 34, 212 P. 509, 511 (Mont. 1922) (“The note and mortgage are inseparable; the former as essential, the latter as an incident. An assignment of the note carries the mortgage with it, while the assignment of the latter alone is a nullity. The mortgage can have no separate existence.”) (citations omitted).

Nebraska: In re Union Packing Co., 62 B.R. 96, 100 (Bankr. D. Neb. 1986) (with or without the

assignment of the mortgage, the assignee of the promissory note has the right to enforce the mortgage securing the note).

New Hampshire: Southerin v. Mendum, 5 N.H. 420, 1831 WL 1104, at *7 (N.H. 1831) (“When a

mortgagee transfers to another person , the debt which is secured by the mortgage, he ceases to have any control over the mortgage. . . . And we are of the opinion, that the interest of the mortgagee passes in all cases with the debt, and that it is not within the statute of frauds, because it is a mere incident to the debt, has no value independent of the debt, and cannot be separated from the debt.”).

New Jersey: In re Kennedy Mort. Co., 17 B.R. 957, 966 (Bankr. D. N.J. 1982) (“Anyone interested in acquiring an interest in the mortgage would be obliged to obtain an interest in the debt.”).

New York: Mortgage Elec. Registration Sys., Inc. v. Coakley, 41 A.D.3d 674, 838 N.Y.S.2d 622 (App. Div. 2007) (“at the time of the commencement of this action, MERS was the lawful holder of the promissory note (see UCC 3-204[1]; Franzese v. Fidelity N.Y. FSB, 214 A.D.2d 646, 625 N.Y.S.2d 275), and of the mortgage, which passed as an incident to the promissory note (see Payne v. Wilson, 74 N.Y. 348, 354-355; see also Weaver Hardware Co. v. Solomovitz, 235 N.Y. 321, 139 N.E. 353; Matter of Falls, 31 Misc. 658, 660, 66 N.Y.S. 47, aff’d. 66 A. D. 616, 73 N.Y.S. 1134”) (emphasis added); Provident Bank v. Community Home Mortgage Corp., 498 F. Supp. 2d 558, 564-65 (E.D.N.Y. 2007) (applying principle that the mortgage follows the note).

North Carolina: Dixie Grocery Co. v. Hoyle, 204 N.C. 109, 167 S.E. 469 (1933) (“The mortgage follows the debt.”).

Ohio: U.S. Nat’l Bank Ass’n v. Marcino, 181 Ohio App.3d 328, 337 (2009) (“[T]he negotiation of a note operates as an equitable assignment of the mortgage, even when the mortgage is not assigned or delivered. Kuck v. Sommers (1950), 100 N.E.2d 68, 75, 59 Ohio Abs. 400. Various sections of the Uniform Commercial Code, as adopted in Ohio, support the conclusion that the owner of a promissory note should be recognized as the owner of the related mortgage. . . . Thus, although the recorded assignment is not before us, there is sufficient evidence on the record to establish that appellee is the current owner of the note and mortgage at issue in this case, and, therefore, the real party in interest.”) (citations to Ohio’s versions of UCC §§ 9-109(a)(3), 9-102(a)(72)(D) and 9-203(g) omitted).

Oklahoma: Zorn v. Van Buskirk, 111 Okla. 211, 239 P. 151 (1925) (“the mortgage follows the note”).

Pennsylvania: In re Miller, No. 99-25616JAD, 2007 WL 81052, at *6 & n.7 (Bankr. W.D. Pa. Jan.

9, 2007) (citing and quoting with approval Gray, Mortgages in Pennsylvania at § 1-3 (1985) (“the

mortgage follows the note”)).

South Carolina: MidFirst Bank, SSB v. C.W. Haynes & Co., Inc., 893 F. Supp. 1304, 1318 (D. S.C. 1994) (“South Carolina recognizes the ‘familiar and uncontroverted proposition’ that ‘the assignment of a note secured by a mortgage carries with it an assignment of the mortgage.’ Hahn v. Smith, 157 S.C. 157, 154 S.E. 112 (1930); Ballou v. Young, 42 S.C. 170, 20 S.E. 84 (1894).”).

Texas: Kirby Lumber Corp. v. Williams, 230 F.2d 330, 333 (5th Cir. 1956) (applying Texas law) (“The rule is fully recognized . . . that a mortgage to secure a negotiable promissory note is merely an incident to the debt, and passes by assignment or transfer of the note.”).

Utah: Smith v. Jarman, 211 P. 962, 966 (Utah 1922) (“The modern doctrine that the mortgage follows the note as an incident was thus long ago recognized by this court . . . .”).

Virginia: Yerby v. Lynch, 3 Gratt. 460, 1847 WL 2384, at *8-10 (Va. 1847) (“the mortgage follows the debt”).

Virgin Islands: UMLI C VP LLC v. Matthias, 234 F. Supp. 2d 520, 523 (D. V.I. 2002) (citing and quoting with approval the “RESTATEMENT (THIRD) OF PR OPER TY, MORTGAGES § 5.4(a) (1997). The comment to this section further explains that ‘[t]he principle of this subsection, that the mortgage follows the note, … applies even if the transferee does not know that the obligation is secured by a mortgage…. Recordation of a mortgage assignment is not necessary to the effective transfer of the obligation or the mortgage securing it.’ Id. § 5.4 cmt. b (1997). Accordingly, in the Virgin Islands, no separate document specifically assigning and transferring the mortgage which secures a note is required to accompany the assignment of the obligation, because the mortgage automatically follows the note.”).

Washington: Nance v. Woods, 79 Wash. 188, 189, 140 P. 323, 323 (Wash. 1914) (“the mortgage follows the note”).

As mentioned above, the general common law rule that “the mortgage follows the note” is codified in Article 9 of the UCC. Section 9-203(g) of the UCC states: “The attachment of a security interest in a right to payment or performance secured by a security interest or other lien on personal or real property is also attachment of a security interest in the security interest, mortgage, or other lien.”17 UCC § 9-203(g) (emphasis added). The phrase “security interest” in this provision includes a buyer’s ownership interest because UCC § 1-201(b)(35) defines “security interest” to include “any interest of a . . . buyer of . . . a promissory note in a transaction that is subject to Article 9.” Thus, under Article 9, a sale of a mortgage note means that the buyer’s rights attach not only to the mortgage note itself but also to the mortgage that secures the mortgage note. Moreover, under UCC § 9-308(e), those rights are perfected and can be enforced against third parties. Regarding the impact of these UCC provisions, one treatise states: “Article 9 makes it as plain as possible that the secured party need not record an assignment of mortgage, or anything else, in the real property records in order to perfect its rights in the mortgage.” J. McDonnell and J. Smith, Secured Transactions Under the Uniform Commercial Code, § 16.09[3][b].

Courts in several states have affirmed and applied the “mortgage follows the note” rule in cases where the mortgage assignment was not recorded by the transferee.19 See, e.g., Nat’l Livestock Bank v. First Nat. Bank, 203 U.S. 296, 307-08 (1906) (citing with approval a decision of the Supreme Court of Kansas for the proposition that “where a mortgage upon real estate is given to secure payment of a negotiable note, and before its maturity the note and mortgage are transferred by indorsement of the note to a bona fide holder, the assignment, if there be a written one, need not be recorded”); Jackson v. Mortgage Elec. Registration Sys., Inc., 770 N.W.2d 487, 497-98, 500 (Minn. 2009) (applying the “mortgage follows the note” rule where there was no assignment of the mortgage); UMLI C VP LLC v. Matthias, 234 F. Supp. 2d 520, 523 (D. V.I. 2002) (“Recordation of a mortgage assignment is not necessary to the effective transfer of the obligation or the mortgage securing it.”); Federal Nat’l Mort. Ass’n v. Kuipers, 314 Ill. App. 3d 631, 635, 732 N.E.2d 723, 727 (Ill. Ct. App. 2000) (“Because the assignment of the debt, with nothing more, is sufficient to preserve the mortgage lien, it cannot follow that the lien is somehow extinguished for the failure to record the assignment. Therefore, we are persuaded that the mortgage lien and priority position inure to the benefit of the assignee and that recording the assignment is unnecessary to preserve the security for the debt.”); In re Kennedy Mortgage Co., 17 B.R. 957, 964 (Bankr. D.N.J. 1982) (“The fact that assignments of mortgages may be recorded does not affect the validity of an assignment of a mortgage which has not been recorded.”).

Courts have also affirmed and applied the “mortgage follows the note” rule even when there was no actual separate written assignment of the mortgage. See, e.g., Carpenter v. Longan, 83 U.S. 271, 275 (1873) (“The transfer of the note carries with it the security, without any formal assignment or delivery, or even mention of the latter.”); Chase Home Fin., LLC v. Fequiere, 119 Conn. App. 570, 989 A.2d 606, 610-11 (Conn. Ct. App. 2010) (“General Statutes § 49-17 [which codifies the “mortgage follows the note” rule] permits the holder of a negotiable instrument that is secured by a mortgage to foreclose on the mortgage even when the mortgage has not yet been assigned to him.” (emphasis added)); U.S. Nat’l Bank Ass’n v. Marcino, 181 Ohio App.3d 328, 337 (2009) (holding that bank was the “current owner” of a mortgage note and the related mortgage despite the fact that “there is no evidence on the record that appellee is the current assignee of the note and mortgage,” and finding that “the negotiation of a note operates as an equitable assignment of the mortgage, even when the mortgage is not assigned or delivered” (citing Kuck v. Sommers, 100 N.E.2d 68, 75, 59 Ohio Abs. 400 (1950)); UMLI C VP LLC v. Matthias, 234 F. Supp. 2d 520, 523 (D. V.I. 2002) (the principle “that the mortgage follows the note, . . . applies even if the transferee does not know that the obligation is secured by a mortgage”); In re Union Packing Co., 62 B.R. 96, 100 (Bankr. D. Neb. 1986) (with or without the assignment of the mortgage, the assignee of the promissory note has the right to enforce the mortgage securing the note); Morris v. Bacon, 123 Mass. 58, 59 (1877) (note holder that endorsed and delivered mortgage note to bank as security for a loan, but without an assignment of the mortgage, was required by the court to transfer the mortgage to the bank); Bremer County Bank v. Eastman, 34 Iowa 392, 1872 WL 254, at *1 (Iowa 1872) (“The transfer of the note, secured by the mortgage, carried the mortgage with it as an incident to the debt, and the indorsee of the note could maintain an action in his own name, to foreclose the mortgage without any assignment thereon whatever.”); Southerin v. Mendum, 5 N.H. 420, 1831 WL 1104, at *8 (N.H. 1831) (“the right of the mortgagee before foreclosure is . . . assignable by a mere assignment of the debt, without deed or writing”).

Common MBS practices, as described above, are consistent with the general rule that “the mortgage follows the note”: pursuant to the pooling and servicing agreement that governs a mortgage-loan securitization, and the language of assignment typically contained in such an agreement, the mortgage note and the mortgage itself are sold, assigned, transferred and delivered to the trustee, and the transferor also typically delivers a written assignment of the mortgage that is in blank in recordable form. Courts have held that the language of assignment contained in a pooling and servicing agreement, along with the corresponding transfer, sale and delivery of the mortgage note and mortgage, are sufficient to transfer the mortgage to the transferee/trustee or its designee or nominee. See, e.g., Wells Fargo Bank, N.A. v. Konover, No. 3:05 CV 1924 (CFD), 2009 WL 2710229, at *3 (D. Conn. Aug. 21, 2009) (MBS pooling agreement vested authority in pool trustee to bring legal action in the event of default); U.S. Bank N.A. v. Cook, No. 07 C 1544, 2009 WL 35286, at *2-3 (N.D. Ill. Jan. 6, 2009) (MBS pooling trust agreement effected an assignment of the mortgage at issue to the pool trustee); In re Samuels, 415 B.R. 8, 18 (Bankr. D. Mass. 2009) (“The [Pooling and Servicing Agreement] itself [by which the MBS loan trust was created], in conjunction with the schedule of mortgages deposited through it into the pool trust, served as a written assignment of the designated mortgage loans, including the mortgages themselves.”); EMC Mortgage Corp. v. Chaudhri FSB, 400 N.J. Super. 126, 141, 946 A.2d 578, 588 (N.J. Super. Ct. 2008) (“any [mortgage] assignment shall pass and convey the estate of the assignor in the mortgaged premises, and the assignee may sue thereon in his own name.’” (citing New Jersey Stat. Ann. § 46:9-9 and Byram Holding Co. v. Bogren, 2 N.J. Super. 331, 336, 63 A.2d 822 (N.J. Ch. Div. 1949)); LaSalle Bank N.A. v. Lehman Bros. Holdings, Inc., 237 F. Supp. 2d 618, 632-33 (D. Md. 2002) (MBS pooling agreement granted trustee authority to bring suit on behalf of trust); LaSalle Bank N.A. v. Nomura Asset Capital Corp., 180 F. Supp. 2d 465, 470-71 (S.D.N.Y. 2001) (language in the pooling and servicing agreement for MBS trust effectually assigned mortgage to the pool trustee).

What is the Relationship Between the UCC and State Real Property Laws?

Article 9 does not apply to “the creation or transfer of an interest in or lien on real property, . . . except to the extent that provision is made for . . . liens on real property in Sections 9-203 and 9-308.” UCC §9-109(d)(11) (emphasis added). As discussed above, UCC § 9-203(g) provides that, when a security interest in a mortgage note attaches, a security interest in the underlying mortgage also attaches, and UCC § 9-308(e) provides the same regarding the perfection of the security interest. See UCC § 9-203 cmt. 9 (the “mortgage follows the note” rule codified into UCC §§ 9-203(g) and 9-308(e)). In addition, UCC § 9-109(b) makes clear that Article 9 does apply to mortgage notes even though Article 9 does not govern the creation of the mortgage itself:

The application of this article [9] to a security interest [remember that this term is defined to include any interest of a buyer of a promissory note in a transaction subject to Article 9] in a secured obligation [e.g., mortgage note] is not affected by the fact that the obligation [e.g., mortgage note] is itself secured by a transaction or interest [e.g., creation of the

mortgage or deed of trust itself] to which this article does not apply.

UCC § 9-109(b)

The creation of an interest in or lien on real property, including a mortgage, is governed by the non-UCC law of the state in which the property is located. See, e.g., Oregon v. Corvallis Sand and Gravel Co., 429 U.S. 363, 378-79 (1977). Likewise, the enforceability of mortgages (including the right and method to foreclose) is subject to all of the conditions precedent and requirements that are set forth in the particular mortgage itself and in all applicable state and local laws. Those conditions precedent and procedural requirements vary from mortgage to mortgage and from state to state. Thus, ownership of a mortgage (i.e., without notice to the mortgagor or the public, without judicial proceedings (where required), without satisfaction of other conditions precedent or procedural requirements in the mortgage itself or in applicable state law), does not always give the holder of the mortgage the legal ability to foreclose on the mortgage. Though a discussion of the other necessary prerequisites to foreclosure is beyond the scope of this paper, the fact that other steps may need to be taken by the owner of a mortgage note, or the owner of a mortgage, is neither unique nor surprising in our legal and regulatory system and does not diminish an otherwise legally effective transfer of the mortgage note and mortgage.

How Does the Use of MERS Affect These Issues?

The use of MERS as the nominee for the benefit of the trustee and other transferees in the mortgage loan securitization process has been a subject of litigation in recent years. See, e.g., Bellistri v. Ocwen Loan Servicing, LLC, 284 S.W.3d 619, 623 (Mo. Ct. App. 2009). Some cases address the authority or ability of MERS or transferees of MERS to foreclose on a mortgage for which MERS is or was the mortgagee of record. See, e.g., Saxon Mort. Serv., Inc. v. Hillery, No. C-08-4357 EMC, 2008 WL 5170180, at *4-5 (N.D. Cal. Dec. 9, 2008). As a general matter, the assignment and transfer of a mortgage to MERS as nominee of and for the benefit of the beneficial owner of the mortgage does not adversely impact the right to foreclose on the mortgage.

Decisions in many jurisdictions support this conclusion. See, e.g., In re Mortgage Elect. Registration Sys., Inc. (MERS) Litig., No. 2:09-md-2119, 2010 WL 4038788, at *8 (D. Ariz. Sept. 30, 2010) (“Plaintiffs have not cited any legal authority where the naming of MERS . . . was cause to enjoin a non-judicial foreclosure as wrongful.”); Commonwealth Property Advocates, LLC v. Mortgage Elect. Registration Sys., Inc., No. 2:10-CV-340 TS, 2010 WL 3743643, at *3 (D. Utah Sept. 20, 2010) (MERS as nominee has authority to foreclose); Taylor v. Deutsche Bank Nat’l Trust Co., No. 5D09-4035, 2010 WL 3056612, at *3 (Fla. App. Aug. 6, 2010) (“[T]he written assignment of the note and mortgage from MERS to Deutsche Bank properly transferred the note and mortgage. . . . The transfer, moreover, was not defective by reason of the fact that MERS lacked a beneficial ownership interest in the note at the time of the assignment, because MERS was lawfully acting in the place of the holder and was given explicit and agreed upon authority to make just such an assignment.”); Mortgage Elect. Registration Sys., Inc. v. Bellistri, No. 4:09-CV-731 CAS, 2010 WL 2720802, at *15 (E.D. Mo. July 1, 2010) (“[a]s the nominee of the original lender … or the lender’s assigns, MERS has bare legal title to the note and deed of trust securing it, and this is sufficient to create standing” to initiate foreclosure proceedings); Silvas v. GMAC Mortgage, LLC, No. CV-09-265-PHX-GMS, 2009 WL 4573234, at *8 (D. Ariz. Jan. 5, 2010) (MERS empowered to foreclose where MERS is designated on deed of trust as beneficiary); Diessner v. Mortgage Elec. Registration Sys., 618 F. Supp. 2d 1184, 1187-91 (D. Ariz. 2009) (MERS and trustee under deed of trust are authorized to institute non-judicial foreclosure proceeding); Jackson v. Mortgage Elec. Registration Sys., Inc., 770 N.W.2d 487, 501 (Minn. 2009) (rejecting argument that transfer of mortgage note to MERS is a transfer that must be recorded before foreclosure); Reynoso v. Paul Financial, LLC, No. 09-3225 SC, 2009 WL 3833298, at *2 (N.D. Cal. Nov. 16, 2009) (naming of MERS as initial beneficiary under deed of trust, as nominee for the lender, and the subsequent transfer of the deed of trust from MERS to a transferee was effective and did not hinder transferee’s right to foreclose); Blau v. America’s Servicing Co., No. CV-08-773, 2009 WL 3174823, at *8 (D. Ariz. Sept. 29, 2009) (MERS authorized under deed of trust to act on behalf of lender and transfer its interests); Farahani v. Cal-Western Recon. Corp., No. 09-194, 2009 WL 1309732, at *2-3 (N.D. Cal. May 8, 2009) (MERS authorized to pursue non-judicial foreclosure action); Vazquez v. Aurora Loan Servs., No 2:08-cv-01800-RCJRJJ, 2009 WL 1076807, at *1 (D. Nev. Apr. 20, 2009) (loan documents sufficiently demonstrate MERS’ standing “with respect to the loan and the foreclosure”); Pfannenstiel v. Mortgage Elect. Registration Sys., Inc., No. CIV S-08-2609, 2009 WL 347716, at *4 (E.D. Cal. Feb. 11, 2009) (dismissing plaintiff ’s claim that MERS lacked authority to foreclose); Trent v. Mortgage Elect. Registration Sys., Inc., 288 Fed. App’x 571, 572 (11th Cir. 2008) (MERS “has the legal right to foreclose on the debtors’ property” and “is the mortgagee”); Peyton v. Recontrust Co., No. TC021868, Notice of Ruling, at 2 (Cal. Super. Ct. County of Los Angeles S. Cent. Dist. Oct. 15, 2008) (MERS may foreclose under California law); Johnson v. Mortgage Elect. Registration Sys., Inc., 252 Fed. App’x 293, 294 (11th Cir. 2007) (summary judgment for MERS on its action for foreclosure of plaintiff ’s property); In re Smith, 366 B.R. 149, 151 (Bankr. D. Colo. 2007) (MERS has standing to conduct foreclosure on behalf of the beneficiary); Mortgage Elect. Registration Sys., Inc. v. Revoredo, 955 So.2d 33, 34 (Fla. Dist. Ct. App. 2007) (“Because, however, it is apparent – and we so hold – that no substantive rights, obligations or defenses are affected by use of the MERS device, there is no reason why mere form should overcome the salutary substance of permitting the use of this commercially effective means of business.”); Mortgage Elect. Registration Sys., Inc. v. Ventura, CV054003168S, 2006 WL 1230265, at *1 (Conn. Super. Apr. 20, 2006) (MERS is proper party in foreclosure).

There are several minority decisions that, in some form, have taken issue with MERS. But none of these decisions, to our knowledge, has invalidated a mortgage for which MERS is the nominee, and none of these decisions has challenged MERS’ ability to act as a central system to track changes in the ownership and servicing of loans:22 See Rinegard-Guirma v. Bank of Am., Nat’l Ass’n, No. 10-1065-PK , 2010 WL 3945476, at *4 (D. Or. Oct. 6, 2010) (suggesting that MERS may not qualify as a legitimate beneficiary of a deed of trust under Oregon law, and preliminarily enjoining foreclosure action by MERS); In re Allman, No. 08-31282-elp7, 2010 WL 3366405, at *10 (Bankr. D. Or. Aug. 24, 2010) (same); Mortgage Elec. Registration Sys., Inc. v. Saunders, 2 A.3d 289, 297 (Me. 2010); In re Box, No. 10-20086, 2010 WL 2228289, at *5 (Bankr W.D. Mo. June 3, 2010) (finding that MERS, as beneficiary and nominee under the deed of trust lacked authority to assign the mortgage note because it never “held” the note itself);23 In re Hawkins, No. BK -s-07-13593-LBR , 2009 WL901766, at *3 (Bankr. D. Nev. Mar. 31, 2009) (finding that MERS was not a true “beneficiary” under a deed of trust, that, under the UCC, MERS was not entitled to enforce the note, and that “[i]n order to foreclose, MERS must establish there has been a sufficient transfer of both the note and deed of trust, or that it has authority under state law to act for the note’s holder”).

Finally, it is important to recognize that the UCC does not displace traditional rules of agency law.

See UCC § 1-103(b) (“Unless displaced by the particular provisions of [the Uniform Commercial Code], the principles of law and equity, including the law [of] . . . principal and agent . . . supplement its provisions.”); see

also UCC § 9-313 cmt. 3 (principles of agency apply for purposes of determining “possession” under Article 9).

Under general agency law, an agent has authority to act on behalf of its principal where the principal “manifests assent” to the agent “that the agent shall act on the principal’s behalf and subject to the principal’s control, and the agent manifests assent or otherwise consents so to act.” Restatement (Third) of Agency § 1.01 (2006).

Accordingly, the UCC does not prevent MERS or others, including loan servicers, from acting as the agent for the note holder in connection with transfers of ownership in mortgage notes and mortgages. See, e.g., In re Tucker, No. 10-61004, 2010 WL 3733916, at *6 (Bankr. W.D. Mo. Sept. 20, 2010) (finding MERS was the “agent for [the lender] under the Deed of Trust from the inception, and MERS became the agent for each subsequent note-holder under the Deed of Trust when each such note holder negotiated the Note to its successor and assign”); King v. Am. Mortgage Network, Inc., No. 1:09CV162 DAK, 2010 WL 3516475, at *3 (D. Utah Sept. 2, 2010) (rejecting argument that note and deed of trust were split because Fannie Mae held the note and MERS was listed as the nominal beneficiary under the deed of trust and finding that both MERS and the authorized loan servicer had authority as agents of the note holder to act on behalf of the note holder, including the initiation of foreclosure proceedings on the underlying property); Mich. Comp. Laws § 600.3204(1)(d) (“The party foreclosing the mortgage is either the owner of the indebtedness or of an interest in the indebtedness secured by the mortgage or the servicing agent of the mortgage.”); Hilmon v. Mortgage Elect. Registration Sys., Inc., No. 06-13055, 2007 WL 1218718, at *3 (E.D. Mich. Apr. 23, 2007); Caravantes v. California Reconveyance Co., No. 10-cv-1407-IEG (AJB), 2010 WL 4055560, at *9 (S.D. Cal. Oct. 14, 2010) (“as servicer of the subject loan in this case, JP Morgan had the authority to record the Notice of Default and to enforce the power of sale under the Deed of Trust”); Birkland v. Silver State Fin. Servs., Inc., No. 2:10-CV-00035-KJD-LRL, 2010 WL3419372, at *3 (D. Nev. Aug. 25, 2010) (“MERS, as nominee on a deed of trust, is granted authority as an agent on behalf of the nominator (holder of the promissory note) as to the administration of the deed of trust, which would include substitution of trustees”). In short, principles of agency law provide MERS and loan servicers another legal basis for their respective roles in the transfer of mortgage notes and mortgages.

4. Conclusion

In summary, the longstanding and consistently applied rule in the United States is that, when a mortgage note is transferred, “the mortgage follows the note.” When a mortgage note is transferred and delivered to a transferee in connection with the securitization of the mortgage loan pursuant to an MBS pooling and servicing agreement or similar agreement, the mortgage automatically follows and is transferred to the mortgage note transferee, notwithstanding that a third party, including an agent/nominee entity such as MERS, may remain as the mortgagee of record. Both common law and the UCC confirm and apply this rule, including in the context of mortgage loan securitizations. The legal principles and processes discussed above provide for – and, if followed, result in – a valid and enforceable transfer of mortgage notes and the underlying mortgages. The transfer and legal effectiveness of mortgage notes and mortgages are not diminished by the fact that the enforceability of mortgages, including the right to foreclose, is subject to the conditions precedent and requirements that are set forth in the particular mortgage itself and in the laws of the state in which the mortgaged property is located.

Footnotes:

1. References to the UCC are to the Official Text of the Model UCC, as revised, issued by the National Conference of Commissioners on Uniform State Laws.

2. Note that the UCC replaces the more common U.S. spelling of “endorsement” for the less common “indorsement.” The UCC spelling is used throughout this Executive Summary.3. However, in some states, such as Massachusetts and Minnesota, courts have held that the transfer of a mortgage note without an

express transfer of the mortgage vests in the note holder only an equitable interest in the mortgage. This arrangement has been

described as follows: the holder of the mortgage holds the legal title to the mortgage in constructive trust for the benefit of the

mortgage note holder. In both states, however, case law suggests that foreclosure proceedings must be initiated by, or at least in the

name of, the holder of the legal title in the mortgage.

4. In most states, recording of an assignment of mortgage is generally not required to ensure the enforceability of the assignment of mortgage as between the assignor and assignee, and anyone with knowledge thereof. It is beyond the scope of this post to discuss in detail the potential risks to the mortgage transferee of not recording a mortgage assignment.

Those risks might include, among others, delaying the transferee’s ability to foreclose on the mortgage, failing to receive notices that may go to the mortgagee of record, and otherwise leaving the assignee open to negligent or fraudulent actions or inactions by the mortgagee of record that could bind the mortgage transferee and impair the value or enforceability of the mortgage. Similarly, when an assignment of mortgage is not recorded, the assignor may be liable for certain obligations imposed upon a mortgagee of record, such as the obligation to provide a pay-off statement or mortgage release within a designated time period.

5. Issues related to a party’s right to foreclose or to engage in foreclosure-related activities are generally outside the scope of this paper.

6. For ease of reference, “mortgage” will be used throughout much of this post to refer to both mortgages and deeds of trust, and “mortgage note” will be used to refer to a promissory note that is secured by a mortgage.

7. References to the UCC are to the Official Text of the Model UCC, as revised, issued by the National Conference of Commissioners

on Uniform State Laws.

8. While Article 9 does not directly govern a mortgage on real property, the fact that a mortgage note is itself secured by a mortgage on real property does not render Article 9 inapplicable to transfers of the mortgage note. See UCC § 9-109(b) (“The application of this article [9] to a security interest in a secured obligation is not affected by the fact that the obligation is itself secured by a transaction or interest to which this article does not apply.”).

9. Note that the UCC eschews the more common U.S. spelling of “endorsement” for the less common “indorsement.” The UCC spelling is used throughout this paper.

10. Article 3 and Article 9 are not mutually exclusive. Article 9 applies to the transfer of all “promissory notes,” which includes negotiable

and non-negotiable instruments. Both Article 3 and Article 9 apply to “negotiable instruments.” With respect to non-negotiable instruments, only Article 9 applies to the transfer.

11. UCC § 3-104(b) defines “instrument” simply as a “negotiable instrument” for purposes of Article 3. As discussed in more detail below, the definition of “instrument” in Article 9 (governing secured transactions) is somewhat more expansive.

12. It is important to note that Article 3 does not concern “ownership” of a mortgage note, but instead provides for the transfer of a mortgage note and the right to enforce such notes. See UCC § 3-301; UCC § 3-203 cmt. 1. A party need not be the “owner” of the mortgage note to enforce it. See UCC § 3-301 (“A person may be a person entitled to enforce the instrument even though the person is not the owner of the instrument or is in wrongful possession of the instrument.”). Thus, a party may have the right to enforce the instrument, but not have “ownership” of that instrument. UCC § 3-203 cmt 1. For an example of situations where a party with the right to enforce an instrument is not also the “owner” of the instrument, see UCC 3-203 cmt. 1 and Note 16 infra.

13. Note also that UCC § 3-203(c) provides for the scenario in which an instrument is transferred for value without the indorsement that, as described in the text below, would be needed for the mortgage note to have been “negotiated.” Under that section, if a negotiable mortgage note is transferred for value as part of a loan securitization, but the transferor fails to indorse the note, the transferee of the note has the “specifically enforceable right to the unqualified indorsement of the transferor.” UCC § 3-203(c); see Note 16, infra (discussing distinction between the right to enforce a mortgage note and ownership of the mortgage note).

14. An indorsement is considered to be made “on an instrument” for purposes of negotiation when it is made either on the mortgage note itself or on a separate paper, often referred to as an “allonge,” that is affixed to the note. See UCC § 3-204(a). Once affixed, the allonge becomes “part of the instrument.” Id.

15. As noted above, the right to enforce an instrument and the ownership of that instrument are not necessarily the same. See UCC §3-203 cmt. 1. Thus, a party may have the right to enforce the instrument, but not have “ownership” of that instrument. Id. A party need not be the “owner” of the note to enforce it. See UCC § 3-301 (“A person may be a person entitled to enforce the instrument even though the person is not the owner of the instrument or is in wrongful possession of the instrument.”). For example, if X (holder of an instrument payable to X) sells the instrument to Y pursuant to a document conveying all of X’s right, title and interest

in the instrument to Y, but does not deliver immediate possession to Y, Y would have ownership of the instrument under the agreement, but Y generally would not be entitled to enforce the instrument until it obtained possession of the instrument. Id.

16. UCC § 3-301 also permits a person without possession to enforce a mortgage note where, in certain circumstances, there has been mistaken payment as defined in UCC § 3-418(d).

17. Article 9 also applies to the creation of a lien on, or a “less-than-ownership security interest” in, a mortgage note. Because most assignments and transfers of mortgage notes in loan securitizations are of the ownership of the mortgage notes, not a mere lien on or security interest in the notes, this paper addresses only outright sales of mortgage notes under Article 9. The principles discussed below regarding attachment of a buyer’s interest in a sale of mortgage notes are identical to those that apply in the context of the creation of a lien on mortgage notes, and the principles regarding perfection of the interest in the mortgage notes are likewise very similar. “Although . . . Article [9] occasionally distinguishes between outright sales of receivables and sales that secure an obligation, neither . . . Article [9] nor the definition of “security interest” (Section 1-201(37)) delineates how a particular transaction is to be classified. That issue is left to the courts.” UCC § 9-109 cmt 4.

18. Under Article 9, the term “instrument” is defined broadly as “a negotiable instrument or any other writing that evidences a right to the payment of a monetary obligation, is not itself a security agreement or lease, and is of a type that in ordinary course of business is transferred by delivery with any necessary indorsement or assignment.” UCC § 9-102(a)(47).

19. The comments to UCC § 9-203 expressly provide that “Subsection (g) codifies the common-law rule that a transfer of an obligation secured by a security interest or other lien on personal or real property also transfers the security interest or lien.” UCC § 9-203 cmt. 9; see also Restatement (Third) of Property (Mortgages) § 5.4(a) (1997). The same holds true for UCC § 9-308(e), under which perfection of a security interest in a mortgage note also accomplishes perfection of a security interest in the mortgage. See UCC §9-308 cmt. 6.

20. However, in some states, such as Massachusetts and Minnesota, courts have held that the transfer of a mortgage note without an express transfer of the mortgage vests in the note holder only an equitable interest in the mortgage. See, e.g., First Nat’l Bank of Cape Cod v. North Adams Hoosac Savs. Bank, 7 Mass. App. Ct. 790, 796 (1979); Jackson v. Mortgage Elect. Registration Sys., Inc., 770 N.W.2d 487, 497, 500-01 (Minn. 2009). This arrangement has been described as follows: the holder of the mortgage holds the legal title to the mortgage in constructive trust for the benefit of the mortgage note holder. See First Nat’l Bank of Cape Cod, 7 Mass. App. Ct. at 796. In both states, however, case law suggests that foreclosure proceedings must be initiated by, or at least in the name of, the holder of the legal title in the mortgage. See Jackson, 770 N.W.2d at 500; U.S. Bank Nat’l Ass’n v. Ibanez, Nos. 08 MISC 384283 (KCL), 08 MISC 386755 (KCL), 2009 WL 3297551, at *11 (Mass. Land Ct. Oct. 14, 2009) (rejecting argument that note holders had authority to foreclose on mortgages for which their status as full mortgagees was in dispute) (currently on appeal to the Massachusetts Supreme Judicial Court).

21. Courts have observed that UCC § 9-203(g) codifies the “mortgage follows the note” rule. See, e.g., U.S. Nat’l Bank Ass’n v. Marcino, 181 Ohio App.3d 328, 337 (2009) (quoting with approval Official Comment 9 to UCC § 9-203: “subsection (g) [of UCC § 9-203] codifies the common-law rule that a transfer of an obligation secured by a security interest or other lien on personal or real property also transfers the security interest or lien”).

22. As discussed above, UCC § 9-308(e) provides that “perfection of a security interest in a right to payment or performance also perfects a security interest in a security interest, mortgage, or other lien on personal or real property securing the right.” UCC §9-308(e) (emphasis added).

23. In most states, recording of an assignment of mortgage is generally not required to ensure the enforceability of the assignment of mortgage as between the assignor and assignee, and anyone with knowledge thereof. It is beyond the scope of this paper to discuss in detail the potential risks to the mortgage transferee of not recording a mortgage assignment. Those risks might include, among others, delaying the transferee’s ability to foreclose on the mortgage, failing to receive notices that may go to the mortgagee of record, and otherwise leaving the assignee open to negligent or fraudulent actions or inactions by the mortgagee of record that could bind the mortgage transferee and impair the value or enforceability of the mortgage. Similarly, when an assignment of mortgage is not recorded, the assignor may be liable for certain obligations imposed upon a mortgagee of record, such as the obligation to provide a pay-off statement or mortgage release within a designated time period.

24. Although the rule is “the mortgage follows the note” when a mortgage note is assigned, some case law indicates that the converse is not true and that the mortgage note does not necessarily follow the mortgage if there is an attempted assignment of the mortgage alone or separate from the mortgage note. See, e.g., Bellistri v. Ocwen Loan Servicing, LLC, 284 S.W.3d 619, 623 (Mo. Ct. App. 2009) (“An assignment of the deed of trust separate from the note has no ‘force.’”); Saxon Mort. Serv., Inc. v. Hillery, No. C-08-4357 EMC, 2008 WL 5170180, at *4-5 (N.D. Cal. Dec. 9, 2008) (“For there to be a valid assignment, there must be more than just assignment of the deed [of trust] alone; the note must also be assigned.”); In re Wilhelm, 407 B.R. 392, 400-05 (Bankr. D. Idaho 2009); Kelley v. Upshaw, 39 Cal.2d 179, 192 (1952) (“In any event, Kelley’s purported assignment of the mortgage without an assignment of the debt which is secured was a legal nullity.”). This is consistent with the longstanding aspect of the “mortgage follows the note” rule that “the note and mortgage are inseparable; the former as essential, the latter as an incident.” In re Bird, No. 03-52010-JS, 2007 WL 2684265, at *2-4 (Bankr. D.Md. Sept. 7, 2007).

25. UCC Article 3, which applies to negotiable mortgage notes, does not apply to mortgages themselves because mortgages do not fit the definition of “negotiable instrument” in UCC § 3-104(a).

26. Some investors and loan servicers have sought to lessen the risk of challenges to foreclosure pertaining to MERS by assigning loans out of MERS and to the note holder prior to the initiation of foreclosure.

27. The Court in In re Box expressly noted, but did not decide, the question of whether MERS had authority to assign the note as an agent of the lender or even as “a nominee beneficiary.” In re Box, 2010 WL 2228289 at *4. The same court, in a later case, answered the question directly and found that MERS, as the designated “nominee for the lender and its assigns,” “was the agent for [the lender] under the Deed of Trust from the inception, and MERS became agent for each subsequent note-holder under the Deed of Trust when each such note holder negotiated the Note to its successors and assigns.” In re Tucker, No. 10-61004, 2010 WL 3733916, at *6 (Bankr. W.D. Mo. Sept. 20, 2010) (“[w]hen [note-holder] acquired the right to enforce the Note as the note-holder, MERS held the beneficial interest in the Deed of Trust on behalf of [note-holder] and [note-holder] had the right to enforce all the rights granted to [the original lender] and its successors and assigns in the Deed of Trust”). Thus, the Court found that the Note and the Deed of Trust were not split because of MERS’ status as agent for the note holders. Id.

28. Some parties to litigation, and commentators, have relied upon the Kansas Supreme Court’s decision in Landmark National Bank v. Kesler, 216 P.3d 158 (Kan. 2009), to support the proposition that the identification of MERS as a nominee on a mortgage is improper. However, reliance on the decision in Kesler for that proposition is misplaced and stretches the decision well-beyond its actual holding. In Kesler, the Court merely held that MERS, in its capacity as the nominee for the lender under a second-position mortgage, was not entitled to notice of a foreclosure sale by the holder of the senior mortgage. See id. at 169-70. As the Kansas Appeals Court that considered the case noted, “[w]hether MERS may act as a nominee for the lender, either to bring a foreclosure suit or for some other purpose, is not at issue….” Landmark Nat’l Bank v. Kesler, 192 P.3d 177, 180 (Kan. Ct. App. 2008).

For More Info on How To Effectively Challenge Your Wrongful Foreclosure Using Valid Mortgage Securitization Arguments, UCC and Relevant Case Laws: Visit http://www.fightforeclosure.net